Wyniki dla

USD/JPY unosi się w strefie zagrożenia: Czy Japonia może powstrzymać wzrost do 160?

USD/JPY unosi się w tym, co handlowcy nazywają teraz „strefą zagrożenia” - przedziałem 155—160, który wcześniej wymuszał Japonię do ręki.

USD/JPY unosi się w tym, co handlowcy nazywają teraz „strefą zagrożenia” - przedziałem 155—160, który wcześniej wymuszał Japonię do ręki. Według analityków para testuje poziomy, które w przypadku naruszenia mogą zmusić Tokio do ponownej interwencji w obronie jena. Dla rynków jest to nie tylko próg psychologiczny; to linia wyznaczona przez historię. Każdy krok bliżej 160 ożywia wspomnienia przeszłych interwencji i spekulacji na temat tego, jak daleko Japonia pozwoli osłabić swoją walutę, zanim wkroczy.

Raporty wskazują, że u podstaw napięcia leży rosnąca rozbieżność między ekspansją fiskalną Japonii a jej ostrożną postawą monetarną. Plan stymulacyjny premiera Sanae Takaichi o wartości 21,3 biliona jenów (112 mld funtów) zwiększył rentowności i jeszcze bardziej osłabił jena, podobnie jak Stany Zjednoczone utrzymują wysokie stopy procentowe.

Pytanie brzmi teraz, czy Japonia może - czy zrobi - działać na czas, aby zatrzymać wzrost USD/JPY, zanim przebije się przez 160 i przetestuje determinację Tokio na arenie globalnej.

Co napędza USD/JPY?

Ostatni spadek jena jest zakorzeniony w rosnącej luce politycznej Japonii ze Stanami Zjednoczonymi. Bodziec Takaichi, największy od czasu pandemii, obejmuje wydatki na ulgi energetyczne, ulgi podatkowe i materiały pieniężne. Ma na celu złagodzenie presji związanych z kosztami utrzymania, ale inwestorzy postrzegają ją jako inflacyjną i lekkomyślną fiskalną. Bloomberg poinformował, że rentowności japońskich obligacji rządowych (JGB) wzrosły do najwyższego poziomu od 2008 roku, ponieważ pogłębiają się obawy o zadłużenie i słabnie zaufanie do długoterminowej dyscypliny fiskalnej

Ostrożne stanowisko Banku Japonii tylko wzmocniło presję. Gubernator Kazuo Ueda nadal twierdzi, że wzrost płac musi ustabilizować się przed jakąkolwiek poważną zmianą polityki, nawet jeśli inflacja pozostaje powyżej celu 2 procent.

Natomiast Rezerwa Federalna utrzymuje podwyższone stopy procentowe w USA i pozostaje niechętna do szybkich cięć. Ta różnica rentowności sprawia, że posiadanie dolarów jest bardziej satysfakcjonujące, wysyłając kapitał wypływający z jena i utrzymując USD/JPY w pobliżu wieloletnich maksimum.

Dlaczego to ma znaczenie

Obserwatorzy rynku twierdzą, że słabość jena zmniejsza się w obie strony. Łagodniejsza waluta przynosi korzyści eksporterom takim jak Toyota i Sony, których zagraniczne zarobki przekładają się na wyższe zyski. Jednak dla importerów i gospodarstw domowych ból jest natychmiastowy. Japonia w dużej mierze opiera się na importowanym paliwie i żywności, co oznacza, że każdy wzrost wartości USD/JPY sprawia, że codzienne życie jest droższe. „Jen w realnym ujęciu jest prawie tak słaby jak lira turecka” - ostrzegł Robin Brooks z Brookings Institution, opisując stanowisko fiskalne rządu jako „odmowę długu”.

Poza granicami Japonii jen służy jako globalny barometr nastrojów na ryzyko. Kiedy gwałtownie słabnie, sygnalizuje rosnące zaufanie do dolara i ośmiela strategie handlu przenośnego finansowane w jenach. Ale zwiększa to również ryzyko nagłych odwróceń, jeśli interweniuje Tokio. Rynki wciąż przypominają okres połowy roku, kiedy Japonia podobno wydała ponad 60 miliardów dolarów na obronę swojej waluty po tym, jak USD/JPY na krótko przekroczył 160. To dziedzictwo sprawia, że każdy ruch w tym zespole wydaje się odliczaniem.

Wpływ na rynki i strategię

Na rynkach obligacji inwestorzy domagają się wyższych rentowności, aby zrównoważyć ryzyko fiskalne, zwiększając dziesięcioletnie stopy JGB powyżej 1%, a czterdziestoletnie rentowności powyżej 3,6 procent. Wzrost ten odzwierciedla obawy, że dług Japonii - już ponad dwukrotnie większy od jej gospodarki - będzie dalej wzrastał w ramach programu prowzrostowego Takaichiego.

Minister finansów Satsuki Katayama ostrzegł już, że rząd „będzie działał przeciwko nieuporządkowanym ruchom”, zdanie, które handlowcy interpretują teraz jako zawoalowane zagrożenie interwencją.

Dla inwestorów akcji słabszy jen przyniósł krótkoterminowy impuls. Nikkei 225 osiągnął najwyższy poziom od dziesięcioleci, wspierany przez duże akcje eksportowe i nieoczekiwane zyski zagraniczne.

Jednak wiąże się to ze swoją kosztą: zaufanie konsumentów spadło, a oczekiwania inflacyjne rosną. Globalnie miękkość jena napędza apetyt na ryzyko - paliwo dla akcji, a nawet kryptowalut - ale pozostawia rynki podatne na ostrą korektę, jeśli Tokio lub BoJ nagle zmienią postawę.

Dla handlowców detalicznych ta zmienność stanowi szansę i ryzyko w równym stopniu. Przy dużej zmienności wokół kluczowych poziomów niezbędne stają się zdyscyplinowane ustalanie wielkości pozycji i śledzenie depozytu zabezpieczającego - narzędzia takie jak Kalkulator pochodnych może pomóc traderom oszacować wartości pipsów, wielkość kontraktów oraz potencjalny zysk lub stratę przed wejściem na rynek.

Perspektywy ekspertów

Prognozy dla USD/JPY zależą od czasu. Jeśli BoJ podniesie stopy procentowe do 0.75 procent w grudniu, jak spodziewa się niewielka większość ekonomistów, jen może spowodować wzrost ulgi z powrotem w kierunku 150.

Jeśli jednak bank centralny opóźni, a dane z USA pozostaną stabilne, inwestorzy mogą kontynuować testowanie górnej granicy zakresu. „Stymulacja Sanae Takaichi w stylu Abenomics zwiększy globalną płynność i wzmocni dolara - King Dollar żyje i ma się dobrze” - powiedział James Thorne z Wellington Altus.

Wiele zależy od tego, czy Fed przesunie się przed BoJ. Rynki kontraktów terminowych wyceniają obecnie 75.5% szans na obniżkę stóp procentowych w USA w grudniu.

Analitycy dodali również, że dovish Fed może zmniejszyć lukę rentowności i wywołać zakup jena. Ale jeśli tego nie ma, japońska waluta pozostaje zakładnikiem bezwładności polityki i globalnych nastrojów. Im dłużej USD/JPY pozostaje blisko 160, tym większa presja na Tokio, aby udowodnić, że nadal wzbudza szacunek rynku.

Spostrzeżenia techniczne USD/JPY

W chwili pisania tego tekstu USD/JPY utrzymuje się blisko 156.66, konsolidując się w strefie wykrywania cen po rozszerzeniu zwyżkowy biegać. Pasma Bollingera (10, zamknięcie) poszerzają się, wykazując zwiększoną zmienność i ciągłe nastawienie, ponieważ akcja cenowa pozostaje blisko górnego pasma - znak silnego pędu zwyżkowego, ale także zwiększonego ryzyka krótkoterminowego wyczerpania.

Kluczowe strefy wsparcia mieszczą się na poziomie 154.00, 150.00 i 146.60, gdzie przełamanie poniżej każdej z nich może spowodować likwidację sprzedaży i głębsze korekty. Z drugiej strony odkrycie cen powyżej 156.00 pozostawia ograniczony opór, co oznacza, że kolejne wycofania mogą przyciągnąć kupujących spadek, chyba że zmienność wzrośnie.

