結果

美元/日元懸浮在危險區域:日本能否阻止攀升至 160?

美元/日元正在交易者現在稱為「危險區」的內容中,這是以前迫使日本強迫的 155—160 範圍。

美元/日元正在交易者所稱為「危險區域」中,這是以前迫使日本強迫的 155—160 範圍。據分析師表示,該貨幣對正在測試水平,如果突破,可能會迫使東京再次干預以保護日元。對於市場來說,這不僅僅是心理門檻,而是歷史所繪製的一條線。每一次接近 160 點的行動都恢復了對過去的干預和對日本在進行投入之前將允許其貨幣走弱多遠的猜測回憶。

報導稱,緊張局勢的核心是日本財政擴張和其謹慎的貨幣立場之間日益差異。正如美國維持高利率的同時,總理高一早上一的 21.3 萬億日元(112 億英鎊)的刺激計劃推動收益率上升並進一步削弱日元。

現在的問題是,日本是否可以-或將-及時採取行動,以阻止美元/日元的上漲,然後再突破 160,測試東京在全球舞台上的決心。

什麼驅動美元/日元?

日元的最新下跌源於日本與美國的政策差距越來越大。高市的刺激措施是大流行以來最大的刺激措施,包括能源緩解、稅收減免和現金派發的支出。它旨在緩解生活成本的壓力,但投資者認為它是通脹和財政上毫無慮的。彭博社報道,隨著債務擔憂加深,對長期財政紀律的信心衰退,日本政府債券(JGB)收益率已飆升至 2008 年以來的最高水平

日本央行的謹慎態度僅增強了壓力。上田行長繼續認為,即使通脹仍在 2% 的目標上方,工資增長必須穩定在任何重大政策改變之前。

相比之下,美聯儲保持美國利率上升,並且仍不願快速削減。這種收益差使持有美元更有回報,使資金流出日元,並使美元/日元保持在多年高位附近。

為什麼重要

市場觀察者表示,日元的疲軟兩方向都會減少。較軟的貨幣使豐田和索尼等出口商受益,他們的海外收入意味著更高的利潤。然而對於進口商和家庭來說,痛苦是立即的。日本主要依賴進口燃料和食品,這意味著美元/日元的每一次升高都會使日常生活變得更加昂貴。布魯金斯研究所的羅賓布魯克斯警告說:「日本的實際實際實際價值幾乎與土耳其里拉一樣疲弱,」稱政府的財政立場為「拒絕債務」。

在日本的邊界以外,日元是全球風險情緒的氣象表。當它急劇下跌時,它表明對美元的信心日益增長,並鼓勵以日元資助的手提交易策略。但是,如果東京干預,它也會增加突然逆轉的風險。市場仍然回憶年中期,據報導,日本在美元/日元短暫突破 160 億美元後花費了超過 60 億美元的保護其貨幣。這種遺產使該樂隊中的每一動作都感覺像是倒數計時。

對市場和策略的影響

在債券市場上,投資者要求更高收益率以抵消財政風險,將十年期 JGB 利率高於 1%,四十年期收益率超過 3.6%。上升反映了對日本的債務(已經是日本經濟的兩倍以上)在高市的支持增長議程下將進一步增長的擔憂。

財政部長片山幸已經警告說,政府「會採取行動防止失規的行動」,這一句話現在交易者解釋為隱蔽的干預威脅。

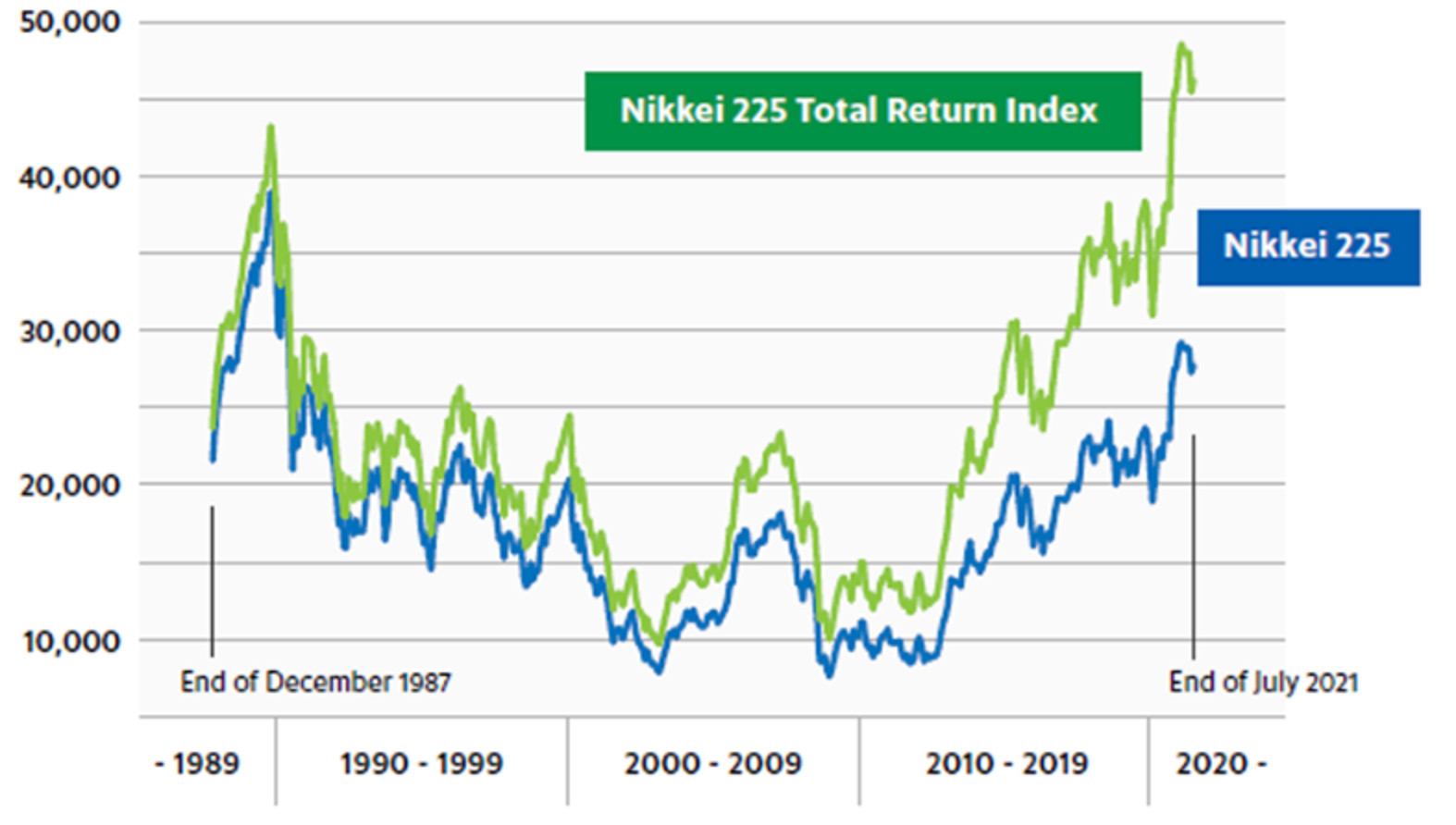

對於股票投資者來說,日元走弱在短期上漲。日經 225 指數升至數十年來最高水平,受到出口龐大的股票和海外盈利不預期的支撐。

然而,這有代價:消費者信心下降,通脹預期正在上升。在全球範圍內,日元的柔軟促進風險願望,這是股票甚至加密貨幣的燃料,但如果東京或日本央行突然改變立場,市場容易遭受大幅修正。

對於零售交易者來說,這種波動性同等地帶來機會和風險。由於關鍵水平周圍的波動率高,有紀律的頭寸規模和保證金跟踪成為必不可少的工具-例如 德里夫計算器 可以幫助交易者在進入市場之前估計點值,合約大小和潛在的利潤或虧損。

專家展望

美元/日元的預測取決於時間。如果日本央行在 12 月將利率提高至 0.75%,正如極少數經濟學家所預期的那樣,日元可能會將救濟反彈回升至 150。

但是,如果中央銀行延遲,並且美國數據保持穩定,交易者可能會繼續測試該範圍的上限。威靈頓 Altus 的詹姆斯·索恩表示:「佐奈高一的 Abenomics 風格的刺激措施將擴大全球流動性並加強美元-國王美元活得很好。」

