검색 결과

위험지대에 머물고 있는 USD/JPY: 일본은 160선 상승을 멈출 수 있을까요?

USD/JPY는 현재 트레이더들이 “위험 지대”라고 부르는 지역, 즉 이전에 일본의 압박을 받을 수 밖에 없었던 155~160 박스권을 맴돌고 있습니다.

USD/JPY는 현재 트레이더들이 “위험 지대”라고 부르는 지역, 즉 이전에 일본의 압박을 받을 수 밖에 없었던 155~160 박스권을 맴돌고 있습니다.애널리스트들에 따르면, USD/USD는 이 레벨을 돌파할 경우 도쿄가 엔화 방어를 위해 다시 개입할 수 있는 수준을 시험하고 있다고 합니다.시장의 경우 이는 단순한 심리적 임계값이 아니라 역사가 그린 선입니다.160에 가까워질 때마다 과거 개입에 대한 기억과 함께 일본이 개입하기 전에 얼마나 약세를 보일 것인지에 대한 추측이 되살아납니다.

보고서에 따르면 긴장의 중심에는 일본의 재정 확장과 신중한 통화 기조 간의 격차가 커지고 있습니다.미국이 고금리를 유지하고 있는 것처럼 사나에 다카이치 총리의 21.3조 엔 (1,120억 파운드) 규모의 경기부양책으로 인해 수익률이 상승하고 엔화는 더욱 약세를 보이고 있습니다.

이제 문제는 일본이 USD/JPY가 160을 돌파하고 세계 무대에서 도쿄의 결의를 시험하기 전에 USD/JPY의 상승을 멈출 수 있는지, 아니면 제때 조치를 취할 것인지 여부입니다.

USD/JPY를 이끄는 요인은 무엇일까요?

최근 엔화 하락은 일본과 미국의 정책 격차 확대에 뿌리를 두고 있습니다.팬데믹 이후 최대 규모를 기록한 다카이치 총재의 경기부양책에는 에너지 구제, 세금 감면, 현금 지급 등에 대한 지출이 포함됩니다.이는 생활비 압박을 완화하는 것을 목표로 하고 있지만 투자자들은 이를 인플레이션이고 재정적으로 무모하다고 보고 있습니다.블룸버그는 부채 우려가 심화되고 장기 재정 규율에 대한 신뢰가 약해지면서 일본 국채 (JGB) 수익률이 2008년 이후 최고치를 기록했다고 보도했습니다.

일본은행 (BoJ) 의 신중한 입장은 압력을 증폭시켰을 뿐입니다.우에다 카즈오 총재는 인플레이션이 목표 2% 를 상회하고 있음에도 불구하고 주요 정책 변화 이전에 임금 상승률이 안정화되어야 한다고 계속 주장하고 있습니다.

이와는 대조적으로, 연방준비은행은 미국 금리를 인상했으며 빠른 금리인하를 꺼려하고 있습니다.이러한 수익률 차이로 인해 달러 보유에 대한 보상이 높아져 자본이 엔화 밖으로 유출되고 USD/JPY는 수년 만에 최고치 근방에 머물게 됩니다.

중요한 이유

시장 관측자들은 엔화 약세가 양방향으로 하락한다고 말합니다.통화 약세는 해외 수입이 수익 증가로 이어지는 Toyota 및 Sony와 같은 수출업체에게 이익이 됩니다.그러나 수입업자와 가정에서는 고통이 즉각적입니다.일본은 수입 연료와 식품에 크게 의존하고 있습니다. 즉, USD/JPY가 1초간 상승할 때마다 일상 생활비가 더 비쌉니다.브루킹스 연구소의 로빈 브룩스 (Robin Brooks) 는 정부의 재정 기조를 “부채 거부”라고 설명하면서 “실질 실질 기준으로 볼 때 일본 엔화는 터키 리라와 거의 비슷하다”고 경고했다.

일본 국경을 넘어 엔화는 위험 심리의 글로벌 지표 역할을 합니다.환율이 급락하면 달러에 대한 신뢰가 높아지고 엔화로 자금을 조달하는 캐리트레이드 전략이 강화됩니다.하지만 도쿄가 개입할 경우 급격한 반전 위험이 커질 수도 있습니다.시장은 여전히 연중기를 떠올립니다. 당시 일본은 USD/JPY가 160달러를 잠깐 돌파한 후 자국 통화를 방어하기 위해 600억 달러 이상을 썼다고 합니다.이러한 유산을 바탕으로 밴드 내 모든 움직임은 카운트다운처럼 느껴집니다.

시장 및 전략에 미치는 영향

채권 시장에서 투자자들은 재정 위험을 상쇄하기 위해 더 높은 수익률을 요구하고 있으며, 이로 인해 10년물 JGB 금리는 1% 이상으로, 40년물 수익률은 3.6% 이상으로 상승하고 있습니다.이러한 상승은 이미 일본 경제 규모의 두 배가 넘는 일본 부채가 다카이치의 성장 촉진 어젠다에 따라 더 늘어날 것이라는 우려를 반영합니다.

카타야마 사츠키 재무장관은 이미 정부가 “무질서한 움직임에 대해 조치를 취할 것”이라고 경고했는데, 이는 현재 트레이더들이 은폐된 개입의 위협으로 해석하고 있습니다.

주식 투자자의 경우 엔화 약세가 단기적으로 상승했습니다.Nikkei 225는 수출이 많은 주식과 해외 실적 폭락에 힘입어 수십 년 만에 최고 수준까지 상승했습니다.

하지만 여기에는 대가가 따릅니다. 소비자 신뢰지수가 하락했고 기대 인플레이션이 상승하고 있습니다.전 세계적으로 엔화 약세는 주식, 심지어 암호화폐에 대한 원동력인 위험 선호도를 높여주고 있지만, 도쿄 또는 BoJ가 갑자기 입장을 바꾼다면 시장이 급격한 조정에 취약해질 수 있습니다.

소매 트레이더에게 이러한 변동성은 기회와 위험을 동등하게 제공합니다.주요 레벨 주변에서는 변동성이 크기 때문에 체계적인 포지션 규모 조정 및 마진 추적이 필수적입니다. 이러한 도구는 다음과 같습니다. 파생 계산기 트레이더가 시장에 진입하기 전에 핍 가치, 계약 규모 및 잠재적 손익을 추정하는 데 도움이 될 수 있습니다.

전문가 전망

USD/JPY 전망치는 타이밍에 따라 달라집니다.대다수의 경제학자들이 예상하는 것처럼 BoJ가 12월에 금리를 0.75% 까지 인상한다면 엔화는 150까지 다시 안도 랠리를 펼칠 수 있습니다.

그러나 중앙은행 (ECB) 이 지연되고 미국 경제지표가 견고하게 유지된다면 트레이더는 박스권 상한선을 계속 테스트할 수 있습니다.웰링턴 앨터스의 제임스 쏜 (James Thorne) 은 “사나에 다카이치 (Sanae Takaichi) 의 아베노믹스 스타일 경기 부양책은 글로벌 유동성을 확대하고 달러 강세를 보일 것입니다. 킹 달러는 건재합니다”라고 말했습니다.

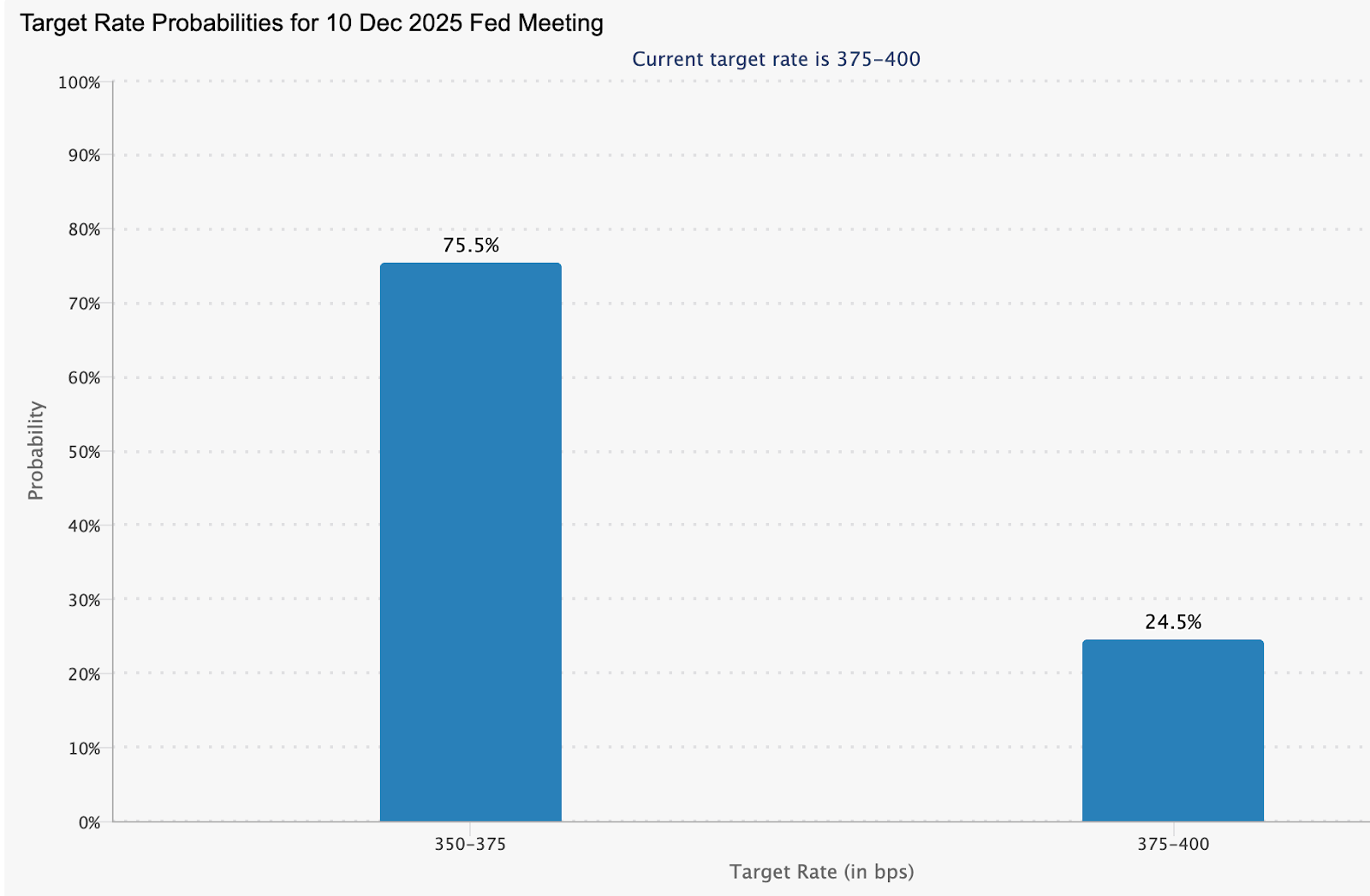

많은 것은 연준이 BoJ보다 먼저 움직일지 여부에 달려 있습니다.선물 시장은 현재 12월 미국 금리인하 가능성을 75.5% 로 보고 있습니다.