The RSI (14) wspina się do strefy wykupu, co sugeruje, że siła zwyżkowa może zbliżyć się do szczytu. Jeśli wskaźnik RSI utrzymuje odczyt powyżej 70, pęd może wzrosnąć; jednak każde odwrócenie poniżej tego poziomu może wskazywać na osiągnięcie zysków lub wczesną presję sprzedaży.

Klucz na wynos

Według analityków powrót USD/JPY do korytarza 155—160 jest czymś więcej niż wzorcem wykresów; jest to referendum w sprawie mieszanki politycznej Japonii. Ekspansja fiskalna bez dopasowanej korekty monetarnej sprawiła, że jen jest bezbronny, a inwestorzy są sceptyczni. Interwencja może na krótko ustabilizować rynki, ale tylko zdecydowane zaostrzenie lub ograniczenie fiskalne przywrócą zaufanie. Do tego czasu para znajduje się prosto w strefie zagrożenia - gdzie każdy ruch podnosi test nie tylko tolerancji Tokio, ale także wiarę świata w zdolność Japonii do kontrolowania własnej waluty.

Rekordowy kwartał Nvidii spotyka się z chłodną reakcją rynku

Pomimo wzrostu Nvidii i podniesionej prognozy na około 65 miliardów dolarów w kolejnym kwartale, reakcja rynku była zaskakująco powściągliwa.

Gdy Nvidia Corporation ogłosiła przychody za trzeci kwartał na poziomie 57 miliardów dolarów – wzrost o 62% rok do roku – wydawało się, że to kolejny bezbłędny triumf w wyścigu sprzętu AI. Jednak mimo tego wzrostu i podniesionej prognozy na około 65 miliardów dolarów w kolejnym kwartale, reakcja rynku była zaskakująco powściągliwa.

Podczas wycieku z wewnętrznego spotkania CEO Jensen Huang przyznał: „Rynek tego nie docenił.” Ta rozbieżność między realizacją a entuzjazmem pokazuje, jak wysokie oczekiwania – i euforia wokół AI – podniosły poprzeczkę nawet dla najlepszych.

Co napędza rekordowy kwartał Nvidii

Siłą napędową wyników Nvidii pozostaje popyt na centra danych – fundament infrastruktury AI. Sam ten segment wygenerował około 51 miliardów dolarów przychodu, co oznacza wzrost o 66% rok do roku i 25% kwartał do kwartału.

Flagowe produkty, takie jak platforma Blackwell, nadal dominują w zamówieniach korporacyjnych, a prognozy wskazują na kolejny rekordowy kwartał – 65 miliardów dolarów przychodu, 65% wzrost rok do roku. Nvidia nie tylko rośnie; wyznacza tempo całego cyklu inwestycji kapitałowych w branży.

Wzrost ten potęgują siły geopolityczne i strukturalne. W miarę jak chmura, robotyka i systemy autonomiczne rozwijają się na całym świecie, sprzęt Nvidii znajduje się w centrum innowacji – i w wąskim gardle podaży. Jednak wraz z sukcesem pojawia się kruchość: gdy perfekcja staje się normą, najmniejsze potknięcie wydaje się wstrząsem. „Gdy przyzwyczaisz rynek do perfekcji,” żartował jeden z analityków, „nawet świetny wynik nie wystarcza.”

Dlaczego to ma znaczenie

Nvidia stanowi obecnie około 7,31% całkowitej wagi S&P 500, co czyni ją najważniejszym barometrem nastrojów wokół AI. Tak duża spółka, która po rekordowym kwartale porusza się w bok, sugeruje, że inwestorzy kwestionują nie dane, lecz narrację.

FinancialContent nazwał to „próbą ognia dla AI i szerokiego rynku”. Jeśli doskonałość Nvidii już nie ekscytuje, reszta branży technologicznej odczuje chłód.

Sam Huang ujął to jasno: jeśli dostarczysz słaby kwartał, obwiniają cię o przebicie bańki; jeśli świetny – oskarżają o jej pompowanie. Ta pułapka percepcji podkreśla nową fazę w handlu AI – taką, w której wyniki muszą być ponadprzeciętne, by poruszyć rynki. Odzwierciedla to także subtelną zmianę: od szumu i obietnic do dyscypliny i realizacji.

Wpływ na ekosystem technologii i AI

Wyniki Nvidii początkowo podniosły notowania akcji technologicznych, a AMD, Broadcom i dostawcy pamięci korzystali z optymizmu. Jednak w miarę upływu dnia te wzrosty się ulotniły – co dowodzi, że entuzjazm stał się kruchy.

Według analityków, jeśli potężne wyniki nie wywołują już rajdu, oznacza to, że większość wzrostu infrastruktury AI jest już uwzględniona w cenach. Inwestorzy mogą teraz nagradzać efektywność operacyjną zamiast samej ekspansji. To naturalna ewolucja: gdy wzrost dojrzewa, na pierwszy plan wysuwa się dyscyplina wyceny.

Dla nabywców sprzętu i użytkowników korporacyjnych ta ewolucja może oznaczać nieco łatwiejszą dostępność, ale ostrzejsze ceny. Wyzwanie dla Nvidii to utrzymanie marż przy zwiększaniu produkcji – przejście od wizjonerskiego wzrostu do przemysłowej precyzji.

Perspektywy ekspertów

Obserwatorzy rynku wskazują na dwa możliwe scenariusze. Jeśli Nvidia będzie nadal skutecznie działać – rozwijając nowe linie produktów, zwiększając moce produkcyjne i radząc sobie z ryzykiem eksportowym – może utrzymać pozycję lidera i przedłużyć swoją passę. Firma wciąż posiada technologiczną fosę, którą niewielu jest w stanie przekroczyć.

Drugi scenariusz to korekta wyceny: jeśli inwestorzy zaczną się zastanawiać, czy wzrost sprzętu może stale wyprzedzać inflację kosztów i konkurencję, Nvidia może napotkać plateau. Jak ujął to jeden z analityków Bernstein: „Nie wiem, czego więcej można oczekiwać, przynajmniej po tych wynikach.”

Dla traderów sygnałami do obserwacji są trendy w prognozach, aktualizacje portfela zamówień (szczególnie w Chinach) oraz tempo wdrażania chipów Rubin i Blackwell. Wahania kapitalizacji rynkowej o pół biliona dolarów w ciągu kilku tygodni pokazują, jak wrażliwe stały się nastroje.

Techniczne spojrzenie na Nvidię

W chwili pisania tego tekstu Nvidia (NVDA) notowana jest w okolicach 194,50 USD, odbijając się od dolnego pasma Bollingera po przetestowaniu wsparcia na poziomie 179,70 USD. Pasma Bollingera (10, zamknięcie) umiarkowanie się rozszerzają – co oznacza wzrost zmienności – a kurs zbliża się do linii środkowej. Sugeruje to potencjalną kontynuację ruchu w kierunku górnego pasma w krótkim terminie.

Poziom 173,20 USD wyróżnia się jako kolejne kluczowe wsparcie; jego przebicie może wywołać likwidacje pozycji i wzmocnić presję spadkową. Z drugiej strony, 208,00 USD tworzy silną strefę oporu, gdzie w przypadku przedłużenia rajdu mogą pojawić się zarówno realizacja zysków, jak i późne zakupy pod wpływem FOMO.

Wskaźniki momentum wzmacniają byczy scenariusz. RSI (14) gwałtownie skierował się w górę, przekraczając linię środkową w okolicach 50 – to techniczny sygnał odnowionej presji zakupowej. Utrzymanie się powyżej tego poziomu, wsparte stabilizacją powyżej 179,70 USD, potwierdziłoby krótkoterminowy trend wzrostowy i ponownie przyciągnęło traderów szukających ruchów momentum.

Dla tych, którzy rozważają różne scenariusze, kalkulator Deriv może być przydatny do symulacji zysków i strat przy różnych ustawieniach zmienności – to niezbędne uzupełnienie analizy wykresów przy planowaniu transakcji NVDA na Deriv MT5.