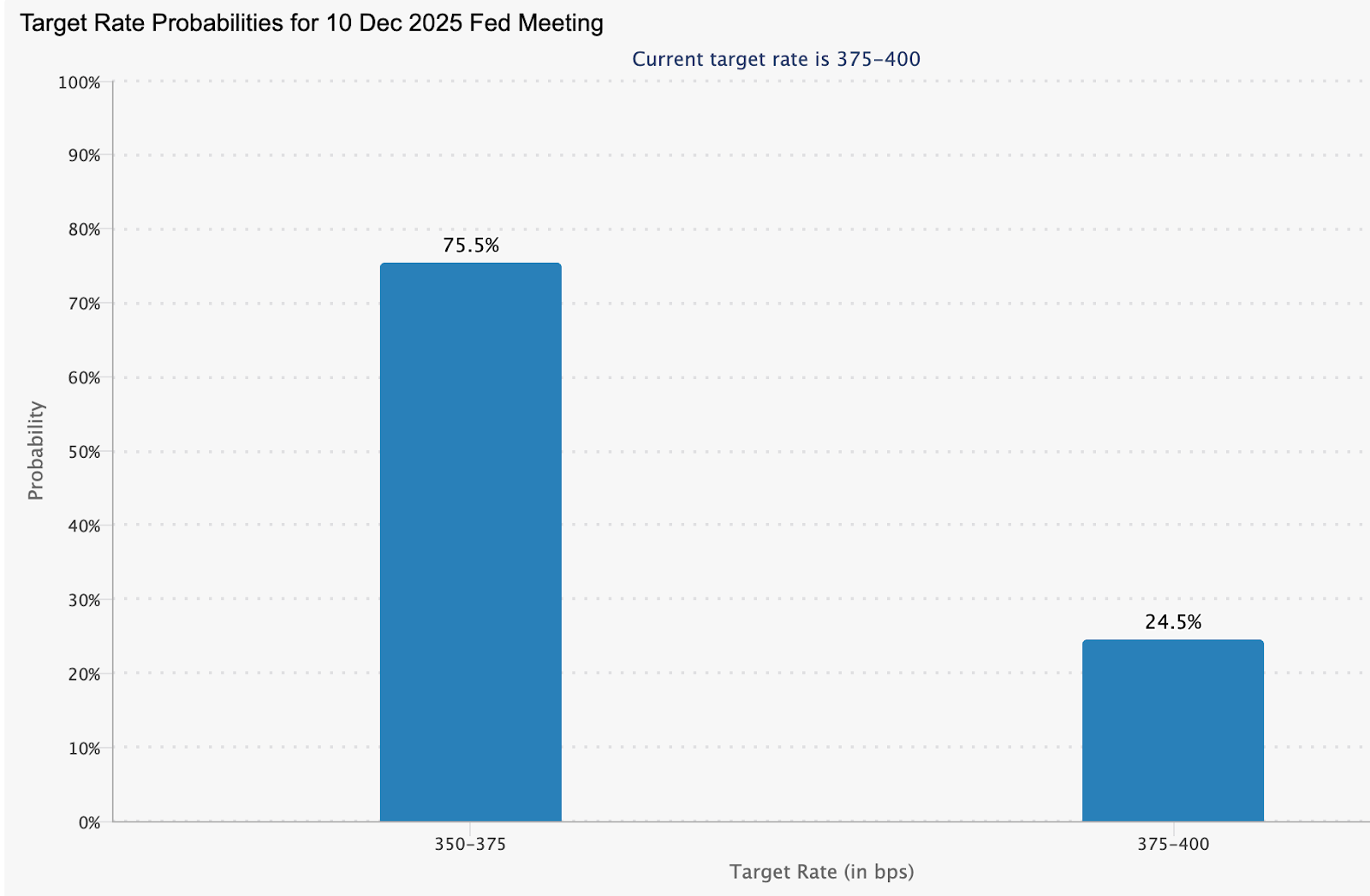

很大程度取決於美聯儲是否在日本央行之前轉移。期貨市場目前在 12 月份美國下跌的機率有 75.5%。

分析師還補充說,一個多姿 美聯儲 可能縮小收益差距並觸發日元買入。但如果沒有這一點,日本的貨幣仍然是政策慣性和全球情緒的人質。美元/日元維持在 160 附近的時間越長,東京對證明它仍然受到市場尊重的壓力就越大。

美元/日元技術分析

在撰寫本文時,美元/日元接近 156.66,在延長後在價格探索區內整合 看漲 跑。布林格帶(10,收盤)正在擴大,由於價格走勢保持接近上帶,因此價格走勢仍然接近上帶,這是強勁看漲勢頭的跡象,但也增加了短期耗盡的風險。

主要支撐區位於 154.00、150.00 和 146.60,其中跌破每個區域可能會觸發售清盤和更深入的修正。在上行方面,價格在 156.00 以上的價格發現留了有限的阻力,這意味著下一次回調可能會吸引下跌買家,除非波動性激增。

自動化學習 (14)正在攀升進入超買區域,表明看漲勢力可能已接近最高。如果 RSI 維持在 70 以上的讀數,動力可能會延續更高;但是,任何低於此水平的反轉可能表明未來獲利或早期賣出壓力。

關鍵外賣

根據分析師的說法,美元/日元的回歸 155—160 走廊不僅僅僅是圖表模式;這是關於日本政策組合的公民投票。未配合貨幣調整的財政擴張使日元脆弱,投資者懷疑。干預可能會短暫地穩定市場,但只有決定的收緊或財政限制才能恢復信心。在此之前,這對貨幣對於危險區域中,每一次更高的走勢不僅測試東京的寬容性,而且世界對日本控制自己的貨幣能力的信心。

Nvidia 極佳財報卻遭市場冷遇

儘管 Nvidia 業績大幅增長,並將下季指引上調至約 650 億美元,市場反應卻異常冷淡。

當 Nvidia Corporation 公布第三季營收達 570 億美元——年增 62%——看似又一次在 AI 硬體競賽中完美勝出。然而,儘管業績大幅增長並將下季指引上調至約 650 億美元,市場反應卻異常冷淡。

在一場外洩的全員會議中,執行長黃仁勳坦言:「市場並不領情。」這種執行力與市場熱情之間的落差,顯示出高漲的預期與 AI 狂熱已經將標準推高,即使是表現最優異的公司也難以令人驚艷。

推動 Nvidia 極佳財報的動力

Nvidia 業績的命脈仍然是資料中心需求——AI 基礎設施的支柱。該部門單季就創造了約 510 億美元營收,年增 66%,季增 25%。

Blackwell 平台等旗艦產品持續主導企業訂單,而最新指引預示下一季將再創新高——營收 650 億美元,年增 65%。Nvidia 不僅在成長,更是在為整個產業的資本支出週期定下節奏。

地緣政治與結構性力量進一步推升成長。隨著雲端、機器人與自動化系統在全球擴展,Nvidia 硬體成為創新的核心——同時也是供應的瓶頸。但成功也帶來脆弱:當完美成為常態,任何微小的波動都會被放大。「當你讓市場習慣於完美時,」一位分析師打趣道,「即使表現優異也不夠好。」

為什麼這很重要

Nvidia 現在約佔 S&P 500 總權重的 7.31%,成為 AI 情緒最具影響力的指標。如此巨大的股票在創紀錄財報後橫盤,意味著投資人質疑的不是數據,而是敘事。

FinancialContent 稱這是「AI 與更廣泛市場的關鍵時刻」。如果 Nvidia 的卓越表現已無法激起熱情,其他科技股也將感受到寒意。

黃仁勳自己說得很直白:表現不好會被指責戳破泡沫,表現太好又被說是在推高泡沫。這種認知陷阱凸顯 AI 交易進入新階段——只有超越卓越的表現才能撼動市場。這也反映出一種微妙的轉變:從炒作與承諾,走向紀律與交付。

對科技與 AI 生態系的影響

Nvidia 財報最初帶動整體科技股上揚,AMD、Broadcom 及記憶體供應商也受惠於樂觀情緒。但隨著交易日推進,漲幅逐漸消退——證明市場熱情已變得脆弱。

分析師指出,如果如此亮眼的業績不再引發漲勢,代表 AI 基礎設施的成長已大致反映在股價上。投資人現在可能更重視營運效率,而非單純擴張。這是自然的演變:當成長趨於成熟,估值紀律就會主導。

對硬體買家與企業用戶而言,這種演變可能意味著供應條件略為寬鬆,但價格壓力加大。Nvidia 的挑戰將是如何在擴大產能的同時維持利潤率——從願景式成長轉向工業級精準。

專家展望

市場觀察者認為,未來有兩條路。若 Nvidia 能持續執行——擴展新產品線、擴大製造能力、並妥善應對出口風險——就能維持領先並延續成長。公司依然擁有少數對手能企及的技術護城河。

另一種情境則是估值重置:如果投資人開始質疑硬體成長是否能無限超越成本膨脹與競爭,Nvidia 可能面臨停滯。正如 Bernstein 一位分析師所言:「至少就這份財報來說,我不知道還能要求什麼。」

對交易者而言,值得關注的訊號包括指引趨勢、訂單積壓(特別是中國市場)以及 Rubin 和 Blackwell 晶片的推進速度。市值在數週內波動五千億美元,顯示市場情緒已極為敏感。

Nvidia 技術面解析

截至撰文時,Nvidia (NVDA) 股價約在 $194.50,從下方 Bollinger Band 反彈,先前曾測試 $179.70 支撐位。Bollinger Bands(10,收盤)正適度擴大——顯示波動性上升——價格行為正靠近中線。這暗示短線有望繼續向上測試上軌。

$173.20 是下一個重要支撐位;若跌破,可能引發賣壓加劇並擴大下行動能。相反地,$208.00 則形成強大壓力區,若漲勢延續,獲利了結與末端 FOMO 買盤可能同時出現。

動能指標進一步強化多頭觀點。RSI(14)急劇上揚,突破中線 50——這是買盤壓力回升的技術訊號。若能持續站穩該水準,並穩定於 $179.70 之上,將有助於短線多頭趨勢,吸引關注動能操作的交易者。

對於規劃情境的投資人,Deriv calculator 可用於模擬不同波動性下的盈虧——這是規劃 NVDA 於 Deriv MT5 交易時,圖表分析的重要輔助工具。

重點總結

投資人認為 Nvidia 仍是 AI 基礎設施熱潮的核心——財務無可匹敵,技術領先。然而,市場冷淡的反應標誌著轉折點:投資人不再只看承諾,而是要看證據。在 AI 交易的新階段,執行力、利潤韌性與創新節奏將決定領導地位。對交易者而言,Nvidia 的技術圖表或許預示短線上行,但更大的故事是預期的轉變——完美已成為新常態,而非驚喜。