분석가들은 또한 비둘기증이라고 덧붙였습니다. 연준 수익률 격차를 좁히고 엔화 매수를 촉발할 수 있습니다.하지만 그렇지 않으면 일본 통화는 여전히 정책 관성과 글로벌 심리에 영향을 줄 수 있습니다.USD/JPY가 160 근방에 머무는 기간이 길어질수록 도쿄가 여전히 시장의 존경을 받고 있다는 것을 증명해야 한다는 압력이 커집니다.

USD/JPY 기술 인사이트

이 글을 쓰는 시점에서 USD/JPY는 156.66 근방에서 거래되고 있으며, 연장 후 가격 발견 영역 내에서 통합되고 있습니다. 낙관적 를 실행합니다.볼린저 밴드 (10, 종가) 가 확대되고 있는데, 가격 움직임이 상단 밴드 근방에 머물면서 변동성이 확대되고 지속 편향을 보이고 있습니다. 이는 강력한 강세 모멘텀의 신호이지만 단기 소진 위험도 증가합니다.

주요 지지대는 154.00, 150.00, 146.60이며, 이 지지선을 하향 이탈한다면 매도 청산 및 심층 조정이 시작될 수 있습니다.반면, 156.00 위에서 가격이 발견되면 저항선이 제한될 수 있습니다. 즉, 변동성이 급증하지 않는 한 다음 하락에는 하락 매수자가 몰릴 수 있습니다.

더 RSI (14) 은 과매수 영역에 진입하고 있는데, 이는 강세 강세가 정점에 가까워지고 있음을 시사합니다.RSI가 70 이상으로 유지된다면 모멘텀이 더 높아질 수 있지만, 이 레벨 아래로 반전된다면 차익실현 또는 조기 매도 압력이 이어질 수 있습니다.

주요 테이크 아웃

애널리스트들에 따르면, USD/JPY가 155~160선을 향해 돌아선 것은 단순한 차트 패턴을 넘어 일본 정책 믹스에 대한 국민투표라고 합니다.이에 상응하는 통화 조정이 없는 재정 확장으로 엔화는 취약해지고 투자자들은 회의적인 반응을 보이고 있습니다.개입으로 시장이 잠깐 안정될 수 있지만, 단호한 긴축 또는 재정 억제만이 신뢰를 회복할 수 있습니다.그때까지는 USD/USD가 위험 지대에 완전히 놓여 있습니다. 이러한 움직임이 오를 때마다 도쿄의 관용력뿐 아니라 자국 통화를 통제할 수 있는 일본의 능력에 대한 전 세계의 믿음이 시험대에 오르게 됩니다.

Nvidia의 깜짝 실적, 시장의 냉담한 반응

Nvidia의 급등과 다음 분기 약 650억 달러로 상향된 가이던스에도 불구하고, 시장의 반응은 이상하리만치 조용했습니다.

Nvidia Corporation이 3분기 매출 570억 달러(전년 대비 62% 증가)를 발표했을 때, AI 하드웨어 경쟁에서 또 한 번의 완벽한 승리처럼 보였습니다. 그러나 급등과 다음 분기 약 650억 달러로 상향된 가이던스에도 불구하고, 시장의 반응은 이상하리만치 냉담했습니다.

유출된 전체 직원 회의에서 CEO 젠슨 황은 “시장이 이를 높이 평가하지 않았다”고 인정했습니다. 실행과 기대감 사이의 이 괴리는 얼마나 높은 기대치와 AI 열풍이 최고의 실적을 내는 기업에게도 기준을 얼마나 높여놓았는지를 보여줍니다.

Nvidia의 깜짝 실적을 이끈 요인

Nvidia 실적의 핵심은 여전히 데이터 센터 수요, 즉 AI 인프라의 중추입니다. 이 부문만으로 약 510억 달러의 매출을 기록했으며, 이는 전년 대비 66%, 전 분기 대비 25% 증가한 수치입니다.

Blackwell 플랫폼과 같은 주력 제품이 여전히 기업 주문을 주도하고 있으며, 가이던스는 또 한 번의 기록적인 분기(매출 650억 달러, 전년 대비 65% 성장)를 예고합니다. Nvidia는 단순히 성장하는 것이 아니라, 업계 전체의 자본 지출 사이클의 템포를 정의하고 있습니다.

지정학적·구조적 요인도 이러한 성장을 가속화합니다. 클라우드, 로보틱스, 자율 시스템이 전 세계적으로 확장됨에 따라, Nvidia의 하드웨어는 혁신의 중심이자 공급의 병목에 위치합니다. 그러나 성공에는 취약성도 따릅니다. 완벽함이 기대치가 되면, 작은 흔들림도 큰 충격처럼 느껴집니다. 한 애널리스트는 “시장이 완벽을 기대하도록 학습시켰을 때, 훌륭함조차도 충분하지 않다”고 말했습니다.

왜 중요한가

Nvidia는 현재 S&P 500 전체 비중의 약 7.31%를 차지하며, AI 심리의 가장 영향력 있는 바로미터가 되었습니다. 이렇게 거대한 종목이 기록적인 분기 후에도 횡보한다는 것은 투자자들이 데이터가 아니라, 내러티브에 의문을 제기하고 있음을 시사합니다.

FinancialContent는 이를 “AI와 전체 시장에 있어 중대한 시험대”라고 표현했습니다. Nvidia의 탁월함이 더 이상 흥분을 불러일으키지 못한다면, 나머지 기술주들도 냉기를 느낄 것입니다.

황 CEO는 이를 명확히 밝혔습니다. “실적이 나쁘면 거품을 터뜨렸다는 비난을 받고, 실적이 좋아도 거품을 키웠다는 비난을 받는다.” 이러한 인식의 함정은 AI 트레이드의 새로운 국면, 즉 시장을 움직이려면 결과가 예외적이어야 하는 시대를 보여줍니다. 이는 또한 미묘한 변화를 반영합니다. 과장과 약속에서 규율과 실적으로의 전환입니다.

기술 및 AI 생태계에 미치는 영향

Nvidia의 실적 발표는 처음에는 AMD, Broadcom, 메모리 공급업체 등 전반적인 기술주를 끌어올렸습니다. 그러나 시간이 지날수록 그 상승분은 사라졌고, 이는 투자 심리가 얼마나 취약해졌는지를 보여줍니다.

애널리스트들에 따르면, 이처럼 엄청난 실적에도 랠리가 이어지지 않는다면, AI 인프라 성장의 상당 부분이 이미 주가에 반영되었음을 의미합니다. 이제 투자자들은 단순한 확장보다는 운영 효율성에 보상을 줄 수 있습니다. 이는 자연스러운 진화입니다. 성장의 성숙기에는 밸류에이션에 대한 규율이 우선시됩니다.

하드웨어 구매자와 기업 사용자에게 이 변화는 공급 여건이 다소 완화되지만 가격은 더 타이트해질 수 있음을 의미합니다. Nvidia의 과제는 생산량을 늘리면서도 마진을 유지하는 것, 즉 비전 중심의 성장에서 산업적 정밀성으로의 전환입니다.

전문가 전망

시장 전문가들은 두 가지 길이 있다고 말합니다. Nvidia가 계속해서 실행력을 보여주고, 신제품 라인을 확장하며, 제조 역량을 넓히고, 수출 리스크를 잘 관리한다면, 리더십을 유지하고 성장세를 이어갈 수 있습니다. 이 회사는 여전히 소수만이 넘볼 수 있는 기술적 해자를 보유하고 있습니다.

다른 시나리오는 밸류에이션 조정입니다. 투자자들이 하드웨어 성장이 비용 인상과 경쟁을 무기한 앞지를 수 있을지 의문을 갖기 시작한다면, Nvidia는 정체 국면에 직면할 수 있습니다. Bernstein의 한 애널리스트는 “적어도 실적만 놓고 보면, 더 이상 뭘 바랄 수 있을지 모르겠다”고 말했습니다.

트레이더들에게는 가이던스 추이, 백로그(특히 중국 내) 업데이트, Rubin 및 Blackwell 칩의 출시 속도가 주요 모니터링 신호입니다. 수 주 만에 5천억 달러에 달하는 시가총액 변동은 투자 심리가 얼마나 민감해졌는지를 보여줍니다.

Nvidia 기술적 인사이트

작성 시점에서 Nvidia(NVDA)는 $194.50 부근에서 거래되고 있으며, $179.70 지지선을 테스트한 후 하단 Bollinger Band에서 반등하고 있습니다. Bollinger Bands(10, 종가 기준)는 점진적으로 확장되고 있는데, 이는 변동성 증가의 신호이며, 가격 움직임이 중간선 쪽으로 수렴하고 있음을 보여줍니다. 이는 단기적으로 상단 밴드까지의 추가 상승 가능성을 시사합니다.

$173.20 수준은 다음 주요 지지선으로 부각되며, 이 아래로 하락할 경우 매도 청산이 촉발되어 하락 모멘텀이 강화될 수 있습니다. 반대로, $208.00은 강한 저항 구간을 형성하며, 랠리가 이어질 경우 이익 실현과 막차 FOMO 매수가 동시에 나타날 수 있습니다.

모멘텀 지표도 강세 시나리오에 힘을 실어줍니다. RSI(14)는 급격히 상승해 50선 부근의 중간선을 상향 돌파했으며, 이는 매수세 재개를 알리는 기술적 신호입니다. 이 수준을 지속적으로 상회하고, $179.70 이상에서 안정성을 유지한다면 단기 상승 추세가 강화되어 모멘텀 트레이더들의 관심을 다시 끌 수 있습니다.

시나리오를 그리는 이들에게는 Deriv calculator를 활용해 다양한 변동성 환경에서 손익을 시뮬레이션할 수 있습니다. 이는 Deriv MT5에서 NVDA 트레이딩을 계획할 때 차트 분석을 보완하는 필수 도구입니다.

핵심 요약

투자자들은 Nvidia가 AI 인프라 붐의 중심에 남아 있을 것으로 보고 있으며, 재무적으로나 기술적으로나 독보적이라고 평가합니다. 그러나 시장의 미지근한 반응은 전환점을 의미합니다. 이제 투자자들은 약속이 아니라 증거에만 보상합니다. AI 트레이드의 이 새로운 국면에서는 실행력, 마진 회복력, 혁신 속도가 리더십을 결정할 것입니다. 트레이더들에게 Nvidia의 차트는 단기 상승 여력을 시사할 수 있지만, 더 큰 이야기는 기대치의 변화, 즉 완벽함이 이제는 놀라움이 아니라 기본값이 된 시대라는 점입니다.

금 가격 전망: 중앙은행이 하한선을 제공하고 있습니다

금리 인하 베팅과 달러 강세의 저변에는 더 깊은 구조적 힘이 있습니다. 바로 세계 중앙은행의 끊임없는 금 매수입니다.