Najważniejsze wnioski

Inwestorzy postrzegają Nvidię jako pozostającą w centrum boomu infrastruktury AI – finansowo bezkonkurencyjną i technologicznie dominującą. Jednak letnia reakcja rynku wyznacza punkt zwrotny: inwestorzy nie nagradzają już obietnic, a jedynie dowody. W tej nowej fazie handlu AI o przywództwie zdecydują realizacja, odporność marż i tempo innowacji. Dla traderów wykres Nvidii może sugerować krótkoterminowy potencjał wzrostowy, ale większa historia to zmiana oczekiwań – gdzie perfekcja jest teraz standardem, a nie zaskoczeniem.

Perspektywa cen złota: banki centralne zapewniają parę

Pod hałasem słabnących zakładów na obniżenie stóp procentowych i siły dolara kryje się głębsza siła strukturalna: nieustanne kupowanie złota przez światowe banki centralne.

Według raportów niezwykła stabilność złota w pobliżu 4050 USD za uncję nie jest przypadkiem. Pod hałasem słabnących zakładów obniżających stawki i siły dolara kryje się głębsza siła strukturalna: nieustanne kupowanie przez światowe banki centralne. Od Pekinu po Ankarę decydenci po cichu przepisują zasady bezpieczeństwa monetarnego, wykorzystując złoto jako zabezpieczenie przed ryzykiem politycznym, niestabilnością walutową i słabnącym zaufaniem do amerykańskiego porządku finansowego.

Według analityków popyt ten stał się niewidzialną ręką wspierającą kruszce. Nawet gdy spekulacyjni inwestorzy wycofują się, a przepływy ETF spłaszczają się, suwerenni nabywcy pomagają zakotwiczyć rynek.

Ponieważ Ludowy Bank Chin przedłuża 12-miesięczną passę kupowania złota, a inne banki centralne podążają za tym, ryzyko spadku złota wygląda teraz bardziej na przerwę niż upadek - piętro wzmocnione przez narody, a nie fundusze.

Co w tej chwili napędza złoto?

Najnowsze dane o zatrudnieniu w USA zresetowały oczekiwania na rynkach światowych. Wrześniowy raport Nonfarm Payrolls wykazał wzrost o 119 000 miejsc pracy, ponad dwukrotnie więcej niż oczekiwali ekonomiści, podczas gdy bezrobocie wzrosło do 4,4 proc.

Na pierwszy rzut oka dane wydają się mieszane - silne zatrudnienie, ale łagodzące tempo - ale wystarczyły, aby skłonić inwestorów do oddzwonienia od Rezerwy Federalnej w sprawie grudniowej obniżki stóp procentowych.

Ta ponowna kalibracja podniosła rentowności dolara i USA, zazwyczaj toksyczne połączenie złota. Ale metal ledwo się wzdrygnął. Powodem jest to, że popyt banków centralnych zmienił wrażliwość złota na cykle polityki.

Według danych Światowej Rady Złota, oficjalne zakupy sektorowe stanowią obecnie prawie jedną czwartą rocznego popytu - strukturalna zmiana w porównaniu z dekadą sprzed dekady. Kiedy Fed się waha, banki centralne tego nie robią.

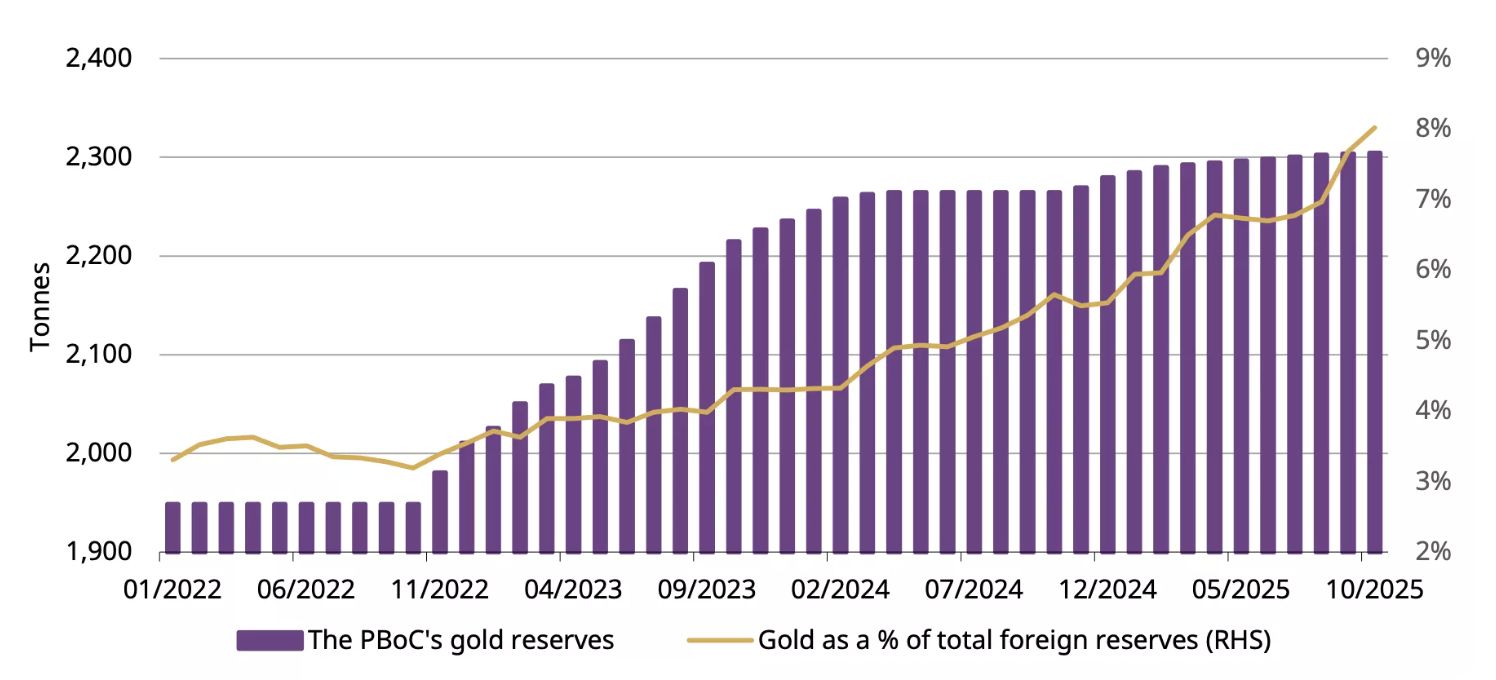

Ludowy Bank Chin (PBoC) odnotował zakupy złota przez 12 kolejnych miesięcy, dodając w październiku 0.9 tony, co podniosło łączną kwotę do 2,304 mln, co stanowi 8% chińskich rezerw walutowych i oznacza cały rok nieprzerwanego zakupu. Turcja, Polska i Indie przyłączyły się do trendu akumulacji.

Dlaczego to ma znaczenie

Obserwatorzy rynku twierdzą, że ta cicha akumulacja suwerenności zmienia rolę złota w globalnym systemie finansowym. To, co kiedyś było handlem „wyłączeniem ryzyka”, jest teraz częścią krajowej strategii rezerw. Zamrożenie rosyjskich aktywów zagranicznych w 2022 roku skłoniło rządy do ponownej oceny swojej ekspozycji na system zdominowany przez dolar, a złoto stało się neutralną alternatywą.

Jak ujął strateg Zaner Metals Peter Grant, najnowsze dane o zatrudnieniu w USA „potwierdzają spowolnienie, ale stabilny rynek - ale to nie zmniejsza apetytu na bezpieczeństwo”.

Dla decydentów na rynkach wschodzących złoto oferuje coś, czego papierowe aktywa nie potrafią: izolację od sankcji, inflacji i polityki walutowej. Dla inwestorów oznacza to, że cena złota nie jest już wyłącznie funkcją stóp procentowych lub apetytu na ryzyko. Jest to wskaźnik geopolityczny - odzwierciedlenie tego, jak duże zaufanie pozostaje w obecnym porządku monetarnym.