黃金價格展望:央行提供支撐底部

在利率降息預期減弱和美元走強的喧囂之下,隱藏著一股更深層的結構性力量:全球央行持續不斷的黃金買盤。

據報導,黃金在每盎司約4,050美元附近的驚人穩定並非偶然。在利率降息預期減弱和美元走強的喧囂之下,隱藏著一股更深層的結構性力量:全球央行持續不斷的買盤。從北京到安卡拉,政策制定者正悄悄改寫貨幣安全的規則,利用黃金作為對抗政治風險、貨幣不穩定及對美國金融秩序信任減弱的避險工具。

分析師指出,這股需求已成為支撐黃金的無形之手。即使投機交易者撤出,ETF 資金流趨於平緩,主權買家仍在幫助穩定市場。

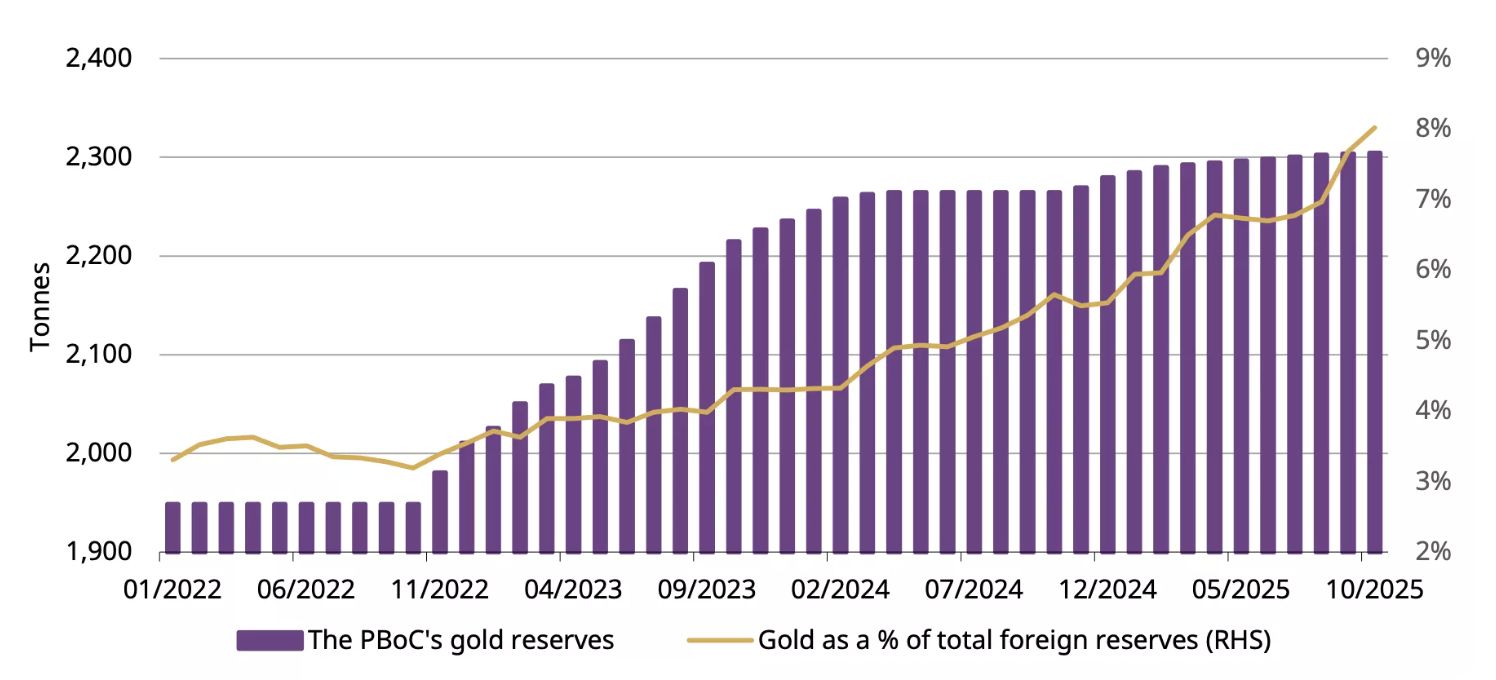

隨著中國人民銀行延續其連續12個月的黃金購買紀錄,其他央行也紛紛跟進,黃金的下行風險如今更像是暫停而非崩盤——這是一個由國家而非基金加強的底部。

目前推動黃金的因素是什麼?

最新的美國就業數據已重新設定全球市場的預期。9月非農就業報告顯示新增11.9萬個職位,超出經濟學家預期的兩倍多,而失業率微升至4.4%。

表面上看,數據呈現混合訊號——強勁的招聘但動能放緩——然而這足以促使投資者調低對聯邦儲備局12月降息的預期。

這一調整推升了美元和美國公債殖利率,這通常對黃金來說是有害的組合。但黃金幾乎沒有動搖。原因在於央行需求改變了黃金對政策週期的敏感度。

根據世界黃金協會的數據,官方部門的購買現在佔年度需求的近四分之一——這是十年前的結構性轉變。當聯準會猶豫時,央行卻不會。

中國人民銀行已連續12個月報告黃金購買,10月增加0.9噸,總量提升至2,304噸,佔中國外匯儲備的8%,標誌著連續一整年的持續買入。土耳其、波蘭和印度也加入了累積黃金的行列。

為何這很重要

市場觀察者表示,這種低調的主權累積正在重塑黃金在全球金融體系中的角色。過去被視為“避險”交易的黃金,現在成為國家儲備策略的一部分。2022年俄羅斯外資資產凍結事件促使各國政府重新評估其對美元主導體系的曝險,黃金因此成為一種中立的替代選擇。

正如Zaner Metals策略師Peter Grant所言,最新的美國就業數據“證實市場放緩但穩定——但這並未減少對安全性的需求。”

對新興市場的政策制定者而言,黃金提供了紙本資產無法比擬的保障:免受制裁、通膨及貨幣政治的影響。對投資者來說,這意味著黃金價格不再僅僅是利率或風險偏好的函數。它是一個地緣政治指標——反映當前貨幣秩序中剩餘信任的鏡子。

對市場與投資者的影響

本輪週期中最顯著的變化是,儘管美元指數(DXY)交易於數月來的最高點,黃金仍維持在接近歷史高位。傳統的反向關係已經減弱。分析師指出,兩種資產的購買原因相同:安全性。這一動態挑戰了黃金僅在利率下降時才反彈的觀念。

對交易者而言,這使短期持倉變得複雜。黃金目前約比10月的4,380美元高點低7%,動能已降溫,但結構性需求依然存在。ETF 資金流近週雖略為負面,卻無恐慌跡象。

散戶投資者已減少持倉,但官方部門已取代他們成為邊際買家。對長期投資者而言,這一轉變意味著回調可能是機會而非警訊,尤其是在宏觀經濟不確定性延續至2026年時。

專家展望

分析師對央行買盤能將黃金推升多遠仍有分歧。高盛仍視近期疲軟為“短暫現象,非反轉”,並維持主權及私人投資需求將支撐價格至2026年。瑞銀預計,若持續從美元儲備多元化,未來兩年內黃金可能攀升至每盎司4,900美元。

該展望的主要風險在於貨幣政策的自滿。如果美國數據保持強勁,聯準會重申“高利率長期存在”立場,投機興趣可能進一步減退。但目前,黃金的韌性已說明一切。市場正在調整至一個新現實——由央行而非交易者主導基調。

黃金技術面洞察

撰寫本文時,黃金(XAU/USD)交易於約4,030美元區域,徘徊於4,020美元支撐位附近。RSI 指標平緩且接近中線,顯示缺乏明顯動能,反映市場猶豫不決。

同時,Bollinger Bands 開始收窄,反映近期波動性降低。價格在中軌附近震盪,暗示可能進入盤整階段,等待下一次突破。

上方阻力位仍在4,200美元及4,365美元,交易者可能在此獲利了結或若多頭情緒回歸則重新買入。相反,若跌破4,020美元,可能打開通往3,940美元支撐的空間,屆時賣壓或清算壓力可能加劇。

重點摘要

2025年底黃金的韌性並非謎團——這是分析師們表達的信息。曾經信任美國國債的機構,現在轉而購買黃金以對沖政策、政治及不確定性風險。交易者或許會淡化這波漲勢,但央行毫不動搖。隨著Fed在分歧的政策前景中航行,全球儲備持續向東轉移,黃金的支撐底部看來與持有者的決心一樣堅實。

.png)