보고서에 따르면 금이 온스당 $4,050 근방에서 놀라운 안정세를 보인 것은 우연이 아닙니다.금리 인하 베팅과 달러 강세가 약화되고 있다는 잡음 이면에는 더 깊은 구조적 힘이 있습니다. 바로 세계 중앙은행의 끊임없는 매수세입니다.베이징에서 앙카라에 이르기까지 정책 입안자들은 정치적 위험, 통화 불안정, 미국 금융 질서에 대한 신뢰 약화에 대한 헤지 수단으로 금을 사용하여 통화 안전 규칙을 조용히 재편하고 있습니다.

애널리스트들에 따르면 이러한 수요는 금괴를 지탱하는 보이지 않는 손이 되었습니다.투기적 투자자들이 철수하고 ETF 유동성이 줄어드는 와중에도 주권 매수자들은 시장을 안정시키는 데 도움을 주고 있습니다.

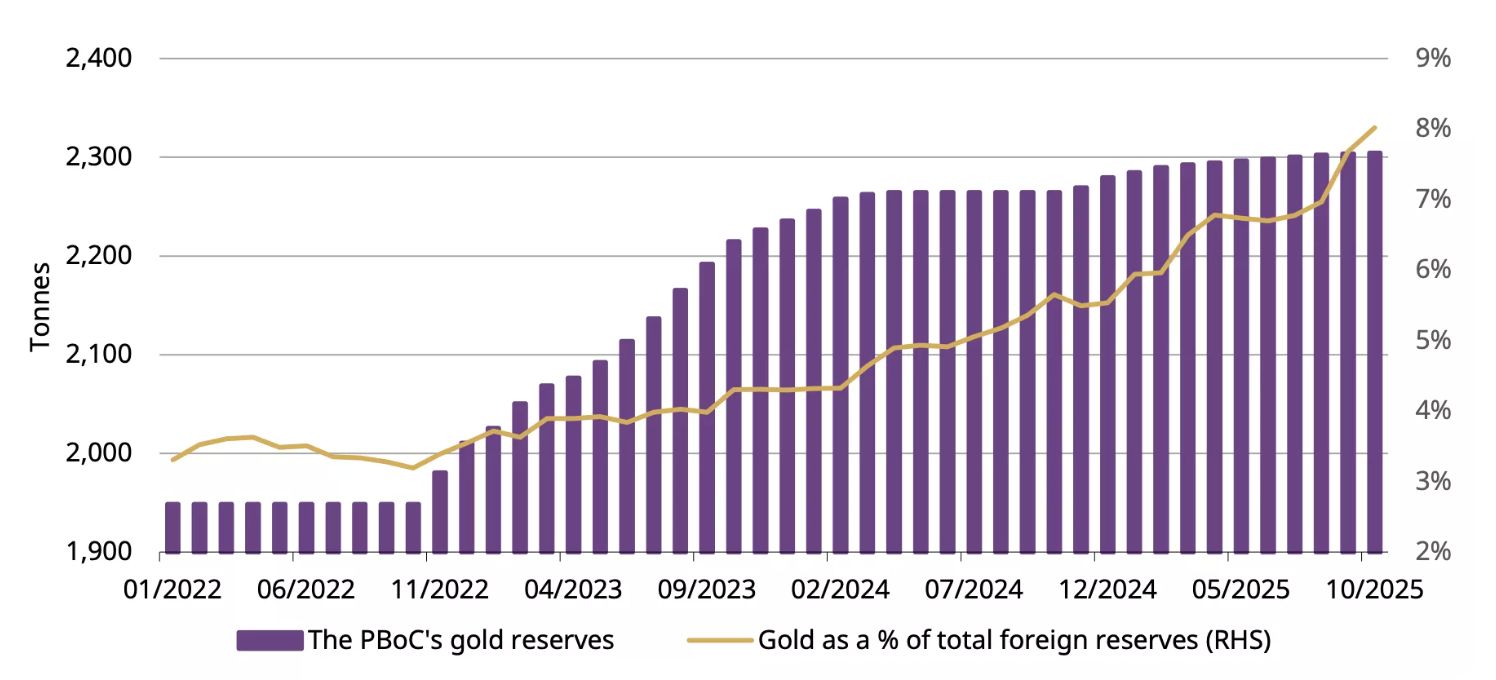

중국 인민은행 (PINE Bank of China) 이 12개월 연속 금 매수 행진을 이어가고 있고, 다른 중앙은행들도 이에 뒤따랐기 때문에, 금의 하락 리스크는 이제 폭락이라기보다는 일시정지에 가까운 것으로 보입니다. 즉, 하한선은 자금이 아니라 국가에 의해 강화된 상태입니다.

현재 금의 원동력은 무엇일까요?

최신 미국 고용 데이터는 글로벌 시장 전반의 기대치를 재조정했습니다.9월 비농업 고용 보고서에 따르면 119,000개의 일자리가 증가하여 경제학자들이 예상했던 것보다 두 배 이상 증가했으며 실업률은 4.4% 까지 증가했습니다.

표면적으로는 고용은 강했지만 모멘텀은 완화되는 등 혼조세를 보이고 있지만, 이는 투자자들이 연방준비은행의 12월 금리 인하 요구를 철회하기에 충분했습니다.

이러한 재조정으로 달러와 미국 수익률이 상승했는데, 이는 일반적으로 금에 독이 되는 조합이었습니다.하지만 금값은 거의 꿈쩍하지 않았습니다.그 이유는 중앙은행 수요로 인해 정책 사이클에 대한 금의 민감도가 달라졌기 때문입니다.

세계 금위원회 (World Gold Council) 의 자료에 따르면, 공식 부문 구매는 현재 연간 수요의 거의 4분의 1을 차지합니다. 이는 10년 전과 비교했을 때 구조적 변화입니다.연준이 망설여도 중앙은행은 망설이지 않습니다.

중국 인민은행 (PBoC) 이 12개월 연속 금 매수를 발표했는데, 10월에는 0.9톤이 추가되어 총 금값이 2,304톤으로 상승하여 중국 외환보유고의 8% 를 차지하며 1년 연속 매수세가 이어졌습니다.터키, 폴란드, 인도 모두 축적 추세에 동참했습니다.

중요한 이유

시장 관측자들은 이러한 조용한 국가 축적이 글로벌 금융 시스템에서 금의 역할을 재편하고 있다고 말합니다.예전에는 “위험 회피” 거래였던 것이 이제는 국가준비금 전략의 일부가 되었습니다.2022년 러시아 해외 자산이 동결되면서 각국 정부는 달러 위주 체제에 대한 노출을 재평가하게 되었고, 금은 중립적 대안으로 떠올랐습니다.

Zaner Metals 전략가 피터 그랜트 (Peter Grant) 가 말했듯이, 미국의 최신 고용 데이터는 “시장이 둔화되고 있지만, 그렇다고 해서 안전에 대한 욕구가 줄어들지는 않습니다.”

신흥 시장의 정책 입안자들에게 금은 종이 자산이 제공할 수 없는 무언가를 제공합니다. 바로 제재, 인플레이션, 통화의 정치 등입니다.투자자들에게 이는 금 가격이 더 이상 금리나 위험 성향에만 좌우되지 않는다는 것을 의미합니다.이는 지정학적 지표로서 현재 통화질서에 대한 신뢰가 얼마나 유지되고 있는지를 보여주는 지표입니다.

시장 및 투자자에게 미치는 영향

이번 사이클에서 가장 눈에 띄는 변화는 미국 달러 지수 (DXY) 가 몇 개월 만에 가장 강력한 수준에서 거래되고 있음에도 금이 사상 최고치 근방을 유지하고 있다는 것입니다.전통적인 역관계는 약세를 보이고 있습니다.애널리스트들에 따르면 두 자산 모두 안전이라는 동일한 이유로 매입되고 있습니다.이러한 추세는 금리가 하락할 때만 금이 랠리를 펼친다는 생각에 도전장을 던집니다.

트레이더에게는 단기 포지셔닝이 복잡해집니다.금이 10월 최고치인 4,380달러를 7% 가량 하회하는 등 모멘텀은 식었지만 구조적 수요는 그대로입니다.ETF 흐름은 최근 몇 주 동안 소폭 하락했지만 패닉의 조짐은 보이지 않습니다.

개인 투자자들은 투자 익스포저를 줄였지만 공식 부문이 이를 대체하여 한계 매수자로 떠올랐습니다.장기 투자자의 경우 이러한 변화는 특히 2026년까지 거시경제 불확실성이 심화될 경우, 하락폭이 경고보다는 기회를 제공할 수 있음을 시사합니다.

전문가 전망

중앙은행 (ECB) 의 이번 매수세가 어디까지 이어질 수 있을지에 대해서는 애널리스트들의 의견이 분분합니다.골드만삭스 (Goldman Sachs) 는 2026년까지 국채 및 민간 투자 수요 모두가 물가를 뒷받침할 것이라고 주장하면서 최근의 약세를 여전히 “반전이 아닌 일시적 현상”으로 보고 있습니다.UBS는 달러 준비금에서 벗어난 다각화가 지속된다면 향후 2년 내에 온스당 4,900달러까지 상승할 것으로 예상하고 있습니다.

이러한 전망의 주요 위험은 금전적 안일함에 있습니다.미국 경제지표가 견고하게 유지되고 연준이 “장기 상승” 기조를 재확인한다면 투기적 관심은 더 줄어들 수 있습니다.하지만 현재로서는 금의 탄력성이 그 자체로 잘 드러납니다.시장은 트레이더가 아닌 중앙은행이 주도하는 새로운 현실에 적응하고 있습니다.

골드 기술 인사이트

이 글을 쓰는 시점에서 금 (XAU/USD) 은 $4,030 주변에서 거래되고 있으며 $4,020 지지선 근처를 맴돌고 있습니다. RSI 평평하고 미드라인에 가까워 어느 방향으로든 강력한 모멘텀이 부족함을 나타내며 이는 시장이 우유부단하다는 신호입니다.

한편, 볼린저 밴드 최근 변동 이후 변동성이 낮아진 것을 반영하여 좁혀지기 시작했습니다.가격이 미드밴드 근방에서 요동치고 있어 다음 돌파 이전에 횡보 국면이 나타날 가능성이 높습니다.

반면에 $4,200 및 $4,365는 여전히 주요 저항선으로 남아 있으며, 강세 심리가 회복되면 트레이더는 차익 실현 또는 새로운 매수 관심을 기대할 수 있습니다.반대로 4,020달러를 하향 이탈한다면 3,940달러 지지선까지 오를 수 있으며, 이 지지선에서는 매도 압력이 증가하거나 청산 움직임이 나타날 수 있습니다.