Wpływ na rynki i inwestorów

Najbardziej uderzającą zmianą w tym cyklu jest to, że złoto utrzymuje się blisko rekordowych szczytów, nawet gdy indeks dolara amerykańskiego (DXY) utrzymuje się na najsilniejszym poziomie od miesięcy. Tradycyjny odwrotny związek osłabł. Według analityków oba aktywa są kupowane z tego samego powodu: bezpieczeństwa. Ta dynamika podważa ideę, że złoto rośnie tylko wtedy, gdy stopy spadają.

Dla traderów komplikuje to pozycjonowanie krótkoterminowe. Ponieważ złoto jest teraz o około 7% poniżej październikowego rekordu wynoszącego 4380 USD, tempo ostygło, ale popyt strukturalny pozostaje nienaruszony. Przepływy ETF, choć w ostatnich tygodniach lekko ujemne, nie wykazują oznak paniki.

Inwestorzy detaliczni zmniejszyli ekspozycję, ale oficjalny sektor zastąpił ich jako nabywcę marginalnego. Dla inwestorów długoterminowych zmiana ta sugeruje, że wycofania mogą dawać szanse, a nie ostrzeżenia, zwłaszcza jeśli niepewność makroekonomiczna pogłębi się do 2026 roku.

Perspektywy ekspertów

Analitycy pozostają podzieleni co do tego, jak daleko ta oferta banku centralnego może przenieść metal. Goldman Sachs nadal postrzega ostatnią słabość jako „upadek, a nie odwrócenie”, utrzymując, że zarówno popyt na inwestycje suwerenne, jak i prywatne będą podtrzymywać ceny do 2026 roku. UBS przewiduje możliwy wzrost do 4900 USD za uncję w ciągu najbliższych dwóch lat, zakładając dalszą dywersyfikację z dala od rezerw dolarowych.

Głównym zagrożeniem dla tej perspektywy jest samozadowolenie pieniężne. Jeśli dane z USA pozostaną stabilne, a Fed potwierdzi swoją pozycję „wyższą na dłużej”, spekulacyjne zainteresowanie może jeszcze bardziej zanikać. Ale na razie odporność złota mówi sama za siebie. Rynek dostosowuje się do nowej rzeczywistości - takiej, w której ton nadają banki centralne, a nie handlowcy.

Złote spostrzeżenia techniczne

W momencie pisania tego tekstu złoto (XAU/USD) handluje wokół regionu 4,030 USD, unosząc się w pobliżu poziomu wsparcia 4,020 USD. The RSI jest płaski i blisko linii środkowej, co wskazuje na brak silnego pędu w obu kierunkach - znak niezdecydowania rynku.

Tymczasem Zespoły Bollingera zaczęły się zawężać, odzwierciedlając niższą zmienność po ostatnich wahaniach. Cena oscyluje w pobliżu środkowego pasma, co sugeruje potencjalną fazę konsolidacji przed następnym wybuchem.

Z drugiej strony, 4,200 USD i 4,365 USD pozostają kluczowymi poziomami oporu, gdzie inwestorzy mogą spodziewać się zysków lub odnowienia odsetek zakupowych, jeśli powrócą nastroje zwyżkowe. I odwrotnie, przełamanie poniżej 4020 USD może otworzyć drzwi do wsparcia w wysokości 3,940 USD, gdzie może wystąpić zwiększona presja sprzedaży lub likwidacja.

Kluczowe wnioski

Odporność złota pod koniec 2025 roku nie jest tajemnicą - jest to przesłanie wyrażone przez analityków. Te same instytucje, które kiedyś zaufały amerykańskim skarbom, kupują teraz kruszce, aby zabezpieczyć się przed polityką, polityką i niepewnością. Handlowcy mogą osłabić rajd, ale banki centralne nie wzdrygają się. Jako Fed porusza się po podzielonej perspektywie polityki, a globalne rezerwy nadal przesuwają się na wschód, podłoga pod złotem wygląda tak mocno, jak trzymające je ręce.

.png)

Bitcoin’s harsh reset: Flows, fear and two lines that matter

The world’s largest cryptocurrency has shed nearly a third of its value since its October peak, slipping toward critical technical levels as headwinds take effect.

Bitcoin’s harsh reset has arrived. The world’s largest cryptocurrency has shed nearly a third of its value since its October peak, slipping toward critical technical levels as exchange-traded fund outflows and macroeconomic headwinds take effect.

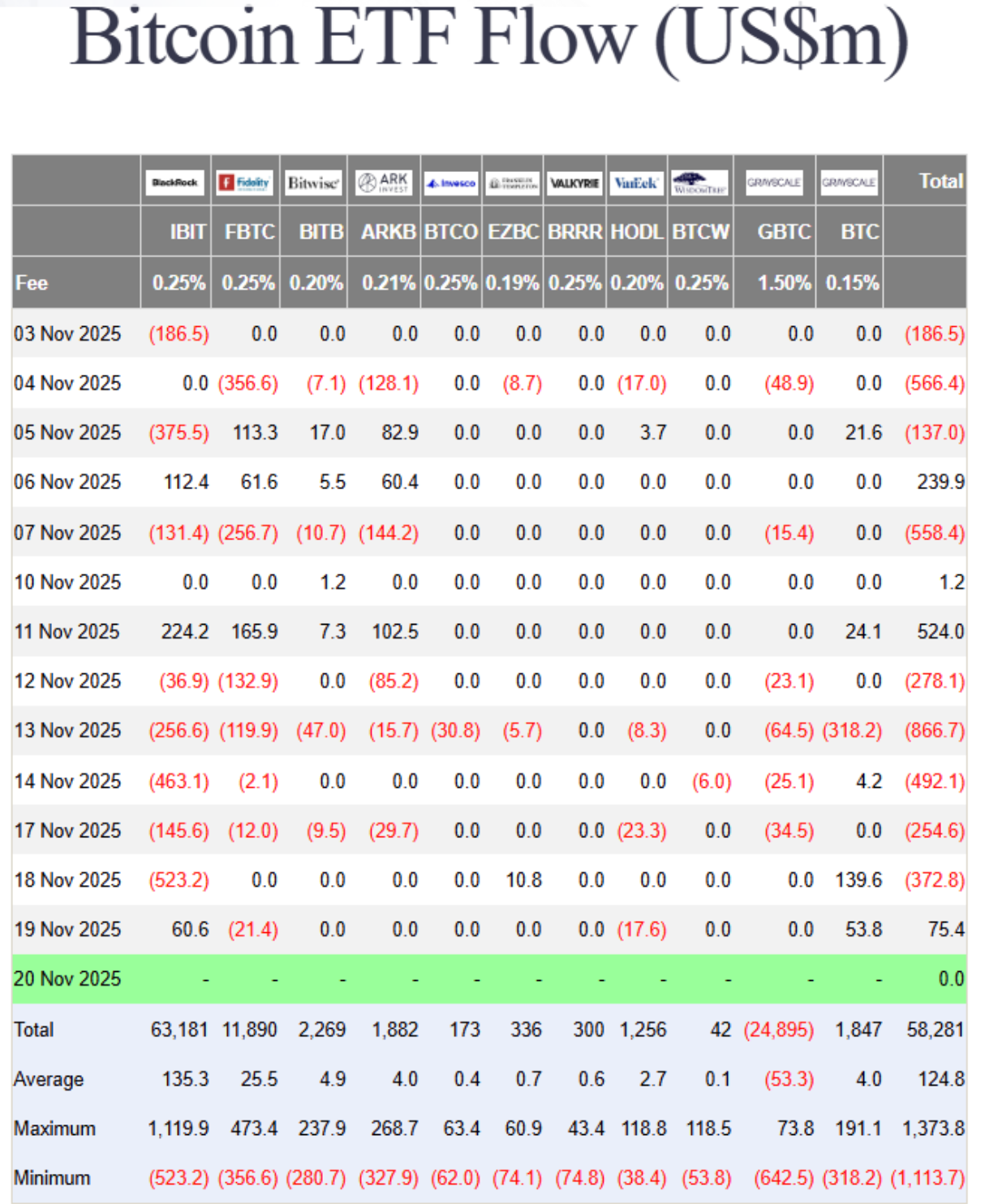

Recent data showed nearly $3 billion has exited Bitcoin ETFs this month alone, turning the same institutional flows that once fuelled the rally into a feedback loop of redemptions and retreat.