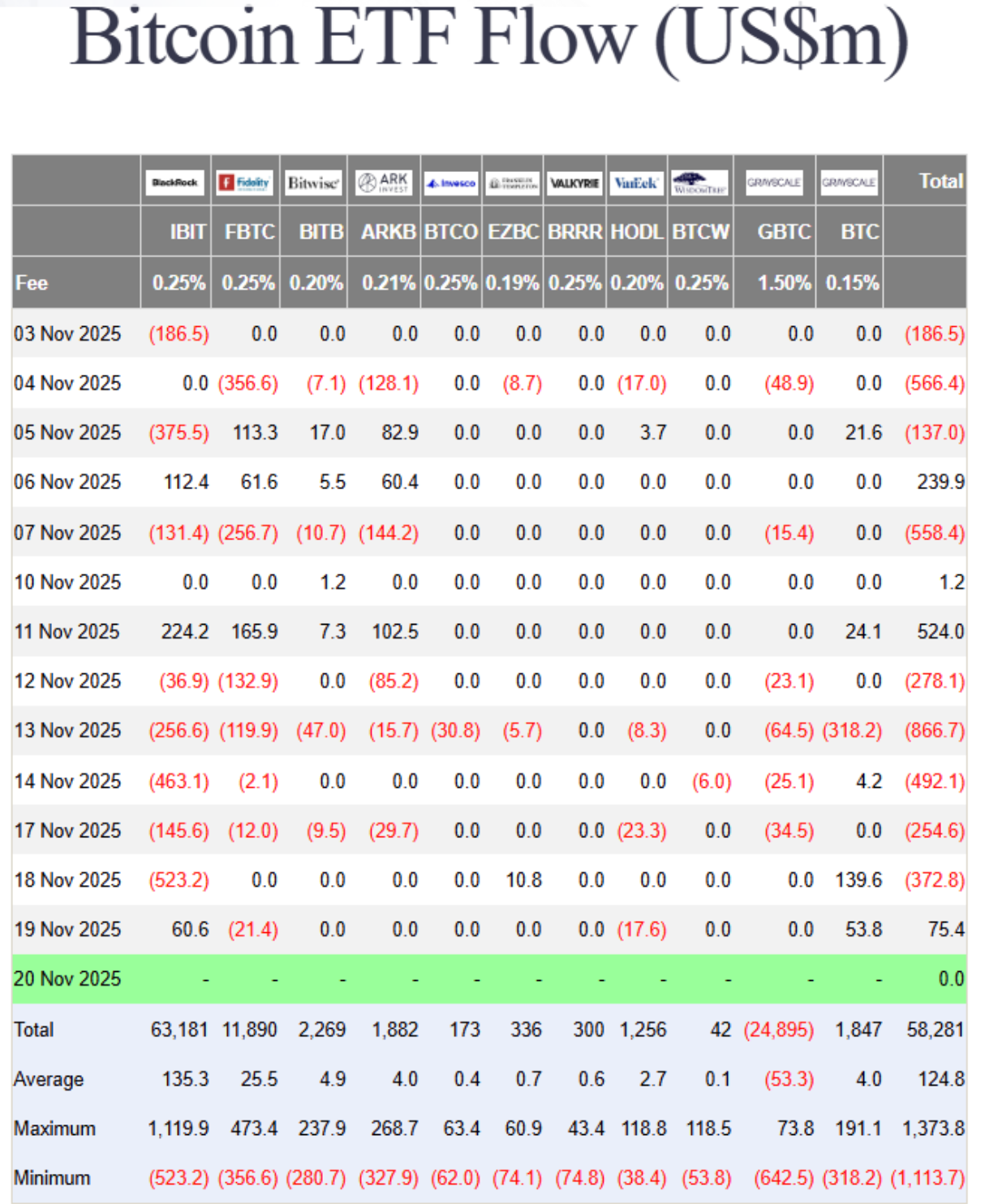

比特幣的嚴峻重置:資金流動、恐懼與兩條關鍵線

這個全球最大的加密貨幣自十月高點以來已下跌近三分之一,隨著逆風生效,價格正滑向關鍵技術水平。

比特幣的嚴峻重置已經到來。這個全球最大的加密貨幣自十月高點以來已下跌近三分之一,隨著交易所交易基金(ETF)資金流出和宏觀經濟逆風生效,價格正滑向關鍵技術水平。

最新數據顯示,僅本月比特幣ETF就流出了近30億美元,曾經推動漲勢的機構資金流如今轉變為贖回和撤退的反饋循環。

這波拋售背後是聯準會(Fed)降息希望減弱、流動性收緊,以及市場被“極度恐懼”癱瘓的混合因素。隨著價格徘徊在約85,600美元附近,且一年低點74,000美元逼近,問題簡單卻緊迫:這次修正是短暫的洗盤,還是比特幣新ETF時代更深層次轉變的開始?

推動比特幣修正的原因

分析師指出,比特幣30%的下跌並非由醜聞或突發事件引起,而是結構性力量終於逆轉的結果。經過兩年的持續流入,現貨比特幣ETF現在正面臨資金流出。曾被譽為加密穩定器的機構投資者,正展現出市場動盪時情緒轉變的速度之快。

根據Farside數據,本月除四天外,ETF均出現贖回,淨流出近30億美元。

部分撤退源於宏觀條件的變化。聯邦儲備系統(Federal Reserve)不願確認降息,強化了美元,吸引流動性遠離投機性資產。

過去的走勢顯示,美元走強通常會壓制比特幣,且通膨數據仍然頑固,交易者正在重新評估12月“寬鬆貨幣”回歸的敘事。結果是市場對反彈反應以賣壓居多,而非熱情——這與數週前推動比特幣飆升至126,000美元的狂熱形成鮮明對比。

為何這很重要

比特幣的拋售揭示了傳統市場與數位市場如今緊密交織的程度。ETF為機構曝險打開了閘門,但同時也將比特幣與更廣泛的風險趨勢連結起來。當投資者從ETF產品撤資時,這種影響會在流動性池和市場情緒中產生連鎖反應。

Luxor的Matt Williams解釋說:“跌至86,000美元主要是由宏觀因素驅動——利率預期、通膨——以及大戶在跌破關鍵技術支撐後減少曝險。”

對交易者而言,這是一個心理轉折點。曾在2017年感恩節期間湧入交易所、推動比特幣首次突破10,000美元的散戶群體,如今大多保持沉默。

Santiment的社交數據顯示,市場情緒在預測跌破70,000美元與對反彈至130,000美元的狂熱樂觀之間均分。這種分歧反映的是猶豫不決,而非堅定信念。在此階段,恐懼而非基本面主導市場氛圍。

對市場與投資者的影響

這波拋售已蔓延至加密領域之外。比特幣與股市指數如納斯達克100的相關性有時超過0.8,意味著科技股與數位資產的走勢現今受相同宏觀因素影響。當利率樂觀情緒消退,兩個市場均受挫。這種連結挑戰了比特幣作為貨幣風險對沖工具的長期主張。

ETF資金流出是另一個壓力點。隨著基金被贖回,流動性提供者被迫在期貨和現貨市場平倉,進一步加劇波動性。

本週加密恐懼與貪婪指數跌至14,為2月以來最低,凸顯情緒惡化速度之快。BTC Markets的Rachael Lucas警告,動能、資金流和成交量趨勢“均反映出情緒急劇惡化”,這是由宏觀收緊和風險規避所驅動。

在背後,流動性提供者正苦苦掙扎。Fundstrat的Tom Lee將加密市場做市商比作數位流動性的“中央銀行”——而目前這些銀行正面臨枯竭。

繼十月200億美元的清算浪潮後,做市商的資產規模縮小,限制了他們吸收訂單流的能力。這提醒我們,加密市場的基礎設施雖然更先進,仍然脆弱。

專家展望

分析師在謹慎與好奇之間搖擺。Coin Bureau的Nic Puckrin形容當前局勢為“牛熊拉鋸戰”,宏觀經濟悲觀情緒被科技板塊的韌性所抵消。

Nvidia的財報超預期短暫提振風險偏好,但比特幣未能跟進,顯示交易者仍在減倉而非加倉。Puckrin將下一阻力位定在107,500美元,若反彈能獲得動能則有望挑戰。

Bitwise的Andre Dragosch認為此輪下跌與過去中期調整相似,指出此次跌幅和持續時間“與先前牛市中的階段性回調相符”。他的基本預期仍是該週期將延續至2026年,受全球貨幣逐步寬鬆推動。

不過目前短期風險仍偏向下行,85,600美元和74,000美元是兩個關鍵觀察點。守住這兩線,比特幣可能築底;失守,下一波洗盤可能迅速來襲。

更大格局:比特幣會引發金融危機嗎?

儘管市場恐慌,比特幣相較於真實金融體系仍屬小規模。整體加密市場約為3至4兆美元,比特幣約占一半。相比之下,全球金融資產超過400兆美元。過去如2022年FTX和2021年Terra崩盤,雖在加密產業內造成混亂,卻幾乎未波及全球市場。

不過,每個週期都讓加密更接近傳統金融。ETF、企業持有和以美國國債支持的穩定幣已建立實質連結。嚴重的比特幣崩盤可能引發ETF贖回,損害持有BTC企業的資產負債表,並迫使穩定幣清算其國債資產。這些情況今日尚不足以引發2008年式的危機——但隨著重疊加深,“加密崩盤”與“金融傳染”之間的界線正日益模糊。

比特幣技術分析

撰文時,比特幣(BTC/USD)在長期下跌後約於84,200美元交易。相對強弱指標(RSI)急劇跌入超賣區,顯示強烈的空頭動能,若買方介入,短期內可能出現反彈。

死亡交叉——50日均線跌破200日均線——加強了看跌偏向,暗示近期可能有進一步下行壓力。

關鍵阻力位分別在106,260美元、115,200美元和123,950美元,若反彈嘗試出現,交易者可能在這些區域獲利了結或重新買入。若無法收復這些區域,比特幣將持續承壓,市場情緒在持續賣壓中保持脆弱。

主要結論

比特幣的下跌並非意外,而是其新現實的壓力測試。ETF時代使這種加密貨幣與全球金融體系更緊密相連,既有利也有弊。流動性曾是順風,現在卻成為雙刃劍。恐懼主導市場,但深度修正是比特幣的DNA之一。

如果那兩條線——85,600美元和74,000美元——能堅守,許多人認為這次重置可能只是下一波機構需求前的又一次清洗階段。若失守,比特幣的嚴峻重置可能演變成更深層的調整。

Nvidia earnings reality check: Is the AI boom back on track?