주요 시사점

2025년 말 금의 회복세는 미스터리가 아닙니다. 애널리스트들이 전한 메시지입니다.한때 미국 국채를 신뢰했던 기관들이 이제는 정책, 정치, 불확실성에 대비하기 위해 금괴를 사들이고 있습니다.트레이더들은 랠리를 늦출 수 있지만 중앙은행은 꿈쩍도 하지 않고 있습니다.마찬가지로 연준 양분된 정책 전망을 헤쳐나가고 글로벌 준비금은 계속해서 동쪽으로 이동하고 있습니다. 금 밑의 바닥은 이를 잡고 있는 손처럼 견고해 보입니다.

.png)

Bitcoin’s harsh reset: Flows, fear and two lines that matter

The world’s largest cryptocurrency has shed nearly a third of its value since its October peak, slipping toward critical technical levels as headwinds take effect.

Bitcoin’s harsh reset has arrived. The world’s largest cryptocurrency has shed nearly a third of its value since its October peak, slipping toward critical technical levels as exchange-traded fund outflows and macroeconomic headwinds take effect.

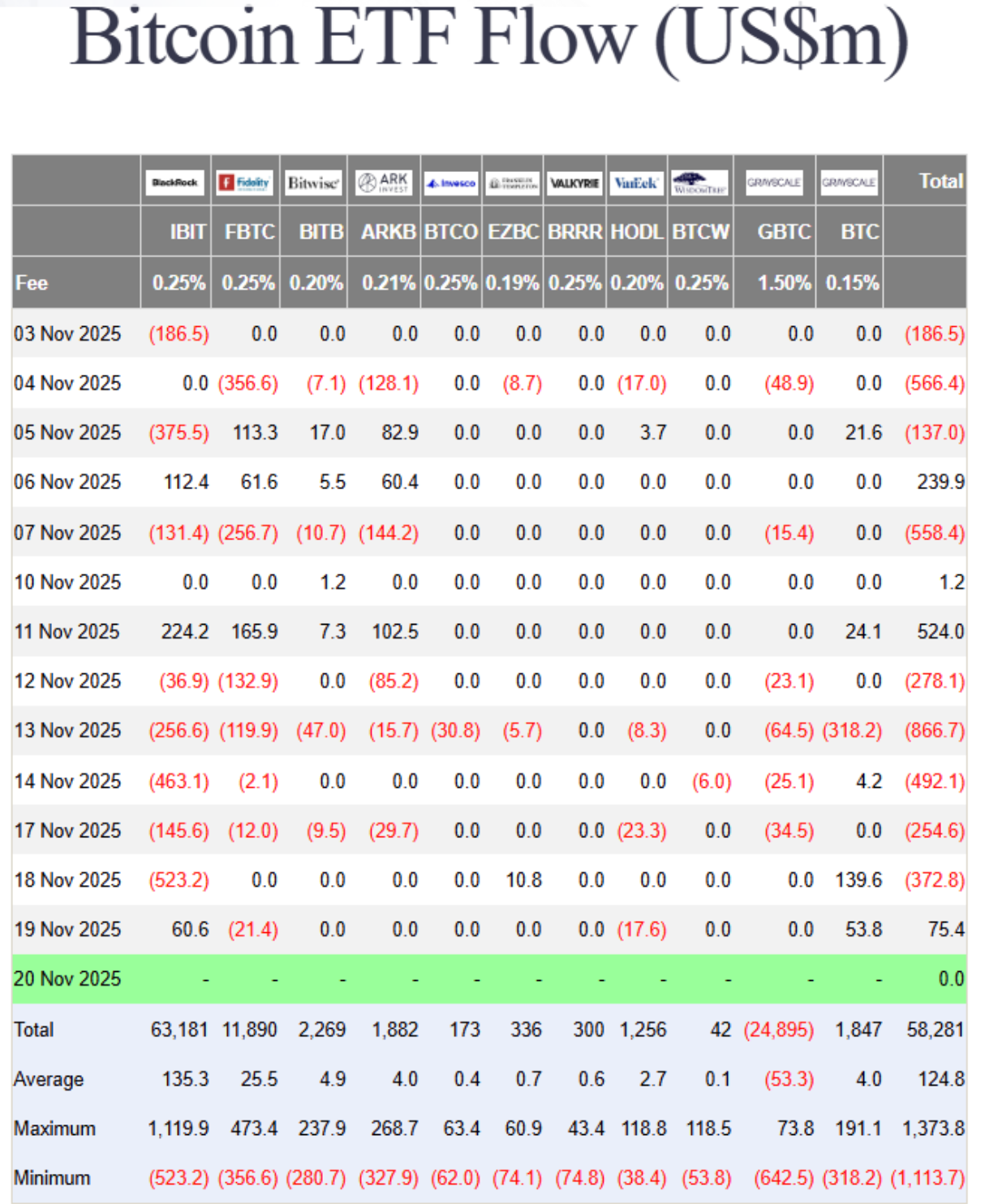

Recent data showed nearly $3 billion has exited Bitcoin ETFs this month alone, turning the same institutional flows that once fuelled the rally into a feedback loop of redemptions and retreat.

Behind the selloff lies a mix of fading Fed-rate-cut hopes, tightening liquidity, and a market paralysed by “extreme fear”. With prices hovering near $85,600 and the one-year low at $74,000 looming, the question is simple but urgent: is this correction a passing flush - or the start of a deeper shift in Bitcoin’s new ETF era?

What’s driving Bitcoin’s correction

Bitcoin’s 30% slide isn’t being driven by scandal or shock - it’s the result of structural forces finally reversing, according to analysts. After two years of relentless inflows, spot Bitcoin ETFs are now experiencing capital outflows. Institutional investors, once hailed as crypto’s stabilisers, are showing how quickly sentiment turns when markets wobble.

According to Farside data, ETF redemptions have occurred on all but four days this month, stripping nearly $3 billion in net outflows.

Part of that retreat stems from shifting macro conditions. The Federal Reserve’s reluctance to confirm rate cuts has strengthened the US dollar, drawing liquidity away from speculative assets.

Past movements have shown that a stronger dollar typically weighs on Bitcoin, and with inflation readings still sticky, traders are reassessing the narrative of “easy money” returning in December. The result is a market where rallies are met with selling rather than enthusiasm - a sharp turn from the euphoria that drove Bitcoin to $126,000 just weeks ago.

Why it matters

Bitcoin’s selloff is revealing just how tightly traditional and digital markets are now intertwined. ETFs opened the floodgates for institutional exposure, but they also linked Bitcoin to broader risk trends. When investors pull money from ETF products, the effect ricochets through liquidity pools and sentiment alike.

As Matt Williams of Luxor explained, “The drop to $86,000 is largely driven by macro forces - rate expectations, inflation - and by large holders cutting exposure after breaking key technical supports.”

For traders, this is a psychological turning point. The same retail crowd that once flooded exchanges during Thanksgiving 2017 - when Bitcoin first crossed $10,000 - is largely silent now.

Social data from Santiment shows sentiment evenly split between predictions of a plunge below $70,000 and wild optimism for a rally to $130,000. The divide signals indecision, not conviction. In this phase, fear - not fundamentals - is setting the tone.

Impact on markets and investors

The selloff has spilled beyond the crypto space. Bitcoin’s correlation with equity indices, such as the Nasdaq 100, has climbed above 0.8 at times, meaning that moves in tech stocks and digital assets now feed off the same macro triggers. When rate optimism fades, both markets suffer. That link cuts against Bitcoin’s long-standing claim as a hedge against monetary risk.

ETF outflows are another pressure point. As funds are redeemed, liquidity providers are compelled to unwind their positions in futures and spot markets, thereby deepening volatility.

The Crypto Fear & Greed Index, which plunged to 14 this week - its lowest since February - underscores how rapidly sentiment has deteriorated. Analysts like Rachael Lucas of BTC Markets warn that momentum, money flow, and volume trends “all reflect a sharp deterioration in sentiment,” driven by macro tightening and risk-off positioning.

In the background, liquidity providers are struggling. Tom Lee of Fundstrat compared crypto market makers to “central banks” of digital liquidity - and right now, those banks are running dry.

Following October’s $20 billion liquidation wave, market makers are operating with smaller balance sheets, which limits their ability to absorb order flow. It’s a reminder that crypto’s plumbing, though more sophisticated, is still fragile.

Expert outlook

Analysts are torn between caution and curiosity. Nic Puckrin of Coin Bureau describes the current landscape as a “bull-bear tug of war,” with macroeconomic pessimism offset by resilience in the tech sector.

Nvidia’s earnings beat briefly lifted risk appetite, but Bitcoin failed to follow through, suggesting traders are still unwinding rather than reloading. Puckrin pegs the next resistance at $107,500, if a rebound can gain traction.

Andre Dragosch of Bitwise sees parallels to past mid-cycle corrections, noting that the depth and duration of this decline “remain consistent with interim pullbacks in previous bull markets.” His base case still anticipates the cycle extending into 2026, driven by gradual global monetary easing.

For now, though, short-term risk remains tilted lower, with $85,600 and $74,000 as the two critical levels to watch. Hold those, and Bitcoin could form a base; lose them, and the next flush could be swift.

The bigger picture: Could Bitcoin trigger a financial crisis?

Despite the panic, Bitcoin remains relatively small compared to the real financial system. The total crypto market stands around $3–4 trillion, with Bitcoin representing roughly half. In contrast, global financial assets exceed $400 trillion. Past collapses, such as FTX in 2022 and Terra in 2021, caused chaos within the crypto industry but barely rippled across global markets.

That said, every cycle pulls crypto closer to traditional finance. ETFs, corporate holdings, and stablecoins backed by US Treasuries have created real linkages. A severe Bitcoin crash could trigger ETF redemptions, hurt balance sheets at companies holding BTC, and pressure stablecoins to liquidate their Treasury assets. None of that would cause a 2008-style crisis today - but as the overlap grows, the line between “crypto crash” and “financial contagion” gets thinner.

Bitcoin technical insights

At the time of writing, Bitcoin (BTC/USD) is trading around the $84,200 mark after an extended downtrend. The RSI has plunged sharply into oversold territory, signalling intense bearish momentum and the potential for a short-term relief bounce if buyers step in.

A death cross - where the 50-day moving average has fallen below the 200-day moving average - reinforces the bearish bias, suggesting further downside pressure in the near term.

Key resistance levels sit at $106,260, $115,200, and $123,950, where traders may expect profit-taking or renewed buying interest if recovery attempts occur. Failure to reclaim these zones could see Bitcoin remain under pressure, with sentiment staying fragile amid persistent selling.

Key takeaways

Bitcoin’s decline isn’t an accident - it’s a stress test of its new reality. The ETF era has tied the cryptocurrency closer to the global financial system, for better and worse. Liquidity, once a tailwind, now cuts both ways. Fear dominates, but deep corrections are part of Bitcoin’s DNA.

If those two lines - $85,600 and $74,000 - hold firm, many say this reset may end up looking like just another cleansing phase before the next wave of institutional demand. Lose them, and Bitcoin’s harsh reset could turn into something much deeper.

Nvidia earnings reality check: Is the AI boom back on track?

Nvidia’s latest earnings didn’t inflate another round of hype; they restored confidence that artificial intelligence is entering its scale phase.