Behind the selloff lies a mix of fading Fed-rate-cut hopes, tightening liquidity, and a market paralysed by “extreme fear”. With prices hovering near $85,600 and the one-year low at $74,000 looming, the question is simple but urgent: is this correction a passing flush - or the start of a deeper shift in Bitcoin’s new ETF era?

What’s driving Bitcoin’s correction

Bitcoin’s 30% slide isn’t being driven by scandal or shock - it’s the result of structural forces finally reversing, according to analysts. After two years of relentless inflows, spot Bitcoin ETFs are now experiencing capital outflows. Institutional investors, once hailed as crypto’s stabilisers, are showing how quickly sentiment turns when markets wobble.

According to Farside data, ETF redemptions have occurred on all but four days this month, stripping nearly $3 billion in net outflows.

Part of that retreat stems from shifting macro conditions. The Federal Reserve’s reluctance to confirm rate cuts has strengthened the US dollar, drawing liquidity away from speculative assets.

Past movements have shown that a stronger dollar typically weighs on Bitcoin, and with inflation readings still sticky, traders are reassessing the narrative of “easy money” returning in December. The result is a market where rallies are met with selling rather than enthusiasm - a sharp turn from the euphoria that drove Bitcoin to $126,000 just weeks ago.

Why it matters

Bitcoin’s selloff is revealing just how tightly traditional and digital markets are now intertwined. ETFs opened the floodgates for institutional exposure, but they also linked Bitcoin to broader risk trends. When investors pull money from ETF products, the effect ricochets through liquidity pools and sentiment alike.

As Matt Williams of Luxor explained, “The drop to $86,000 is largely driven by macro forces - rate expectations, inflation - and by large holders cutting exposure after breaking key technical supports.”

For traders, this is a psychological turning point. The same retail crowd that once flooded exchanges during Thanksgiving 2017 - when Bitcoin first crossed $10,000 - is largely silent now.

Social data from Santiment shows sentiment evenly split between predictions of a plunge below $70,000 and wild optimism for a rally to $130,000. The divide signals indecision, not conviction. In this phase, fear - not fundamentals - is setting the tone.

Impact on markets and investors

The selloff has spilled beyond the crypto space. Bitcoin’s correlation with equity indices, such as the Nasdaq 100, has climbed above 0.8 at times, meaning that moves in tech stocks and digital assets now feed off the same macro triggers. When rate optimism fades, both markets suffer. That link cuts against Bitcoin’s long-standing claim as a hedge against monetary risk.

ETF outflows are another pressure point. As funds are redeemed, liquidity providers are compelled to unwind their positions in futures and spot markets, thereby deepening volatility.

The Crypto Fear & Greed Index, which plunged to 14 this week - its lowest since February - underscores how rapidly sentiment has deteriorated. Analysts like Rachael Lucas of BTC Markets warn that momentum, money flow, and volume trends “all reflect a sharp deterioration in sentiment,” driven by macro tightening and risk-off positioning.

In the background, liquidity providers are struggling. Tom Lee of Fundstrat compared crypto market makers to “central banks” of digital liquidity - and right now, those banks are running dry.

Following October’s $20 billion liquidation wave, market makers are operating with smaller balance sheets, which limits their ability to absorb order flow. It’s a reminder that crypto’s plumbing, though more sophisticated, is still fragile.

Expert outlook

Analysts are torn between caution and curiosity. Nic Puckrin of Coin Bureau describes the current landscape as a “bull-bear tug of war,” with macroeconomic pessimism offset by resilience in the tech sector.

Nvidia’s earnings beat briefly lifted risk appetite, but Bitcoin failed to follow through, suggesting traders are still unwinding rather than reloading. Puckrin pegs the next resistance at $107,500, if a rebound can gain traction.

Andre Dragosch of Bitwise sees parallels to past mid-cycle corrections, noting that the depth and duration of this decline “remain consistent with interim pullbacks in previous bull markets.” His base case still anticipates the cycle extending into 2026, driven by gradual global monetary easing.

For now, though, short-term risk remains tilted lower, with $85,600 and $74,000 as the two critical levels to watch. Hold those, and Bitcoin could form a base; lose them, and the next flush could be swift.

The bigger picture: Could Bitcoin trigger a financial crisis?

Despite the panic, Bitcoin remains relatively small compared to the real financial system. The total crypto market stands around $3–4 trillion, with Bitcoin representing roughly half. In contrast, global financial assets exceed $400 trillion. Past collapses, such as FTX in 2022 and Terra in 2021, caused chaos within the crypto industry but barely rippled across global markets.

That said, every cycle pulls crypto closer to traditional finance. ETFs, corporate holdings, and stablecoins backed by US Treasuries have created real linkages. A severe Bitcoin crash could trigger ETF redemptions, hurt balance sheets at companies holding BTC, and pressure stablecoins to liquidate their Treasury assets. None of that would cause a 2008-style crisis today - but as the overlap grows, the line between “crypto crash” and “financial contagion” gets thinner.

Bitcoin technical insights

At the time of writing, Bitcoin (BTC/USD) is trading around the $84,200 mark after an extended downtrend. The RSI has plunged sharply into oversold territory, signalling intense bearish momentum and the potential for a short-term relief bounce if buyers step in.

A death cross - where the 50-day moving average has fallen below the 200-day moving average - reinforces the bearish bias, suggesting further downside pressure in the near term.

Key resistance levels sit at $106,260, $115,200, and $123,950, where traders may expect profit-taking or renewed buying interest if recovery attempts occur. Failure to reclaim these zones could see Bitcoin remain under pressure, with sentiment staying fragile amid persistent selling.

Key takeaways

Bitcoin’s decline isn’t an accident - it’s a stress test of its new reality. The ETF era has tied the cryptocurrency closer to the global financial system, for better and worse. Liquidity, once a tailwind, now cuts both ways. Fear dominates, but deep corrections are part of Bitcoin’s DNA.

If those two lines - $85,600 and $74,000 - hold firm, many say this reset may end up looking like just another cleansing phase before the next wave of institutional demand. Lose them, and Bitcoin’s harsh reset could turn into something much deeper.

Nvidia earnings reality check: Is the AI boom back on track?

Nvidia’s latest earnings didn’t inflate another round of hype; they restored confidence that artificial intelligence is entering its scale phase.

Yes - the AI boom is back on track, according to analysts, just in a different gear. Nvidia’s latest earnings didn’t inflate another round of hype; they restored confidence that artificial intelligence is entering its scale phase, not its speculative one.

Nvidia investors are bracing for a $300 billion surge in market value after the chipmaker reported its first sales acceleration in seven quarters, signalling that AI demand isn’t fading - it’s normalising into a sustainable growth cycle.

For months, markets were haunted by talk of “peak AI.” However, Nvidia’s results - record data centre revenue, renewed partnerships, and a 5% share spike in after-hours trading - show the story isn’t one of collapse, but calibration. This isn’t a bubble bursting; it’s the industry learning how to breathe again.

What’s driving Nvidia’s momentum

At the core of Nvidia’s dominance in artificial intelligence architecture is its data centre segment, which surpassed $50 billion this quarter, a milestone reached earlier than analysts expected.

This reflects an industrial-scale buildout, not a speculative frenzy. The surge in demand from AI workloads has transformed GPUs from niche products into the backbone of modern computing, powering everything from ChatGPT to enterprise cloud systems.

CEO Jensen Huang captured it best: “We’re in every cloud.” That ubiquity underpins Nvidia’s stability. Its chips are not optional - they’re essential infrastructure. With Blackwell GPUs offering up to 40 times faster inference speeds than the previous generation, the company isn’t chasing hype; it’s engineering the next leap in computational efficiency.

Why it matters

Nvidia’s report acts as a barometer for the AI economy. The stock’s post-earnings rally wasn’t just about profits; it was about validation. The market had priced in fear after days of tech sell-offs, but Nvidia’s blowout numbers reintroduced realism.