Nvidia’s latest earnings didn’t inflate another round of hype; they restored confidence that artificial intelligence is entering its scale phase.

Yes - the AI boom is back on track, according to analysts, just in a different gear. Nvidia’s latest earnings didn’t inflate another round of hype; they restored confidence that artificial intelligence is entering its scale phase, not its speculative one.

Nvidia investors are bracing for a $300 billion surge in market value after the chipmaker reported its first sales acceleration in seven quarters, signalling that AI demand isn’t fading - it’s normalising into a sustainable growth cycle.

For months, markets were haunted by talk of “peak AI.” However, Nvidia’s results - record data centre revenue, renewed partnerships, and a 5% share spike in after-hours trading - show the story isn’t one of collapse, but calibration. This isn’t a bubble bursting; it’s the industry learning how to breathe again.

What’s driving Nvidia’s momentum

At the core of Nvidia’s dominance in artificial intelligence architecture is its data centre segment, which surpassed $50 billion this quarter, a milestone reached earlier than analysts expected.

This reflects an industrial-scale buildout, not a speculative frenzy. The surge in demand from AI workloads has transformed GPUs from niche products into the backbone of modern computing, powering everything from ChatGPT to enterprise cloud systems.

CEO Jensen Huang captured it best: “We’re in every cloud.” That ubiquity underpins Nvidia’s stability. Its chips are not optional - they’re essential infrastructure. With Blackwell GPUs offering up to 40 times faster inference speeds than the previous generation, the company isn’t chasing hype; it’s engineering the next leap in computational efficiency.

Why it matters

Nvidia’s report acts as a barometer for the AI economy. The stock’s post-earnings rally wasn’t just about profits; it was about validation. The market had priced in fear after days of tech sell-offs, but Nvidia’s blowout numbers reintroduced realism.

Analysts like Julian Emanuel of Evercore ISI summed up the pre-earnings tension: “The angst around ‘peak AI’ has been palpable.” Those fears evaporated when Nvidia showed that demand isn’t flattening - it’s broadening.

The company’s performance has become closely tied to the trajectory of U.S. equities. With AI now a structural growth driver, Nvidia’s consistency reassures investors that this is an economic revolution in progress, not a fleeting mania. Its $5 trillion valuation last month wasn’t an aberration; it was a preview of scale yet to come.

Impact on global markets

The aftershocks were immediate. Tech indices that had stumbled under the weight of “AI fatigue” rebounded as Nvidia reignited investor faith. Asian markets opened higher, and S&P futures turned positive, driven by renewed conviction that the AI trade still has legs. Even after a period of correction - Meta down 19%, Oracle off 20% - Nvidia’s performance reaffirmed that the long-term AI thesis remains intact.

Beyond markets, Nvidia’s results signal a new capital cycle. Its multibillion-dollar partnerships with Microsoft, OpenAI, and Anthropic aren’t one-off investments; they’re structural commitments to an AI-driven infrastructure era. Every dollar of GPU spending feeds into an ecosystem that’s building capacity for the next generation of models, data centres, and intelligent services.

Expert outlook

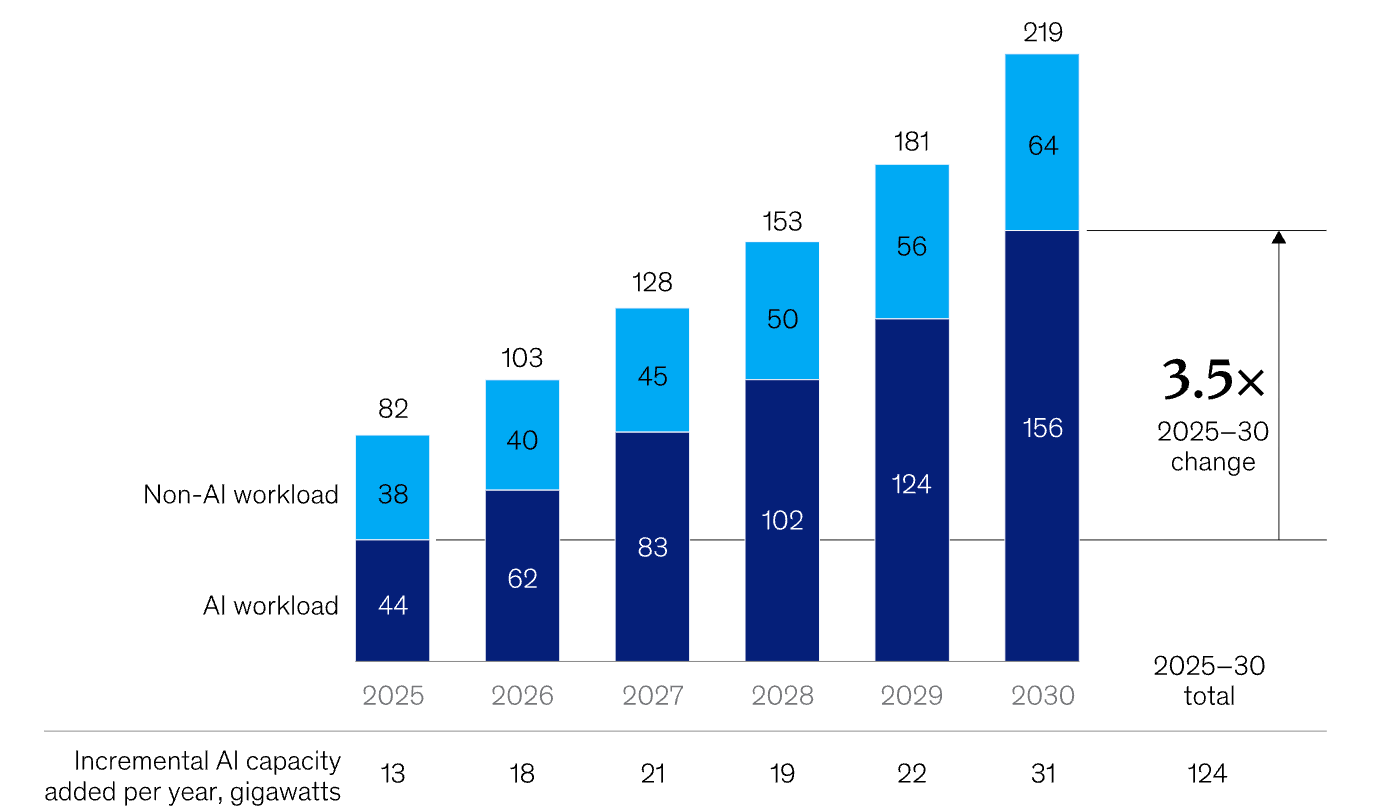

Forecasts are being rewritten. McKinsey estimates $7 trillion in AI infrastructure spending by 2030, with $5.2 trillion going toward data centres. According to McKinsey, we will also see significant incremental AI capacity added every year through to 2030.

Nvidia’s share of that pie could exceed 50%, given its current dominance and design lead. Some analysts even project a $20 trillion market capitalisation by 2030 if the company maintains its pace of innovation.

Still, this is not a frictionless ascent. Export restrictions to China and the rise of custom silicon from rivals like AMD and Google pose challenges. Yet Nvidia’s edge isn’t just its hardware - it’s the CUDA software ecosystem, which locks developers and enterprises into its platform. As long as AI workloads require versatility and performance across models and frameworks, Nvidia’s moat will hold.

Nvidia technical analysis

At the time of writing, Nvidia’s stock (NVDA) is hovering around $186, showing early signs of recovery after a short-term pullback. The RSI is rising sharply from the midline near 50, indicating that bullish momentum may be building as buying pressure intensifies.

Meanwhile, the Bollinger Bands are starting to narrow slightly, signalling a potential volatility squeeze that could precede a directional breakout. The price is currently positioned around the middle band, indicating a balance between buying and selling forces.

On the downside, support levels lie at $180 and $168. A drop below $180 may trigger further selling or stop-loss liquidations, while a break under $168 could confirm a deeper correction. On the upside, the key resistance sits at $208, where profit-taking and fresh buying activity are likely to intensify if the price breaks above it.

Key takeaway

Nvidia’s potential $300bn surge isn’t a sign of euphoria - it’s a reality check for those betting on an AI crash. The company’s results confirm that artificial intelligence has moved beyond the phase of promise into proof. As capital shifts from prototypes to platforms, the question isn’t whether AI will endure - it’s how fast it will reshape every market it touches. For now, Nvidia remains the pulse of that transformation.

For traders navigating that transformation, platforms like Deriv MT5 offer exposure to the tech rally’s next phase - while tools such as the Deriv trading calculator provide the precision to manage risk as the AI-driven market matures.

Sanctions vs supply glut: The battle defining Oil prices

Oil prices are caught in a tug-of-war that defines the entire energy narrative right now - sanctions versus surplus.

Oil prices are caught in a tug-of-war that defines the entire energy narrative right now - sanctions versus surplus. As Washington’s latest restrictions on Russian oil giants, such as Rosneft and Lukoil, take effect, traders are wondering whether this will finally squeeze supply enough to lift prices or if swelling inventories and record U.S. output will keep them grounded.