Yes - the AI boom is back on track, according to analysts, just in a different gear. Nvidia’s latest earnings didn’t inflate another round of hype; they restored confidence that artificial intelligence is entering its scale phase, not its speculative one.

Nvidia investors are bracing for a $300 billion surge in market value after the chipmaker reported its first sales acceleration in seven quarters, signalling that AI demand isn’t fading - it’s normalising into a sustainable growth cycle.

For months, markets were haunted by talk of “peak AI.” However, Nvidia’s results - record data centre revenue, renewed partnerships, and a 5% share spike in after-hours trading - show the story isn’t one of collapse, but calibration. This isn’t a bubble bursting; it’s the industry learning how to breathe again.

What’s driving Nvidia’s momentum

At the core of Nvidia’s dominance in artificial intelligence architecture is its data centre segment, which surpassed $50 billion this quarter, a milestone reached earlier than analysts expected.

This reflects an industrial-scale buildout, not a speculative frenzy. The surge in demand from AI workloads has transformed GPUs from niche products into the backbone of modern computing, powering everything from ChatGPT to enterprise cloud systems.

CEO Jensen Huang captured it best: “We’re in every cloud.” That ubiquity underpins Nvidia’s stability. Its chips are not optional - they’re essential infrastructure. With Blackwell GPUs offering up to 40 times faster inference speeds than the previous generation, the company isn’t chasing hype; it’s engineering the next leap in computational efficiency.

Why it matters

Nvidia’s report acts as a barometer for the AI economy. The stock’s post-earnings rally wasn’t just about profits; it was about validation. The market had priced in fear after days of tech sell-offs, but Nvidia’s blowout numbers reintroduced realism.

Analysts like Julian Emanuel of Evercore ISI summed up the pre-earnings tension: “The angst around ‘peak AI’ has been palpable.” Those fears evaporated when Nvidia showed that demand isn’t flattening - it’s broadening.

The company’s performance has become closely tied to the trajectory of U.S. equities. With AI now a structural growth driver, Nvidia’s consistency reassures investors that this is an economic revolution in progress, not a fleeting mania. Its $5 trillion valuation last month wasn’t an aberration; it was a preview of scale yet to come.

Impact on global markets

The aftershocks were immediate. Tech indices that had stumbled under the weight of “AI fatigue” rebounded as Nvidia reignited investor faith. Asian markets opened higher, and S&P futures turned positive, driven by renewed conviction that the AI trade still has legs. Even after a period of correction - Meta down 19%, Oracle off 20% - Nvidia’s performance reaffirmed that the long-term AI thesis remains intact.

Beyond markets, Nvidia’s results signal a new capital cycle. Its multibillion-dollar partnerships with Microsoft, OpenAI, and Anthropic aren’t one-off investments; they’re structural commitments to an AI-driven infrastructure era. Every dollar of GPU spending feeds into an ecosystem that’s building capacity for the next generation of models, data centres, and intelligent services.

Expert outlook

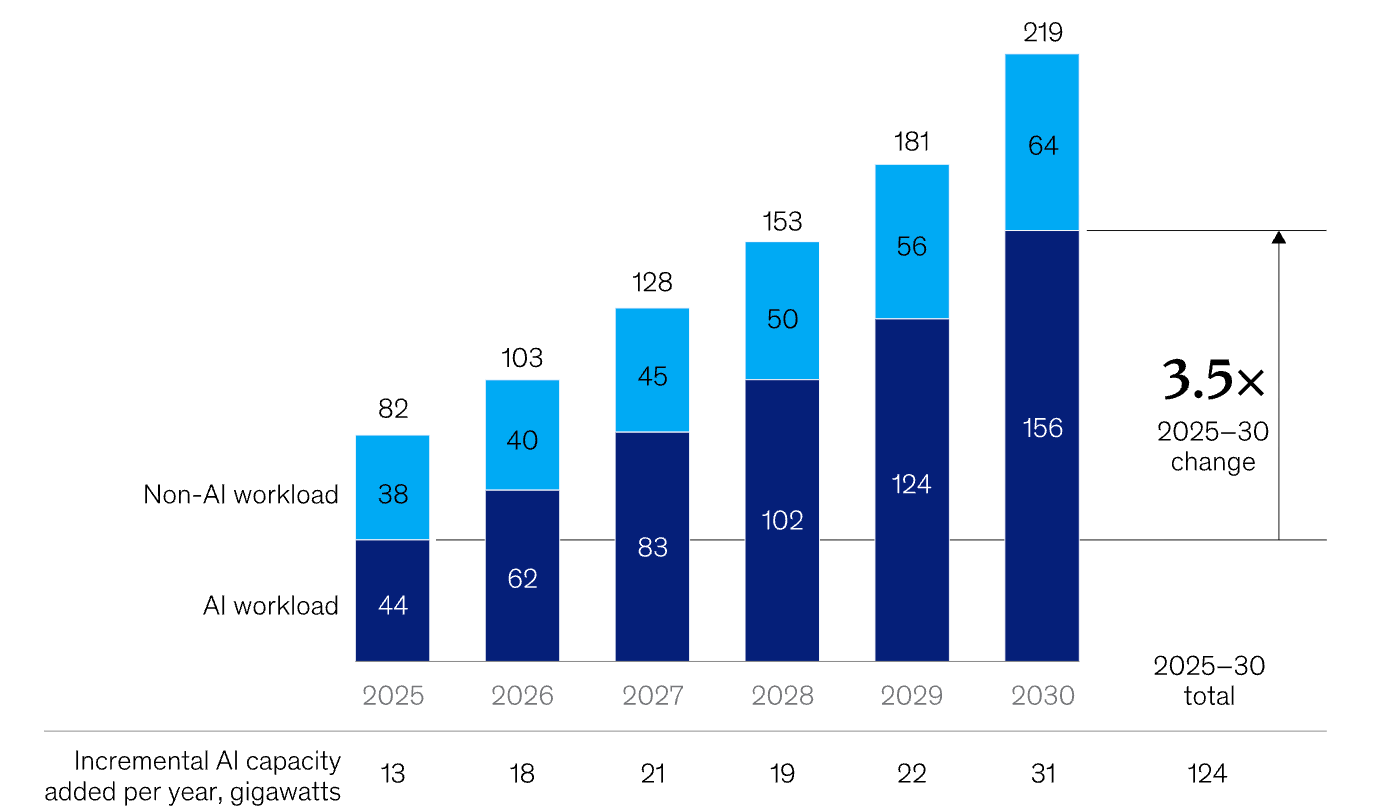

Forecasts are being rewritten. McKinsey estimates $7 trillion in AI infrastructure spending by 2030, with $5.2 trillion going toward data centres. According to McKinsey, we will also see significant incremental AI capacity added every year through to 2030.

Nvidia’s share of that pie could exceed 50%, given its current dominance and design lead. Some analysts even project a $20 trillion market capitalisation by 2030 if the company maintains its pace of innovation.

Still, this is not a frictionless ascent. Export restrictions to China and the rise of custom silicon from rivals like AMD and Google pose challenges. Yet Nvidia’s edge isn’t just its hardware - it’s the CUDA software ecosystem, which locks developers and enterprises into its platform. As long as AI workloads require versatility and performance across models and frameworks, Nvidia’s moat will hold.

Nvidia technical analysis

At the time of writing, Nvidia’s stock (NVDA) is hovering around $186, showing early signs of recovery after a short-term pullback. The RSI is rising sharply from the midline near 50, indicating that bullish momentum may be building as buying pressure intensifies.

Meanwhile, the Bollinger Bands are starting to narrow slightly, signalling a potential volatility squeeze that could precede a directional breakout. The price is currently positioned around the middle band, indicating a balance between buying and selling forces.

On the downside, support levels lie at $180 and $168. A drop below $180 may trigger further selling or stop-loss liquidations, while a break under $168 could confirm a deeper correction. On the upside, the key resistance sits at $208, where profit-taking and fresh buying activity are likely to intensify if the price breaks above it.

Key takeaway

Nvidia’s potential $300bn surge isn’t a sign of euphoria - it’s a reality check for those betting on an AI crash. The company’s results confirm that artificial intelligence has moved beyond the phase of promise into proof. As capital shifts from prototypes to platforms, the question isn’t whether AI will endure - it’s how fast it will reshape every market it touches. For now, Nvidia remains the pulse of that transformation.

For traders navigating that transformation, platforms like Deriv MT5 offer exposure to the tech rally’s next phase - while tools such as the Deriv trading calculator provide the precision to manage risk as the AI-driven market matures.

Sanctions vs supply glut: The battle defining Oil prices

Oil prices are caught in a tug-of-war that defines the entire energy narrative right now - sanctions versus surplus.

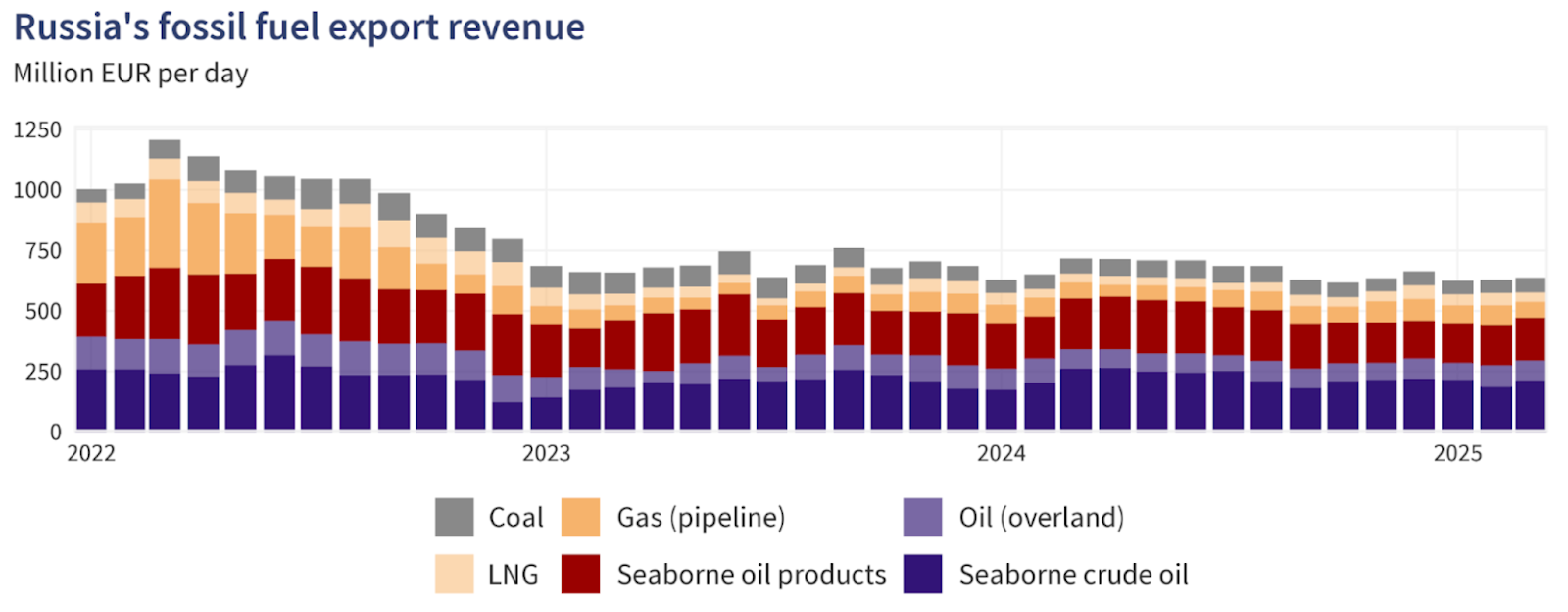

Oil prices are caught in a tug-of-war that defines the entire energy narrative right now - sanctions versus surplus. As Washington’s latest restrictions on Russian oil giants, such as Rosneft and Lukoil, take effect, traders are wondering whether this will finally squeeze supply enough to lift prices or if swelling inventories and record U.S. output will keep them grounded.