Analysts like Julian Emanuel of Evercore ISI summed up the pre-earnings tension: “The angst around ‘peak AI’ has been palpable.” Those fears evaporated when Nvidia showed that demand isn’t flattening - it’s broadening.

The company’s performance has become closely tied to the trajectory of U.S. equities. With AI now a structural growth driver, Nvidia’s consistency reassures investors that this is an economic revolution in progress, not a fleeting mania. Its $5 trillion valuation last month wasn’t an aberration; it was a preview of scale yet to come.

Impact on global markets

The aftershocks were immediate. Tech indices that had stumbled under the weight of “AI fatigue” rebounded as Nvidia reignited investor faith. Asian markets opened higher, and S&P futures turned positive, driven by renewed conviction that the AI trade still has legs. Even after a period of correction - Meta down 19%, Oracle off 20% - Nvidia’s performance reaffirmed that the long-term AI thesis remains intact.

Beyond markets, Nvidia’s results signal a new capital cycle. Its multibillion-dollar partnerships with Microsoft, OpenAI, and Anthropic aren’t one-off investments; they’re structural commitments to an AI-driven infrastructure era. Every dollar of GPU spending feeds into an ecosystem that’s building capacity for the next generation of models, data centres, and intelligent services.

Expert outlook

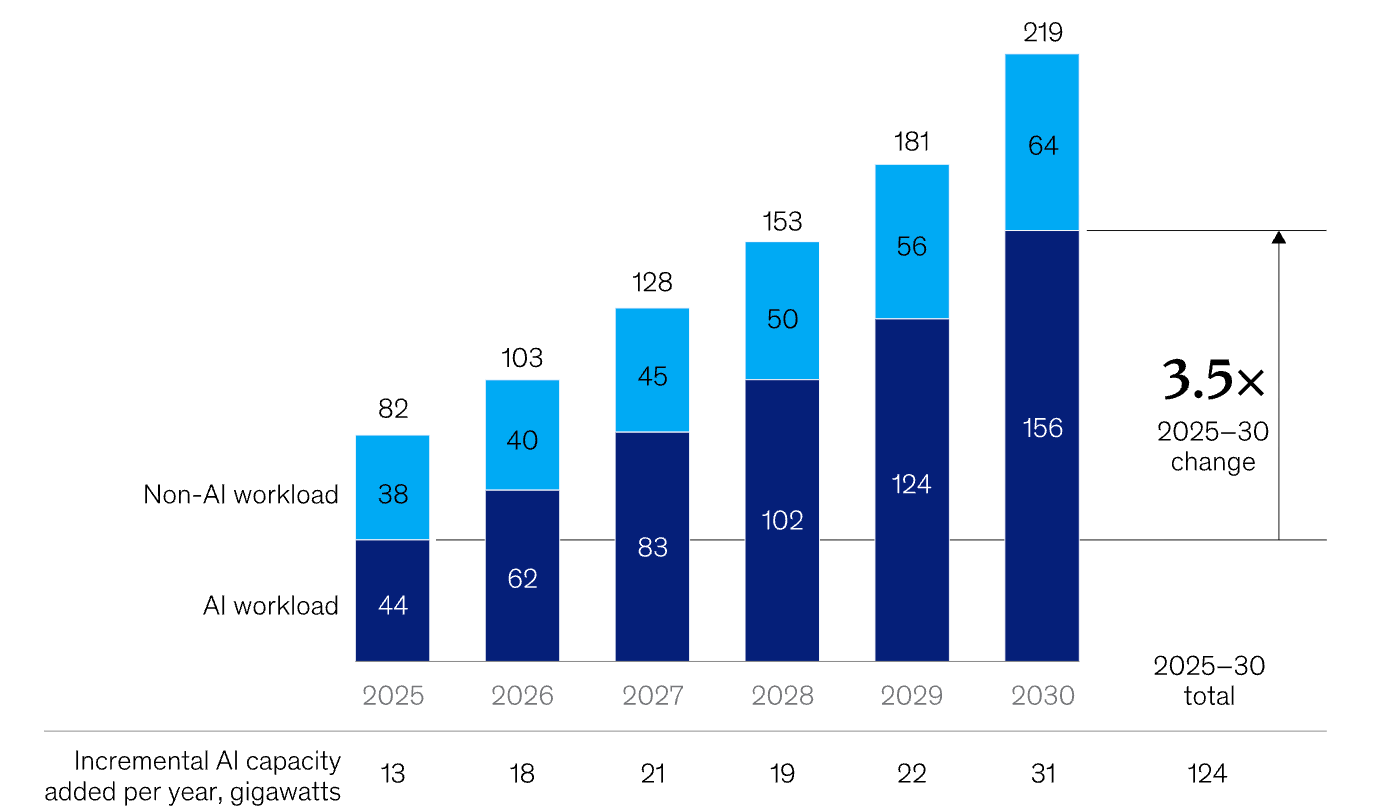

Forecasts are being rewritten. McKinsey estimates $7 trillion in AI infrastructure spending by 2030, with $5.2 trillion going toward data centres. According to McKinsey, we will also see significant incremental AI capacity added every year through to 2030.

Nvidia’s share of that pie could exceed 50%, given its current dominance and design lead. Some analysts even project a $20 trillion market capitalisation by 2030 if the company maintains its pace of innovation.

Still, this is not a frictionless ascent. Export restrictions to China and the rise of custom silicon from rivals like AMD and Google pose challenges. Yet Nvidia’s edge isn’t just its hardware - it’s the CUDA software ecosystem, which locks developers and enterprises into its platform. As long as AI workloads require versatility and performance across models and frameworks, Nvidia’s moat will hold.

Nvidia technical analysis

At the time of writing, Nvidia’s stock (NVDA) is hovering around $186, showing early signs of recovery after a short-term pullback. The RSI is rising sharply from the midline near 50, indicating that bullish momentum may be building as buying pressure intensifies.

Meanwhile, the Bollinger Bands are starting to narrow slightly, signalling a potential volatility squeeze that could precede a directional breakout. The price is currently positioned around the middle band, indicating a balance between buying and selling forces.

On the downside, support levels lie at $180 and $168. A drop below $180 may trigger further selling or stop-loss liquidations, while a break under $168 could confirm a deeper correction. On the upside, the key resistance sits at $208, where profit-taking and fresh buying activity are likely to intensify if the price breaks above it.

Key takeaway

Nvidia’s potential $300bn surge isn’t a sign of euphoria - it’s a reality check for those betting on an AI crash. The company’s results confirm that artificial intelligence has moved beyond the phase of promise into proof. As capital shifts from prototypes to platforms, the question isn’t whether AI will endure - it’s how fast it will reshape every market it touches. For now, Nvidia remains the pulse of that transformation.

For traders navigating that transformation, platforms like Deriv MT5 offer exposure to the tech rally’s next phase - while tools such as the Deriv trading calculator provide the precision to manage risk as the AI-driven market matures.

Sanctions vs supply glut: The battle defining Oil prices

Oil prices are caught in a tug-of-war that defines the entire energy narrative right now - sanctions versus surplus.

Oil prices are caught in a tug-of-war that defines the entire energy narrative right now - sanctions versus surplus. As Washington’s latest restrictions on Russian oil giants, such as Rosneft and Lukoil, take effect, traders are wondering whether this will finally squeeze supply enough to lift prices or if swelling inventories and record U.S. output will keep them grounded.

WTI crude has hovered near $60 in recent sessions, reflecting that same indecision. Every headline about sanctions sparks a flicker of optimism; every inventory report snuffs it out. The outcome of this standoff - between geopolitics and fundamentals - will decide whether oil’s next move is a breakout or another false dawn.

What’s driving the rebound

According to analysts, the recent oil bounce is largely fuelled by heightened concern over Russia’s export flows. In a press release issued by the U.S. Department of the Treasury, the United States and allied countries have imposed sweeping sanctions targeting major Russian oil producers, including Rosneft and Lukoil, along with hundreds of vessels from the “shadow fleet”.

These measures are designed to choke off Russia’s oil revenues and, by extension, reduce its export volumes. The logic is simple: fewer barrels from Russia = tighter global supply = higher prices. But the counter-force is significant: global supply remains robust, and demand isn’t bouncing back as expected.