WTI crude has hovered near $60 in recent sessions, reflecting that same indecision. Every headline about sanctions sparks a flicker of optimism; every inventory report snuffs it out. The outcome of this standoff - between geopolitics and fundamentals - will decide whether oil’s next move is a breakout or another false dawn.

What’s driving the rebound

According to analysts, the recent oil bounce is largely fuelled by heightened concern over Russia’s export flows. In a press release issued by the U.S. Department of the Treasury, the United States and allied countries have imposed sweeping sanctions targeting major Russian oil producers, including Rosneft and Lukoil, along with hundreds of vessels from the “shadow fleet”.

These measures are designed to choke off Russia’s oil revenues and, by extension, reduce its export volumes. The logic is simple: fewer barrels from Russia = tighter global supply = higher prices. But the counter-force is significant: global supply remains robust, and demand isn’t bouncing back as expected.

According to the International Energy Agency (IEA), non-OPEC+ production is forecast to grow by 1.7 million barrels per day (bpd) in 2025, while demand growth is projected at just 0.79 million bpd, signalling a structural surplus unless changes occur.

Meanwhile, data show that Russia’s output and export adapt-workarounds remain effective so far - Russian production rose by about 100,000 bpd even after sanctions. Thus, the rebound is caught between a genuine supply shock narrative and a stubborn demand/stock overhang, and whether prices break out depends on which side prevails.

Why it matters

For traders, producers and consumers, this dynamic is far from academic. A sustained rally driven by supply constraints would favour oil-heavy portfolios, refining margins, and exporting nations. Conversely, if oversupply persists and demand disappoints, even the sanction narrative won’t save prices. As one senior energy analyst noted: “The market doesn’t expect much lost supply until enforcement becomes indisputable.”

For Russia and its global buyers, the stakes are high. Russia’s oil and gas revenues plunged by 27% in October 2025 compared to the same month a year earlier, reflecting the pressure of sanctions even as volumes held up through workarounds.

At the same time, major oil importers such as India and China have been increasing their Russian cargoes in recent months before the November plunge, which has cast doubts about continued oil flows to those countries.

So, if importers continue to absorb discounted Russian barrels, global supply may remain ample even though the narrative suggests otherwise. On the consumer end, if oil prices are kept low due to oversupply, fuel costs remain manageable. If supply loss dominates, refined-product prices (diesel, gasoline) could rise, feeding inflation and impacting economic growth - a risk to be watched for in both developed and emerging markets.

Impact on the market

In practical terms, the battle lines are drawn according to analysts. On the supply-risk side, if sanctions bite and Russian exports drop materially, markets may tighten quickly, and oil prices could rally.

The risk premium is already reflected in crude spreads: the discount for Russian Urals crude versus global benchmarks jumped to around US$19 per barrel by early November, as buyers shunned Russian cargoes, according to a report by Meduza. That suggests the sanction effect may be starting to crack.

But on the flip side, tracking data suggest that Russian flows are still being rerouted, and global producers (especially shale, Brazil and the U.S.) are responding. With U.S. production at record levels and inventories increasing, the oversupply story remains viable, according to industry commentators. If demand remains weak - for instance, from China or the global industry - then any supply-shock rally may be short-lived, and prices could retreat.

Refining and trade flows are also adjusting. Dealers and refiners are now considering discounted Russian crude, longer shipping routes, and higher freight and insurance costs - all of which increase complexity but don’t necessarily immediately reduce volumes. Until actual barrel losses show up in export data, the market may remain in limbo, reluctant to commit to strong upward momentum.

Expert outlook

According to analysts, the most probable scenario is a market stuck in a range-bound trading pattern, punctuated by bursts of volatility. That is, oil may temporarily rally on rumours of sanctions or supply disruptions, but unless demand proves stronger and supply genuinely tightens, the move may lack legs. Reuters reported that the IEA continues to expect supply growth outpacing demand this year.

If enforcement of sanctions tightens - for example, if shadow-fleet tankers are blocked, insurance costs spike or major importers pull back from Russian oil - then we could see a meaningful rally.

On the demand front, counter-signals to watch include refining run-rates (which remain under pressure), travel and mobility trends, and China’s petro-chemical demand. Until one of these breaks clearly favourably, the oversupply story will likely keep a lid on prices.

In short, the supply risk is real, but it hasn’t yet overridden the oversupply/weak-demand backdrop. Until that happens, the rally remains tentative.

Oil technical insights

At the time of writing, US Oil is trading around $59.50, consolidating within a narrow range as momentum starts to stabilise. The RSI is climbing sharply from the midline near 50, hinting at strengthening bullish momentum and suggesting that buyers may be regaining short-term control.

The Bollinger Bands (10, close) are relatively tight, signalling reduced volatility and the potential for a breakout. Price action remains centred around the middle band, showing indecision but with a slight upward bias as buyers attempt to push above the mid-range.

Key support levels are found at $58.26 and $56.85, where a break lower could trigger further selling pressure or stop-loss liquidations. On the upside, resistance sits at $62.00 and $65.00 - levels where profit-taking and stronger buying activity could emerge if the market breaks higher.

Key takeaway

The oil market is at a crossroads where the sanction-driven supply-risk narrative clashes with the solid structural reality of oversupply and weak demand. While the latest Russian sanctions have sharpened the risk premium, global production and inventories remain elevated and demand remains fragile.

Unless export losses are real and demand picks up, the oversupply story will likely keep oil prices pinned. The next key signals to monitor: export data from Russia, inventory changes globally and demand indicators from Asia and the U.S. Stay alert - this is a high-stakes battle that could tip either way.

For traders navigating the oil market, Deriv MT5 offers exposure to both WTI and Brent. Meanwhile, tools such as the Deriv trading calculator provide the precision needed to manage risk as the AI-driven market matures.

USD/JPY outlook: Can the Yen hold its ground amid Japan’s policy tug-of-war?

Reports indicate that the Japanese yen is struggling to maintain its stability as Japan’s fiscal and monetary priorities diverge in opposite directions.

Reports indicate that the Japanese yen is struggling to maintain its stability as Japan’s fiscal and monetary priorities diverge in opposite directions. A massive ¥25 trillion stimulus plan from Prime Minister Sanae Takaichi has reignited concerns about inflation and weighed on the currency, while the Bank of Japan’s cautious stance on rate hikes offers little support. The result is a yen pinned near a nine-month low, with the USD/JPY pair hovering around ¥155.

Many say Japan’s policy tug-of-war is tilting decisively against the yen. Unless the government and central bank find common ground, traders may see further weakness - especially if the dollar remains buoyed by a patient but firm Federal Reserve.

What’s driving USD/JPY

The yen’s weakness stems from a widening policy divide inside Japan’s leadership. Prime Minister Takaichi’s administration has revived Abenomics-style stimulus, prioritising fiscal expansion to boost wages and consumer demand.

Lawmakers have proposed a supplementary budget exceeding ¥25 trillion, stoking concerns over rising debt issuance and sending 40-year Japanese government bond yields to record highs.

Meanwhile, the Bank of Japan (BoJ) is caught between political pressure and macroeconomic caution. Inflation, currently around 2.9%, remains above target, yet the prime minister insists on keeping rates low until wage growth - not food or energy costs - drives price stability.

Governor Kazuo Ueda has hinted at tightening if inflation persists, but uneven growth complicates matters: GDP grew 1.1% year-on-year, yet contracted 0.4% quarter-on-quarter. This tug-of-war has left investors unsure whether Japan’s policies are reflating the economy or eroding its currency.

Why it matters

This internal conflict is redefining how global markets view the yen. Once seen as a safe-haven anchor, it’s now behaving more like a risk currency, moving with rather than against global sentiment. “Japan has added a tumultuous element - they’re a little more wild, a little more volatile,” said Juan Perez of Monex USA. That volatility reflects a new reality: fiscal expansion is now Japan’s dominant narrative, while monetary prudence takes a back seat.

For traders, the risk is that verbal intervention replaces actual action. Finance Minister Satsuki Katayama has expressed concern over the yen’s sharp depreciation, but Tokyo has so far refrained from stepping into the market. Intervention is likely only if USD/JPY breaches ¥156 decisively - a level seen as politically sensitive rather than economically critical by analysts.

Impact across markets

According to reports, the consequences of Japan’s fiscal-monetary split are evident across its bond and currency markets. The yield curve has steepened sharply as investors price in heavier debt issuance, while near-zero short-term rates keep domestic liquidity abundant. This imbalance encourages capital outflows, as investors seek higher yields abroad, further putting downward pressure on the yen.