WTI crude has hovered near $60 in recent sessions, reflecting that same indecision. Every headline about sanctions sparks a flicker of optimism; every inventory report snuffs it out. The outcome of this standoff - between geopolitics and fundamentals - will decide whether oil’s next move is a breakout or another false dawn.

What’s driving the rebound

According to analysts, the recent oil bounce is largely fuelled by heightened concern over Russia’s export flows. In a press release issued by the U.S. Department of the Treasury, the United States and allied countries have imposed sweeping sanctions targeting major Russian oil producers, including Rosneft and Lukoil, along with hundreds of vessels from the “shadow fleet”.

These measures are designed to choke off Russia’s oil revenues and, by extension, reduce its export volumes. The logic is simple: fewer barrels from Russia = tighter global supply = higher prices. But the counter-force is significant: global supply remains robust, and demand isn’t bouncing back as expected.

According to the International Energy Agency (IEA), non-OPEC+ production is forecast to grow by 1.7 million barrels per day (bpd) in 2025, while demand growth is projected at just 0.79 million bpd, signalling a structural surplus unless changes occur.

Meanwhile, data show that Russia’s output and export adapt-workarounds remain effective so far - Russian production rose by about 100,000 bpd even after sanctions. Thus, the rebound is caught between a genuine supply shock narrative and a stubborn demand/stock overhang, and whether prices break out depends on which side prevails.

Why it matters

For traders, producers and consumers, this dynamic is far from academic. A sustained rally driven by supply constraints would favour oil-heavy portfolios, refining margins, and exporting nations. Conversely, if oversupply persists and demand disappoints, even the sanction narrative won’t save prices. As one senior energy analyst noted: “The market doesn’t expect much lost supply until enforcement becomes indisputable.”

For Russia and its global buyers, the stakes are high. Russia’s oil and gas revenues plunged by 27% in October 2025 compared to the same month a year earlier, reflecting the pressure of sanctions even as volumes held up through workarounds.

At the same time, major oil importers such as India and China have been increasing their Russian cargoes in recent months before the November plunge, which has cast doubts about continued oil flows to those countries.

So, if importers continue to absorb discounted Russian barrels, global supply may remain ample even though the narrative suggests otherwise. On the consumer end, if oil prices are kept low due to oversupply, fuel costs remain manageable. If supply loss dominates, refined-product prices (diesel, gasoline) could rise, feeding inflation and impacting economic growth - a risk to be watched for in both developed and emerging markets.

Impact on the market

In practical terms, the battle lines are drawn according to analysts. On the supply-risk side, if sanctions bite and Russian exports drop materially, markets may tighten quickly, and oil prices could rally.

The risk premium is already reflected in crude spreads: the discount for Russian Urals crude versus global benchmarks jumped to around US$19 per barrel by early November, as buyers shunned Russian cargoes, according to a report by Meduza. That suggests the sanction effect may be starting to crack.

But on the flip side, tracking data suggest that Russian flows are still being rerouted, and global producers (especially shale, Brazil and the U.S.) are responding. With U.S. production at record levels and inventories increasing, the oversupply story remains viable, according to industry commentators. If demand remains weak - for instance, from China or the global industry - then any supply-shock rally may be short-lived, and prices could retreat.

Refining and trade flows are also adjusting. Dealers and refiners are now considering discounted Russian crude, longer shipping routes, and higher freight and insurance costs - all of which increase complexity but don’t necessarily immediately reduce volumes. Until actual barrel losses show up in export data, the market may remain in limbo, reluctant to commit to strong upward momentum.

Expert outlook

According to analysts, the most probable scenario is a market stuck in a range-bound trading pattern, punctuated by bursts of volatility. That is, oil may temporarily rally on rumours of sanctions or supply disruptions, but unless demand proves stronger and supply genuinely tightens, the move may lack legs. Reuters reported that the IEA continues to expect supply growth outpacing demand this year.

If enforcement of sanctions tightens - for example, if shadow-fleet tankers are blocked, insurance costs spike or major importers pull back from Russian oil - then we could see a meaningful rally.

On the demand front, counter-signals to watch include refining run-rates (which remain under pressure), travel and mobility trends, and China’s petro-chemical demand. Until one of these breaks clearly favourably, the oversupply story will likely keep a lid on prices.

In short, the supply risk is real, but it hasn’t yet overridden the oversupply/weak-demand backdrop. Until that happens, the rally remains tentative.

Oil technical insights

At the time of writing, US Oil is trading around $59.50, consolidating within a narrow range as momentum starts to stabilise. The RSI is climbing sharply from the midline near 50, hinting at strengthening bullish momentum and suggesting that buyers may be regaining short-term control.

The Bollinger Bands (10, close) are relatively tight, signalling reduced volatility and the potential for a breakout. Price action remains centred around the middle band, showing indecision but with a slight upward bias as buyers attempt to push above the mid-range.

Key support levels are found at $58.26 and $56.85, where a break lower could trigger further selling pressure or stop-loss liquidations. On the upside, resistance sits at $62.00 and $65.00 - levels where profit-taking and stronger buying activity could emerge if the market breaks higher.

Key takeaway

The oil market is at a crossroads where the sanction-driven supply-risk narrative clashes with the solid structural reality of oversupply and weak demand. While the latest Russian sanctions have sharpened the risk premium, global production and inventories remain elevated and demand remains fragile.

Unless export losses are real and demand picks up, the oversupply story will likely keep oil prices pinned. The next key signals to monitor: export data from Russia, inventory changes globally and demand indicators from Asia and the U.S. Stay alert - this is a high-stakes battle that could tip either way.

For traders navigating the oil market, Deriv MT5 offers exposure to both WTI and Brent. Meanwhile, tools such as the Deriv trading calculator provide the precision needed to manage risk as the AI-driven market matures.

USD/JPY outlook: Can the Yen hold its ground amid Japan’s policy tug-of-war?

Reports indicate that the Japanese yen is struggling to maintain its stability as Japan’s fiscal and monetary priorities diverge in opposite directions.

Reports indicate that the Japanese yen is struggling to maintain its stability as Japan’s fiscal and monetary priorities diverge in opposite directions. A massive ¥25 trillion stimulus plan from Prime Minister Sanae Takaichi has reignited concerns about inflation and weighed on the currency, while the Bank of Japan’s cautious stance on rate hikes offers little support. The result is a yen pinned near a nine-month low, with the USD/JPY pair hovering around ¥155.

Many say Japan’s policy tug-of-war is tilting decisively against the yen. Unless the government and central bank find common ground, traders may see further weakness - especially if the dollar remains buoyed by a patient but firm Federal Reserve.

What’s driving USD/JPY

The yen’s weakness stems from a widening policy divide inside Japan’s leadership. Prime Minister Takaichi’s administration has revived Abenomics-style stimulus, prioritising fiscal expansion to boost wages and consumer demand.

Lawmakers have proposed a supplementary budget exceeding ¥25 trillion, stoking concerns over rising debt issuance and sending 40-year Japanese government bond yields to record highs.

Meanwhile, the Bank of Japan (BoJ) is caught between political pressure and macroeconomic caution. Inflation, currently around 2.9%, remains above target, yet the prime minister insists on keeping rates low until wage growth - not food or energy costs - drives price stability.

Governor Kazuo Ueda has hinted at tightening if inflation persists, but uneven growth complicates matters: GDP grew 1.1% year-on-year, yet contracted 0.4% quarter-on-quarter. This tug-of-war has left investors unsure whether Japan’s policies are reflating the economy or eroding its currency.

Why it matters

This internal conflict is redefining how global markets view the yen. Once seen as a safe-haven anchor, it’s now behaving more like a risk currency, moving with rather than against global sentiment. “Japan has added a tumultuous element - they’re a little more wild, a little more volatile,” said Juan Perez of Monex USA. That volatility reflects a new reality: fiscal expansion is now Japan’s dominant narrative, while monetary prudence takes a back seat.

For traders, the risk is that verbal intervention replaces actual action. Finance Minister Satsuki Katayama has expressed concern over the yen’s sharp depreciation, but Tokyo has so far refrained from stepping into the market. Intervention is likely only if USD/JPY breaches ¥156 decisively - a level seen as politically sensitive rather than economically critical by analysts.

Impact across markets

According to reports, the consequences of Japan’s fiscal-monetary split are evident across its bond and currency markets. The yield curve has steepened sharply as investors price in heavier debt issuance, while near-zero short-term rates keep domestic liquidity abundant. This imbalance encourages capital outflows, as investors seek higher yields abroad, further putting downward pressure on the yen.