According to the International Energy Agency (IEA), non-OPEC+ production is forecast to grow by 1.7 million barrels per day (bpd) in 2025, while demand growth is projected at just 0.79 million bpd, signalling a structural surplus unless changes occur.

Meanwhile, data show that Russia’s output and export adapt-workarounds remain effective so far - Russian production rose by about 100,000 bpd even after sanctions. Thus, the rebound is caught between a genuine supply shock narrative and a stubborn demand/stock overhang, and whether prices break out depends on which side prevails.

Why it matters

For traders, producers and consumers, this dynamic is far from academic. A sustained rally driven by supply constraints would favour oil-heavy portfolios, refining margins, and exporting nations. Conversely, if oversupply persists and demand disappoints, even the sanction narrative won’t save prices. As one senior energy analyst noted: “The market doesn’t expect much lost supply until enforcement becomes indisputable.”

For Russia and its global buyers, the stakes are high. Russia’s oil and gas revenues plunged by 27% in October 2025 compared to the same month a year earlier, reflecting the pressure of sanctions even as volumes held up through workarounds.

At the same time, major oil importers such as India and China have been increasing their Russian cargoes in recent months before the November plunge, which has cast doubts about continued oil flows to those countries.

So, if importers continue to absorb discounted Russian barrels, global supply may remain ample even though the narrative suggests otherwise. On the consumer end, if oil prices are kept low due to oversupply, fuel costs remain manageable. If supply loss dominates, refined-product prices (diesel, gasoline) could rise, feeding inflation and impacting economic growth - a risk to be watched for in both developed and emerging markets.

Impact on the market

In practical terms, the battle lines are drawn according to analysts. On the supply-risk side, if sanctions bite and Russian exports drop materially, markets may tighten quickly, and oil prices could rally.

The risk premium is already reflected in crude spreads: the discount for Russian Urals crude versus global benchmarks jumped to around US$19 per barrel by early November, as buyers shunned Russian cargoes, according to a report by Meduza. That suggests the sanction effect may be starting to crack.

But on the flip side, tracking data suggest that Russian flows are still being rerouted, and global producers (especially shale, Brazil and the U.S.) are responding. With U.S. production at record levels and inventories increasing, the oversupply story remains viable, according to industry commentators. If demand remains weak - for instance, from China or the global industry - then any supply-shock rally may be short-lived, and prices could retreat.

Refining and trade flows are also adjusting. Dealers and refiners are now considering discounted Russian crude, longer shipping routes, and higher freight and insurance costs - all of which increase complexity but don’t necessarily immediately reduce volumes. Until actual barrel losses show up in export data, the market may remain in limbo, reluctant to commit to strong upward momentum.

Expert outlook

According to analysts, the most probable scenario is a market stuck in a range-bound trading pattern, punctuated by bursts of volatility. That is, oil may temporarily rally on rumours of sanctions or supply disruptions, but unless demand proves stronger and supply genuinely tightens, the move may lack legs. Reuters reported that the IEA continues to expect supply growth outpacing demand this year.

If enforcement of sanctions tightens - for example, if shadow-fleet tankers are blocked, insurance costs spike or major importers pull back from Russian oil - then we could see a meaningful rally.

On the demand front, counter-signals to watch include refining run-rates (which remain under pressure), travel and mobility trends, and China’s petro-chemical demand. Until one of these breaks clearly favourably, the oversupply story will likely keep a lid on prices.

In short, the supply risk is real, but it hasn’t yet overridden the oversupply/weak-demand backdrop. Until that happens, the rally remains tentative.

Oil technical insights

At the time of writing, US Oil is trading around $59.50, consolidating within a narrow range as momentum starts to stabilise. The RSI is climbing sharply from the midline near 50, hinting at strengthening bullish momentum and suggesting that buyers may be regaining short-term control.

The Bollinger Bands (10, close) are relatively tight, signalling reduced volatility and the potential for a breakout. Price action remains centred around the middle band, showing indecision but with a slight upward bias as buyers attempt to push above the mid-range.

Key support levels are found at $58.26 and $56.85, where a break lower could trigger further selling pressure or stop-loss liquidations. On the upside, resistance sits at $62.00 and $65.00 - levels where profit-taking and stronger buying activity could emerge if the market breaks higher.

Key takeaway

The oil market is at a crossroads where the sanction-driven supply-risk narrative clashes with the solid structural reality of oversupply and weak demand. While the latest Russian sanctions have sharpened the risk premium, global production and inventories remain elevated and demand remains fragile.

Unless export losses are real and demand picks up, the oversupply story will likely keep oil prices pinned. The next key signals to monitor: export data from Russia, inventory changes globally and demand indicators from Asia and the U.S. Stay alert - this is a high-stakes battle that could tip either way.

For traders navigating the oil market, Deriv MT5 offers exposure to both WTI and Brent. Meanwhile, tools such as the Deriv trading calculator provide the precision needed to manage risk as the AI-driven market matures.

USD/JPY outlook: Can the Yen hold its ground amid Japan’s policy tug-of-war?

Reports indicate that the Japanese yen is struggling to maintain its stability as Japan’s fiscal and monetary priorities diverge in opposite directions.

Reports indicate that the Japanese yen is struggling to maintain its stability as Japan’s fiscal and monetary priorities diverge in opposite directions. A massive ¥25 trillion stimulus plan from Prime Minister Sanae Takaichi has reignited concerns about inflation and weighed on the currency, while the Bank of Japan’s cautious stance on rate hikes offers little support. The result is a yen pinned near a nine-month low, with the USD/JPY pair hovering around ¥155.

Many say Japan’s policy tug-of-war is tilting decisively against the yen. Unless the government and central bank find common ground, traders may see further weakness - especially if the dollar remains buoyed by a patient but firm Federal Reserve.

What’s driving USD/JPY

The yen’s weakness stems from a widening policy divide inside Japan’s leadership. Prime Minister Takaichi’s administration has revived Abenomics-style stimulus, prioritising fiscal expansion to boost wages and consumer demand.

Lawmakers have proposed a supplementary budget exceeding ¥25 trillion, stoking concerns over rising debt issuance and sending 40-year Japanese government bond yields to record highs.

Meanwhile, the Bank of Japan (BoJ) is caught between political pressure and macroeconomic caution. Inflation, currently around 2.9%, remains above target, yet the prime minister insists on keeping rates low until wage growth - not food or energy costs - drives price stability.

Governor Kazuo Ueda has hinted at tightening if inflation persists, but uneven growth complicates matters: GDP grew 1.1% year-on-year, yet contracted 0.4% quarter-on-quarter. This tug-of-war has left investors unsure whether Japan’s policies are reflating the economy or eroding its currency.

Why it matters

This internal conflict is redefining how global markets view the yen. Once seen as a safe-haven anchor, it’s now behaving more like a risk currency, moving with rather than against global sentiment. “Japan has added a tumultuous element - they’re a little more wild, a little more volatile,” said Juan Perez of Monex USA. That volatility reflects a new reality: fiscal expansion is now Japan’s dominant narrative, while monetary prudence takes a back seat.

For traders, the risk is that verbal intervention replaces actual action. Finance Minister Satsuki Katayama has expressed concern over the yen’s sharp depreciation, but Tokyo has so far refrained from stepping into the market. Intervention is likely only if USD/JPY breaches ¥156 decisively - a level seen as politically sensitive rather than economically critical by analysts.

Impact across markets

According to reports, the consequences of Japan’s fiscal-monetary split are evident across its bond and currency markets. The yield curve has steepened sharply as investors price in heavier debt issuance, while near-zero short-term rates keep domestic liquidity abundant. This imbalance encourages capital outflows, as investors seek higher yields abroad, further putting downward pressure on the yen.

Across the Pacific, the Federal Reserve’s steadiness has reinforced dollar strength. Officials such as Philip Jefferson and Christopher Waller continue to advocate patience on rate cuts, trimming the probability of a December reduction to around 48%, down from 60% last week (CME FedWatch).

According to analysts, as long as this interest-rate gap persists, the dollar will remain structurally favoured against the yen, - and any yen rallies will likely prove temporary.