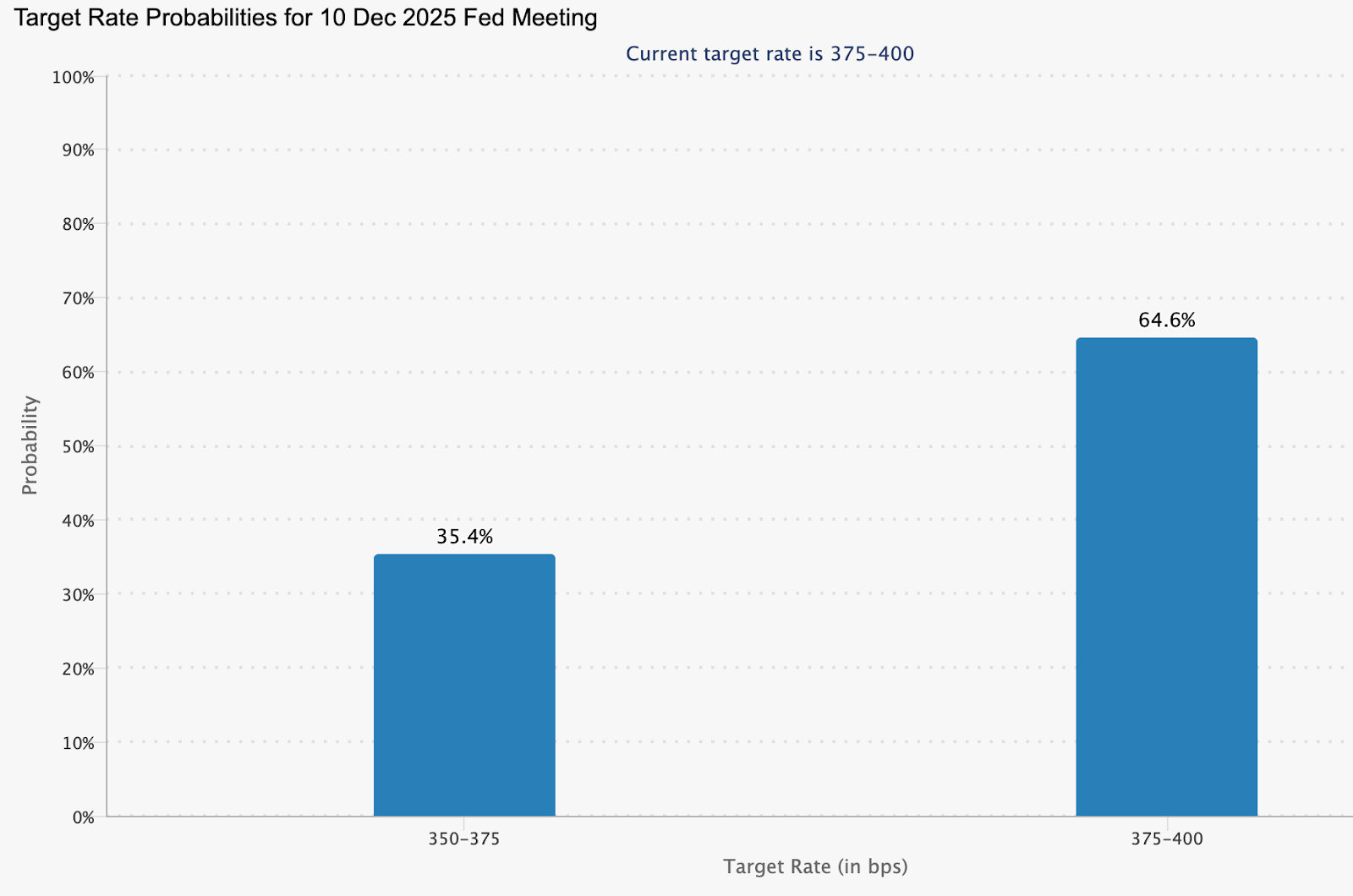

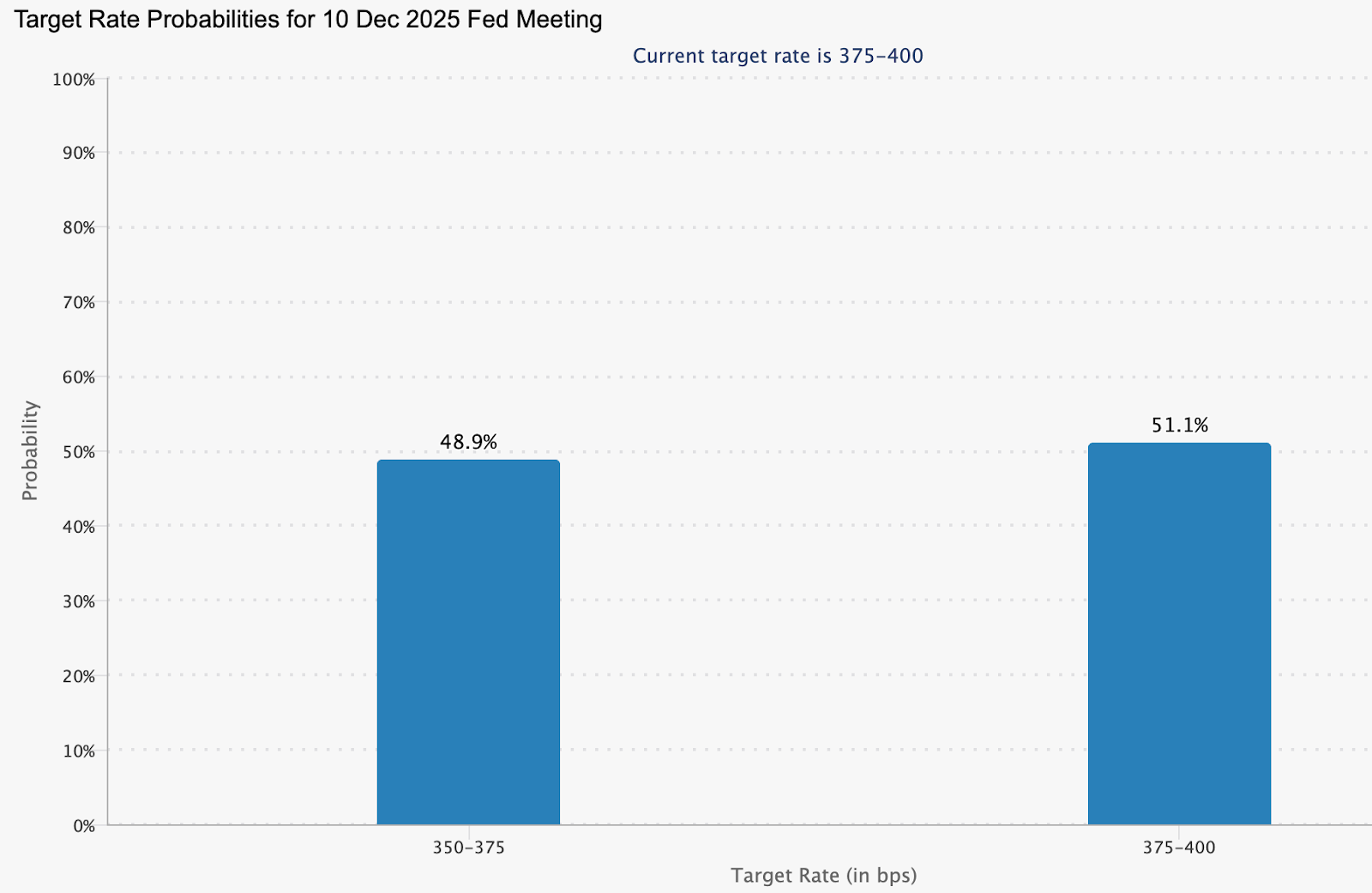

Across the Pacific, the Federal Reserve’s steadiness has reinforced dollar strength. Officials such as Philip Jefferson and Christopher Waller continue to advocate patience on rate cuts, trimming the probability of a December reduction to around 48%, down from 60% last week (CME FedWatch).

According to analysts, as long as this interest-rate gap persists, the dollar will remain structurally favoured against the yen, - and any yen rallies will likely prove temporary.

Expert outlook

Analysts see little relief for the yen in the near term. Barclays recommends holding a long position on the dollar against the yen, arguing that Takaichi’s expansionary agenda will suppress domestic yields and maintain downward pressure on the currency. Still, a sustained climb beyond ¥156 could test Tokyo’s resolve and force coordinated intervention.

The next key event is the delayed US Non-Farm Payrolls report, expected to provide fresh insight into labour market conditions. A weaker reading could trigger short-term dollar selling, allowing the yen to recover briefly. Yet without a policy shift in Japan, that reprieve may be short-lived. For now, the yen’s trajectory is dictated less by data and more by the dissonance between fiscal ambition and monetary caution.

USD/JPY technical insight

At the time of writing, USD/JPY is trading around 155.45, extending gains within a price discovery zone as bullish momentum persists. The pair is hugging the upper Bollinger Band, signalling strong buying pressure but also hinting at a possible overextension.

The RSI is climbing toward the overbought region, reinforcing the risk of a short-term pullback or profit-taking. Immediate support lies at 152.96, followed by 146.45, where a breakdown could trigger sell liquidations and accelerate downside movement.

However, as long as prices hold above the middle Bollinger Band and 153.00, the broader uptrend could remain intact, supported by policy divergence between the Federal Reserve and the Bank of Japan.

Key takeaway

Japan’s yen problem isn’t just about markets - it’s about messaging. Expansionary fiscal policy collides with a hesitant central bank, leaving investors unsure which signal to follow. The result is a currency under sustained strain, with verbal intervention doing little to stop the slide. Unless Tokyo finds alignment between stimulus and stability, the yen’s effort to hold its ground may remain more symbolic than successful.

Gold’s reversion to the mean: A pause before the next rally?

Gold has climbed back above $4,050 per ounce, stabilising after a sharp two-week selloff that pulled the metal down from record highs.

Gold has climbed back above $4,050 per ounce, stabilising after a sharp two-week selloff that pulled the metal down from record highs. The move reflects what analysts increasingly describe as a reversion to the mean - a natural correction following a steep run from $3,450 to $4,380 earlier in the quarter.

With the long-delayed US Non-Farm Payrolls (NFP) report now in focus, traders are watching whether this consolidation is a breather before the next leg up. The broader backdrop remains tense. Hawkish Federal Reserve remarks, delayed data from the US government shutdown, and continued geopolitical stress are all reshaping sentiment. Yet, behind the noise, gold’s pullback looks less like weakness - and more like equilibrium returning.