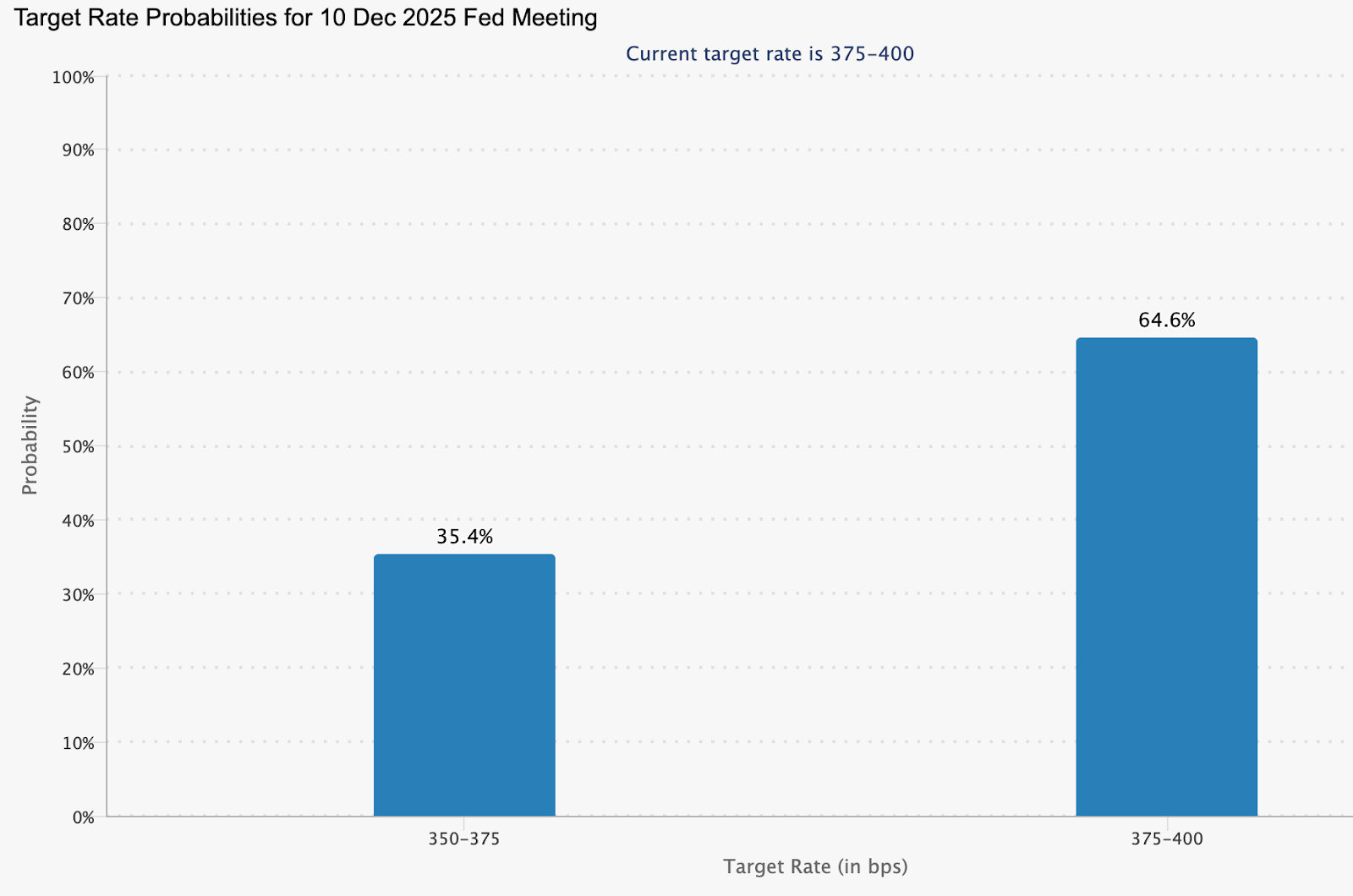

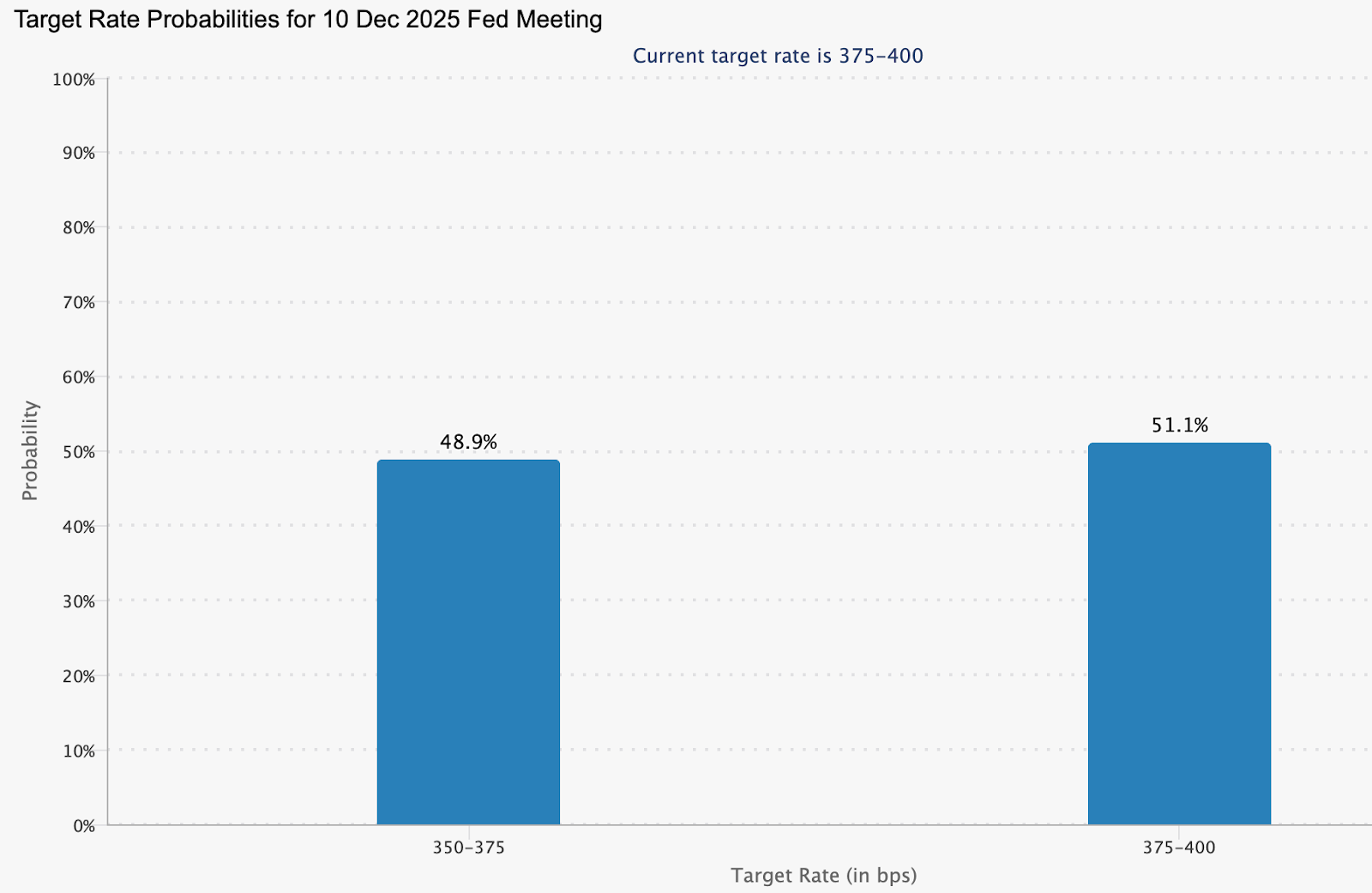

Across the Pacific, the Federal Reserve’s steadiness has reinforced dollar strength. Officials such as Philip Jefferson and Christopher Waller continue to advocate patience on rate cuts, trimming the probability of a December reduction to around 48%, down from 60% last week (CME FedWatch).

According to analysts, as long as this interest-rate gap persists, the dollar will remain structurally favoured against the yen, - and any yen rallies will likely prove temporary.

Expert outlook

Analysts see little relief for the yen in the near term. Barclays recommends holding a long position on the dollar against the yen, arguing that Takaichi’s expansionary agenda will suppress domestic yields and maintain downward pressure on the currency. Still, a sustained climb beyond ¥156 could test Tokyo’s resolve and force coordinated intervention.

The next key event is the delayed US Non-Farm Payrolls report, expected to provide fresh insight into labour market conditions. A weaker reading could trigger short-term dollar selling, allowing the yen to recover briefly. Yet without a policy shift in Japan, that reprieve may be short-lived. For now, the yen’s trajectory is dictated less by data and more by the dissonance between fiscal ambition and monetary caution.

USD/JPY technical insight

At the time of writing, USD/JPY is trading around 155.45, extending gains within a price discovery zone as bullish momentum persists. The pair is hugging the upper Bollinger Band, signalling strong buying pressure but also hinting at a possible overextension.

The RSI is climbing toward the overbought region, reinforcing the risk of a short-term pullback or profit-taking. Immediate support lies at 152.96, followed by 146.45, where a breakdown could trigger sell liquidations and accelerate downside movement.

However, as long as prices hold above the middle Bollinger Band and 153.00, the broader uptrend could remain intact, supported by policy divergence between the Federal Reserve and the Bank of Japan.

Key takeaway

Japan’s yen problem isn’t just about markets - it’s about messaging. Expansionary fiscal policy collides with a hesitant central bank, leaving investors unsure which signal to follow. The result is a currency under sustained strain, with verbal intervention doing little to stop the slide. Unless Tokyo finds alignment between stimulus and stability, the yen’s effort to hold its ground may remain more symbolic than successful.

Gold’s reversion to the mean: A pause before the next rally?

Gold has climbed back above $4,050 per ounce, stabilising after a sharp two-week selloff that pulled the metal down from record highs.

Gold has climbed back above $4,050 per ounce, stabilising after a sharp two-week selloff that pulled the metal down from record highs. The move reflects what analysts increasingly describe as a reversion to the mean - a natural correction following a steep run from $3,450 to $4,380 earlier in the quarter.

With the long-delayed US Non-Farm Payrolls (NFP) report now in focus, traders are watching whether this consolidation is a breather before the next leg up. The broader backdrop remains tense. Hawkish Federal Reserve remarks, delayed data from the US government shutdown, and continued geopolitical stress are all reshaping sentiment. Yet, behind the noise, gold’s pullback looks less like weakness - and more like equilibrium returning.

What’s driving gold’s mean reversion

The latest correction follows months of relentless buying, fuelled by soft US data, de-dollarisation flows, and record central-bank accumulation. Gold’s sprint from $3,450 to $4,380 outpaced fundamentals, leaving technical indicators stretched and sentiment euphoric.

Now, as traders recalibrate expectations for a December rate cut - pricing in a 48.9% chance according to CME FedWatch - the metal has slipped back toward its midrange, around $4,050–$4,100, where short-term and long-term averages converge.

This retreat also mirrors a psychological reset. Markets are digesting the Fed’s cautious tone, with Vice Chair Philip Jefferson urging a “slow approach” to policy changes and regional presidents Bostic and Schmid signalling preference for steady rates. Those comments, paired with delayed macro data, have thinned speculative positions and allowed gold to breathe. In effect, the market is rediscovering balance - a hallmark of mean reversion after an overextended move.

Why it matters

Gold’s mean reversion tells a deeper story about trust and monetary fatigue. As Citadel’s Ken Griffin noted, the rising price of gold reflects “a loss of trust first in US Treasuries, then in G7 bond markets.” Investors are responding not to short-term volatility, but to structural concerns about government debt and the stability of fiat currency.

Analysts at Deutsche Bank maintain that the medium-term trend remains intact, projecting an average gold price of $4,000 per ounce next year. They highlight “elevated official demand” - a reference to sustained central-bank buying.

In October, China’s central bank added 0.9 tonnes to its reserves, marking its 12th straight month of accumulation. Ongoing purchases throughout 2025 have lifted China’s official gold reserves to 2,304.5 tonnes.

This underlines that while traders may be reverting to the mean, nations are not - they’re steadily diversifying away from the dollar.