What’s driving gold’s mean reversion

The latest correction follows months of relentless buying, fuelled by soft US data, de-dollarisation flows, and record central-bank accumulation. Gold’s sprint from $3,450 to $4,380 outpaced fundamentals, leaving technical indicators stretched and sentiment euphoric.

Now, as traders recalibrate expectations for a December rate cut - pricing in a 48.9% chance according to CME FedWatch - the metal has slipped back toward its midrange, around $4,050–$4,100, where short-term and long-term averages converge.

This retreat also mirrors a psychological reset. Markets are digesting the Fed’s cautious tone, with Vice Chair Philip Jefferson urging a “slow approach” to policy changes and regional presidents Bostic and Schmid signalling preference for steady rates. Those comments, paired with delayed macro data, have thinned speculative positions and allowed gold to breathe. In effect, the market is rediscovering balance - a hallmark of mean reversion after an overextended move.

Why it matters

Gold’s mean reversion tells a deeper story about trust and monetary fatigue. As Citadel’s Ken Griffin noted, the rising price of gold reflects “a loss of trust first in US Treasuries, then in G7 bond markets.” Investors are responding not to short-term volatility, but to structural concerns about government debt and the stability of fiat currency.

Analysts at Deutsche Bank maintain that the medium-term trend remains intact, projecting an average gold price of $4,000 per ounce next year. They highlight “elevated official demand” - a reference to sustained central-bank buying.

In October, China’s central bank added 0.9 tonnes to its reserves, marking its 12th straight month of accumulation. Ongoing purchases throughout 2025 have lifted China’s official gold reserves to 2,304.5 tonnes.

This underlines that while traders may be reverting to the mean, nations are not - they’re steadily diversifying away from the dollar.

Impact across markets

In China, investor appetite for gold remains vigorous even during the correction. ETF inflows jumped RMB 32 billion (US$4.5 billion) in October, pushing total holdings to a record 227 tonnes.

Physical demand, measured by withdrawals from the Shanghai Gold Exchange, rose 17 tonnes year-on-year to 124 tonnes, defying seasonal softness. The data suggests that investors see dips as opportunities, not red flags.

Globally, the story is similar. Soft US employment data and climbing jobless claims have tempered the dollar’s strength, nudging investors back into gold and silver.

Still, there’s awareness that a stronger NFP print or easing geopolitical risk could stall momentum. Even so, mean reversion isn’t a bearish event - it’s the market’s way of restoring order after a speculative sprint. And order, in uncertain times, is the most bullish foundation of all.

Expert outlook

Most analysts agree that gold’s medium-term trajectory remains higher, although near-term volatility will hinge on the US jobs data and the Fed’s stance in December. Independent trader Tai Wong says, “soft data is slightly boosting hopes for a December cut - helping gold and silver, which are trying to break a three-day losing streak.” That sentiment captures the current equilibrium: cautious optimism tempered by macro prudence.

If the NFP report underperforms, gold could swiftly retest $4,200, according to analysts. If it surprises to the upside, a dip toward $3,950 would complete a textbook mean reversion cycle before stabilising. Either way, the long-term bull case - driven by de-dollarisation, AI-driven labour disruption, and inflation inertia - remains intact. The question isn’t whether gold rises again, but when.

Gold technical analysis

At the time of writing, XAU/USD is trading near $4,088, rebounding from the lower Bollinger Band as buyers re-enter the market. The Bollinger Bands are beginning to widen after a period of contraction, suggesting that volatility may be returning.

The RSI is rising sharply from the midline, signalling improving bullish momentum. Key resistance levels are seen at $4,200 and $4,365, where profit-taking or further buying could occur if gold breaks higher. On the downside, a fall below $3,940 would likely trigger sell liquidations, exposing deeper support at $3,630.

Overall, gold appears to be in the early stages of a potential bullish continuation, with the technical setup hinting at renewed upside pressure if momentum sustains above the mid-Bollinger Band.

Key takeaway

Gold’s pullback to the $4,000 zone isn’t weakness - it’s rhythm. A reversion to the mean after a parabolic rise is how sustainable trends reset. Beneath short-term volatility, the drivers of this bull phase - de-dollarisation, central-bank accumulation, and macro distrust - remain fully in play. As the US jobs data and Fed decisions unfold, this pause could mark the quiet before gold’s next major rally.

Bitcoin crashes under $90K as ‘death cross’ bites

Spot prices printed as low as 89,420 dollars, the weakest level since February, only six weeks after setting a record near 126,250 dollars.

Bitcoin slipped below 90,000 dollars on Tuesday, extending a selloff that has erased its 2025 gains and pushed sentiment toward the bleak end of the spectrum. Spot prices printed as low as 89,420 dollars, the weakest level since February, only six weeks after setting a record near 126,250 dollars.

The breakdown coincided with a bearish technical crossover known as a death cross and increasingly hesitant fund flows into U.S. spot ETFs.

Together with macro anxiety around the rate path, these factors have tightened liquidity and amplified swings across majors. The next phase hinges on whether price can quickly reclaim lost support and whether ETF prints stabilise from recent choppiness.

What’s driving the slide

The proximate trigger is technical: Bitcoin fell back through reclaimed support near 93,700 dollars, lost its 200-day moving average, and then registered a death cross as the 50-day slipped beneath the 200-day.

On its own the signal is imperfect, but in weak liquidity regimes it often coincides with multi-week drawdowns as momentum traders de-risk.

Flows add fuel. U.S. spot ETF activity has turned choppy after heavy intake earlier in the year, with trackers showing sequences of outflows or flat prints that blunt marginal demand. When the incremental demand fades, price tends to chase lower liquidity pockets until new buyers emerge. Recent dashboards corroborate the stop-start nature of ETF demand. CoinDesk+1.

The Mt. Gox repayments - a trigger, not the cause

Adding fuel to the fire, over 10,600 BTC (worth roughly $953 million) were transferred from Mt. Gox wallets on 18 November 2025, marking the first such movement in eight months.

The long-running repayment saga, stemming from the 2014 collapse of the world’s then-largest exchange, has left creditors waiting over a decade for compensation.

While some feared that repayments could unleash fresh supply, blockchain data shows these movements were administrative, not market sales. Still, perception alone was enough to unsettle sentiment, sparking liquidations and feeding the broader risk-off tone. Analysts now estimate over 230,000 trading accounts were liquidated within 24 hours, totalling more than $1 billion in forced sell orders.

Why this matters

Sentiment has swung hard into fear. CoinDesk flagged “extreme fear” conditions into the weekend and early week, aligning with widely followed gauges that punish downside volatility and negative breadth. In past cycles, similar extremes have marked acceleration phases within larger drawdowns or short-lived exhaustion points.

The macro overlay is not helping. Traders are parsing shifting expectations for U.S. rate cuts and inflation risks tied to policy developments, a mix that reduces risk appetite and tightens crypto liquidity. Reuters’ read-across captures the mood: a near 30 percent retreat from the October peak and growing caution among institutions.

Impact on markets and participants

Price leadership rotated back to bitcoin as traders sold altcoins to manage risk, a pattern visible when social attention and volumes consolidate in the benchmark asset during stress. Ether and other large caps have tracked lower alongside, while crypto-linked equities have generally underperformed on drawdown days, transmitting crypto volatility into listed proxies.

For allocators, ETF prints serve as the cleanest real-time barometer of spot demand. Multi-day flat or negative flows often coincide with fragility in order books and heavier slippage, which is why desks are laser-focused on whether the next sequence turns positive again. If it doesn’t, the unfilled liquidity pocket toward 86,000–88,000 dollars cited by traders continues to be a live risk.

Expert outlook

CoinDesk’s market desk notes that fear spikes of this magnitude have sometimes preceded relief rallies, particularly when realised-loss pressure begins to stabilise and ETF outflows slow. That requires confirmation: a swift reclaim of broken support and evidence of renewed net inflows. Until then, technicals and positioning argue for elevated two-way volatility.

Long-horizon investors continue to point at structural adoption and institutional participation as reasons to stay constructive on multi-year horizons. Dan Tapiero, whose 50T platform backs later-stage crypto companies, frames short-term turbulence as noise against a secular build-out, a view he has reiterated while forecasting a much larger digital-asset economy over the next decade.

Bitcoin price technical insight

Bitcoin (BTC/USD) continues its downward trajectory after forming a death cross, with the 50-day moving average (MA) crossing below the 200-day MA - a classic bearish signal suggesting extended downside pressure. The price is currently hovering near $91,000, after repeatedly failing to hold above key resistance levels at $106,685, $114,000, and $124,650, where prior rallies saw heavy profit-taking and FOMO-driven buying.

The Relative Strength Index (RSI) has dipped into oversold territory, indicating that selling momentum may be overextended and a short-term technical rebound could occur. However, as long as BTC remains below the 50-day MA, the broader trend remains bearish, with traders likely to view any bounce as a chance to sell into strength.

Key takeaway

Bitcoin’s slide below $90,000 reflects a convergence of technical breakdown, hesitant ETF demand, and a risk-off macro tone. The resulting fear spike is typical of late-stage selloffs, but it needs flow confirmation before calling a durable low. Watch for a quick reclaim of the $ 90,000 - $93,000 zone and a run of positive ETF prints to validate any rebound attempt. Until then, expect elevated volatility and tighter liquidity conditions.

抱歉,無法找到符合 的結果。

搜尋提示:

- 檢查拚寫並重試

- 嘗試其他關鍵字