Impact across markets

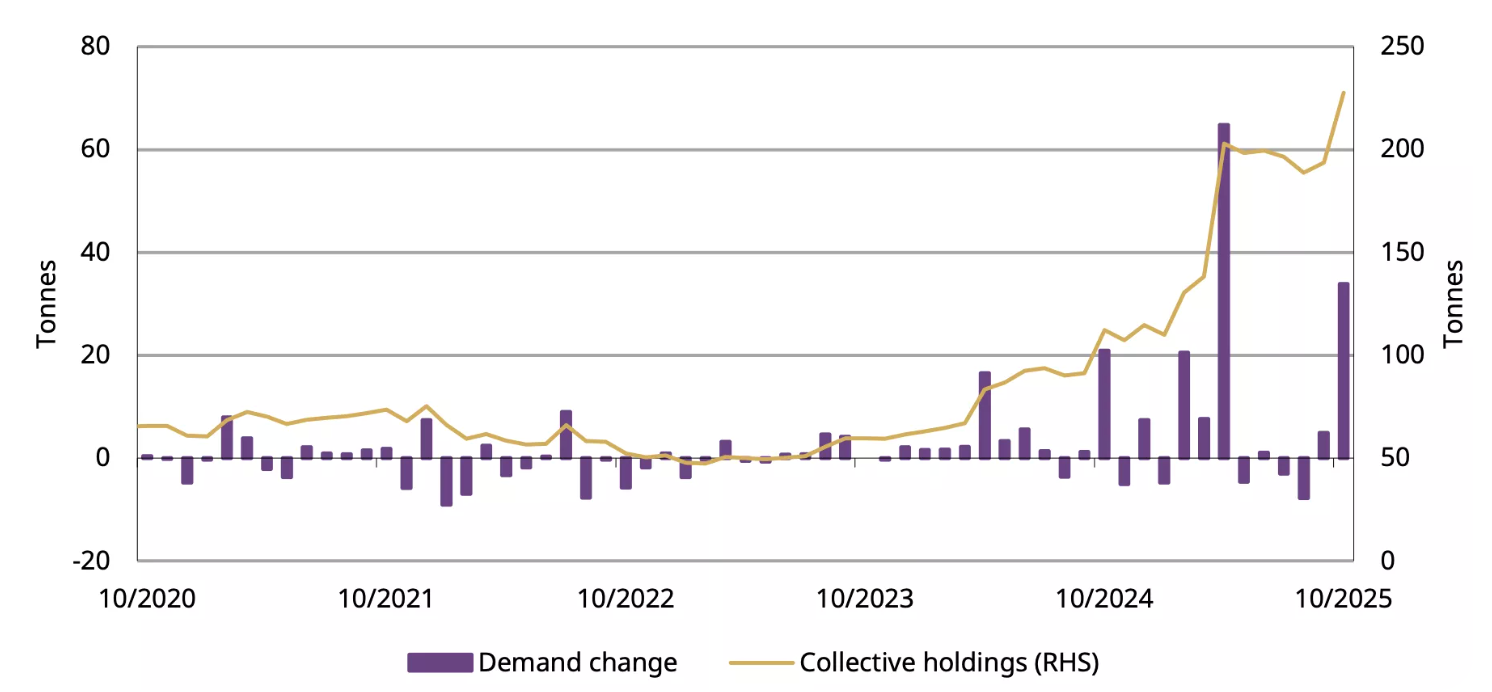

In China, investor appetite for gold remains vigorous even during the correction. ETF inflows jumped RMB 32 billion (US$4.5 billion) in October, pushing total holdings to a record 227 tonnes.

Physical demand, measured by withdrawals from the Shanghai Gold Exchange, rose 17 tonnes year-on-year to 124 tonnes, defying seasonal softness. The data suggests that investors see dips as opportunities, not red flags.

Globally, the story is similar. Soft US employment data and climbing jobless claims have tempered the dollar’s strength, nudging investors back into gold and silver.

Still, there’s awareness that a stronger NFP print or easing geopolitical risk could stall momentum. Even so, mean reversion isn’t a bearish event - it’s the market’s way of restoring order after a speculative sprint. And order, in uncertain times, is the most bullish foundation of all.

Expert outlook

Most analysts agree that gold’s medium-term trajectory remains higher, although near-term volatility will hinge on the US jobs data and the Fed’s stance in December. Independent trader Tai Wong says, “soft data is slightly boosting hopes for a December cut - helping gold and silver, which are trying to break a three-day losing streak.” That sentiment captures the current equilibrium: cautious optimism tempered by macro prudence.

If the NFP report underperforms, gold could swiftly retest $4,200, according to analysts. If it surprises to the upside, a dip toward $3,950 would complete a textbook mean reversion cycle before stabilising. Either way, the long-term bull case - driven by de-dollarisation, AI-driven labour disruption, and inflation inertia - remains intact. The question isn’t whether gold rises again, but when.

Gold technical analysis

At the time of writing, XAU/USD is trading near $4,088, rebounding from the lower Bollinger Band as buyers re-enter the market. The Bollinger Bands are beginning to widen after a period of contraction, suggesting that volatility may be returning.

The RSI is rising sharply from the midline, signalling improving bullish momentum. Key resistance levels are seen at $4,200 and $4,365, where profit-taking or further buying could occur if gold breaks higher. On the downside, a fall below $3,940 would likely trigger sell liquidations, exposing deeper support at $3,630.

Overall, gold appears to be in the early stages of a potential bullish continuation, with the technical setup hinting at renewed upside pressure if momentum sustains above the mid-Bollinger Band.

Key takeaway

Gold’s pullback to the $4,000 zone isn’t weakness - it’s rhythm. A reversion to the mean after a parabolic rise is how sustainable trends reset. Beneath short-term volatility, the drivers of this bull phase - de-dollarisation, central-bank accumulation, and macro distrust - remain fully in play. As the US jobs data and Fed decisions unfold, this pause could mark the quiet before gold’s next major rally.

Bitcoin crashes under $90K as ‘death cross’ bites

Spot prices printed as low as 89,420 dollars, the weakest level since February, only six weeks after setting a record near 126,250 dollars.

Bitcoin slipped below 90,000 dollars on Tuesday, extending a selloff that has erased its 2025 gains and pushed sentiment toward the bleak end of the spectrum. Spot prices printed as low as 89,420 dollars, the weakest level since February, only six weeks after setting a record near 126,250 dollars.

The breakdown coincided with a bearish technical crossover known as a death cross and increasingly hesitant fund flows into U.S. spot ETFs.

Together with macro anxiety around the rate path, these factors have tightened liquidity and amplified swings across majors. The next phase hinges on whether price can quickly reclaim lost support and whether ETF prints stabilise from recent choppiness.

What’s driving the slide

The proximate trigger is technical: Bitcoin fell back through reclaimed support near 93,700 dollars, lost its 200-day moving average, and then registered a death cross as the 50-day slipped beneath the 200-day.

On its own the signal is imperfect, but in weak liquidity regimes it often coincides with multi-week drawdowns as momentum traders de-risk.

Flows add fuel. U.S. spot ETF activity has turned choppy after heavy intake earlier in the year, with trackers showing sequences of outflows or flat prints that blunt marginal demand. When the incremental demand fades, price tends to chase lower liquidity pockets until new buyers emerge. Recent dashboards corroborate the stop-start nature of ETF demand. CoinDesk+1.

The Mt. Gox repayments - a trigger, not the cause

Adding fuel to the fire, over 10,600 BTC (worth roughly $953 million) were transferred from Mt. Gox wallets on 18 November 2025, marking the first such movement in eight months.

The long-running repayment saga, stemming from the 2014 collapse of the world’s then-largest exchange, has left creditors waiting over a decade for compensation.

While some feared that repayments could unleash fresh supply, blockchain data shows these movements were administrative, not market sales. Still, perception alone was enough to unsettle sentiment, sparking liquidations and feeding the broader risk-off tone. Analysts now estimate over 230,000 trading accounts were liquidated within 24 hours, totalling more than $1 billion in forced sell orders.

Why this matters

Sentiment has swung hard into fear. CoinDesk flagged “extreme fear” conditions into the weekend and early week, aligning with widely followed gauges that punish downside volatility and negative breadth. In past cycles, similar extremes have marked acceleration phases within larger drawdowns or short-lived exhaustion points.

The macro overlay is not helping. Traders are parsing shifting expectations for U.S. rate cuts and inflation risks tied to policy developments, a mix that reduces risk appetite and tightens crypto liquidity. Reuters’ read-across captures the mood: a near 30 percent retreat from the October peak and growing caution among institutions.

Impact on markets and participants

Price leadership rotated back to bitcoin as traders sold altcoins to manage risk, a pattern visible when social attention and volumes consolidate in the benchmark asset during stress. Ether and other large caps have tracked lower alongside, while crypto-linked equities have generally underperformed on drawdown days, transmitting crypto volatility into listed proxies.

For allocators, ETF prints serve as the cleanest real-time barometer of spot demand. Multi-day flat or negative flows often coincide with fragility in order books and heavier slippage, which is why desks are laser-focused on whether the next sequence turns positive again. If it doesn’t, the unfilled liquidity pocket toward 86,000–88,000 dollars cited by traders continues to be a live risk.

Expert outlook

CoinDesk’s market desk notes that fear spikes of this magnitude have sometimes preceded relief rallies, particularly when realised-loss pressure begins to stabilise and ETF outflows slow. That requires confirmation: a swift reclaim of broken support and evidence of renewed net inflows. Until then, technicals and positioning argue for elevated two-way volatility.

Long-horizon investors continue to point at structural adoption and institutional participation as reasons to stay constructive on multi-year horizons. Dan Tapiero, whose 50T platform backs later-stage crypto companies, frames short-term turbulence as noise against a secular build-out, a view he has reiterated while forecasting a much larger digital-asset economy over the next decade.

Bitcoin price technical insight

Bitcoin (BTC/USD) continues its downward trajectory after forming a death cross, with the 50-day moving average (MA) crossing below the 200-day MA - a classic bearish signal suggesting extended downside pressure. The price is currently hovering near $91,000, after repeatedly failing to hold above key resistance levels at $106,685, $114,000, and $124,650, where prior rallies saw heavy profit-taking and FOMO-driven buying.

The Relative Strength Index (RSI) has dipped into oversold territory, indicating that selling momentum may be overextended and a short-term technical rebound could occur. However, as long as BTC remains below the 50-day MA, the broader trend remains bearish, with traders likely to view any bounce as a chance to sell into strength.

Key takeaway

Bitcoin’s slide below $90,000 reflects a convergence of technical breakdown, hesitant ETF demand, and a risk-off macro tone. The resulting fear spike is typical of late-stage selloffs, but it needs flow confirmation before calling a durable low. Watch for a quick reclaim of the $ 90,000 - $93,000 zone and a run of positive ETF prints to validate any rebound attempt. Until then, expect elevated volatility and tighter liquidity conditions.

죄송합니다. 와(과) 일치하는 결과를 찾을 수 없습니다.

검색 팁:

- 철자를 확인하고 다시 시도해 주세요

- 다른 키워드로 시도해 보세요