Expert outlook

Analysts see little relief for the yen in the near term. Barclays recommends holding a long position on the dollar against the yen, arguing that Takaichi’s expansionary agenda will suppress domestic yields and maintain downward pressure on the currency. Still, a sustained climb beyond ¥156 could test Tokyo’s resolve and force coordinated intervention.

The next key event is the delayed US Non-Farm Payrolls report, expected to provide fresh insight into labour market conditions. A weaker reading could trigger short-term dollar selling, allowing the yen to recover briefly. Yet without a policy shift in Japan, that reprieve may be short-lived. For now, the yen’s trajectory is dictated less by data and more by the dissonance between fiscal ambition and monetary caution.

USD/JPY technical insight

At the time of writing, USD/JPY is trading around 155.45, extending gains within a price discovery zone as bullish momentum persists. The pair is hugging the upper Bollinger Band, signalling strong buying pressure but also hinting at a possible overextension.

The RSI is climbing toward the overbought region, reinforcing the risk of a short-term pullback or profit-taking. Immediate support lies at 152.96, followed by 146.45, where a breakdown could trigger sell liquidations and accelerate downside movement.

However, as long as prices hold above the middle Bollinger Band and 153.00, the broader uptrend could remain intact, supported by policy divergence between the Federal Reserve and the Bank of Japan.

Key takeaway

Japan’s yen problem isn’t just about markets - it’s about messaging. Expansionary fiscal policy collides with a hesitant central bank, leaving investors unsure which signal to follow. The result is a currency under sustained strain, with verbal intervention doing little to stop the slide. Unless Tokyo finds alignment between stimulus and stability, the yen’s effort to hold its ground may remain more symbolic than successful.

Gold’s reversion to the mean: A pause before the next rally?

Gold has climbed back above $4,050 per ounce, stabilising after a sharp two-week selloff that pulled the metal down from record highs.

Gold has climbed back above $4,050 per ounce, stabilising after a sharp two-week selloff that pulled the metal down from record highs. The move reflects what analysts increasingly describe as a reversion to the mean - a natural correction following a steep run from $3,450 to $4,380 earlier in the quarter.

With the long-delayed US Non-Farm Payrolls (NFP) report now in focus, traders are watching whether this consolidation is a breather before the next leg up. The broader backdrop remains tense. Hawkish Federal Reserve remarks, delayed data from the US government shutdown, and continued geopolitical stress are all reshaping sentiment. Yet, behind the noise, gold’s pullback looks less like weakness - and more like equilibrium returning.

What’s driving gold’s mean reversion

The latest correction follows months of relentless buying, fuelled by soft US data, de-dollarisation flows, and record central-bank accumulation. Gold’s sprint from $3,450 to $4,380 outpaced fundamentals, leaving technical indicators stretched and sentiment euphoric.

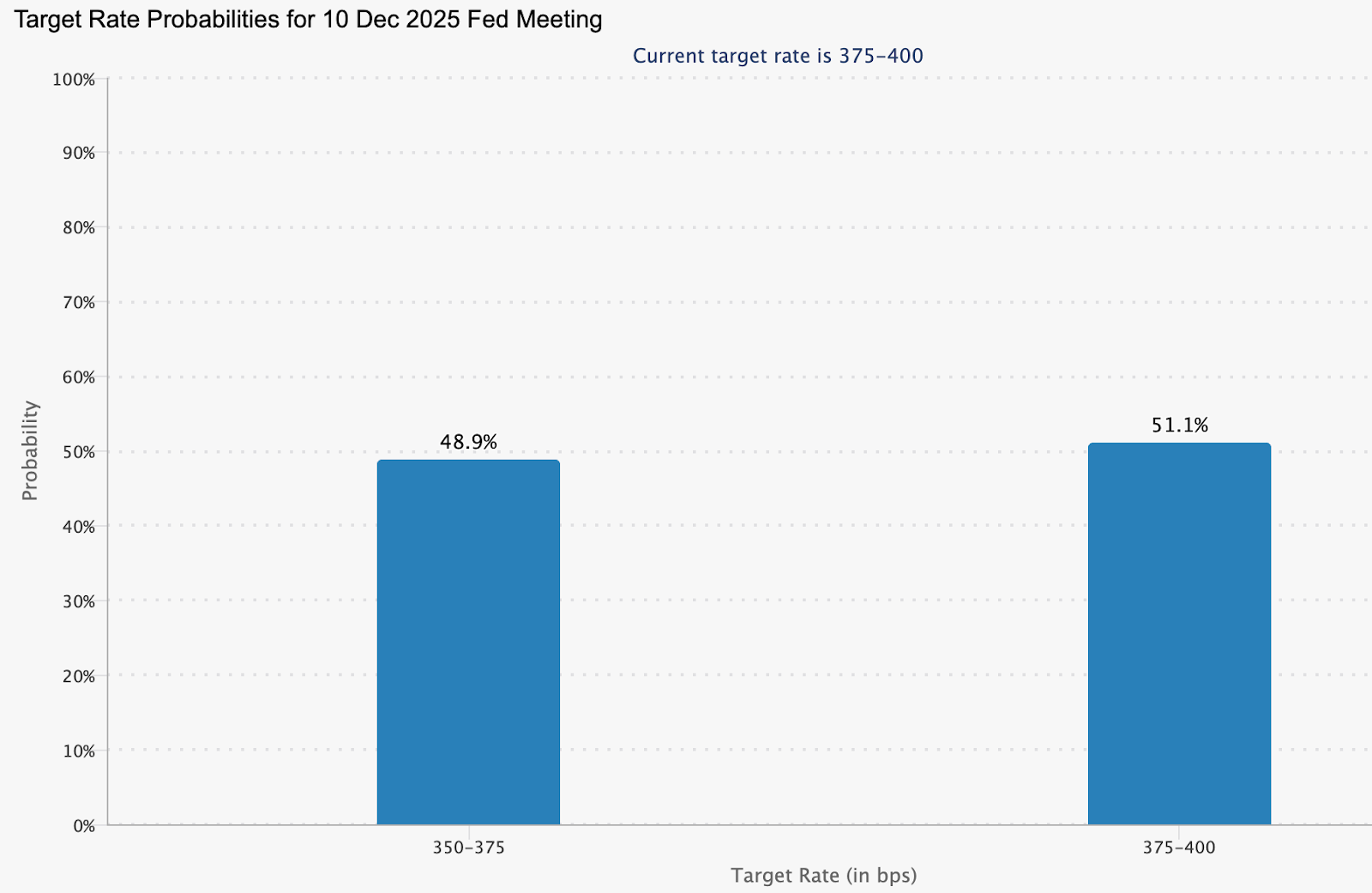

Now, as traders recalibrate expectations for a December rate cut - pricing in a 48.9% chance according to CME FedWatch - the metal has slipped back toward its midrange, around $4,050–$4,100, where short-term and long-term averages converge.

This retreat also mirrors a psychological reset. Markets are digesting the Fed’s cautious tone, with Vice Chair Philip Jefferson urging a “slow approach” to policy changes and regional presidents Bostic and Schmid signalling preference for steady rates. Those comments, paired with delayed macro data, have thinned speculative positions and allowed gold to breathe. In effect, the market is rediscovering balance - a hallmark of mean reversion after an overextended move.

Why it matters

Gold’s mean reversion tells a deeper story about trust and monetary fatigue. As Citadel’s Ken Griffin noted, the rising price of gold reflects “a loss of trust first in US Treasuries, then in G7 bond markets.” Investors are responding not to short-term volatility, but to structural concerns about government debt and the stability of fiat currency.

Analysts at Deutsche Bank maintain that the medium-term trend remains intact, projecting an average gold price of $4,000 per ounce next year. They highlight “elevated official demand” - a reference to sustained central-bank buying.

In October, China’s central bank added 0.9 tonnes to its reserves, marking its 12th straight month of accumulation. Ongoing purchases throughout 2025 have lifted China’s official gold reserves to 2,304.5 tonnes.

This underlines that while traders may be reverting to the mean, nations are not - they’re steadily diversifying away from the dollar.

Impact across markets

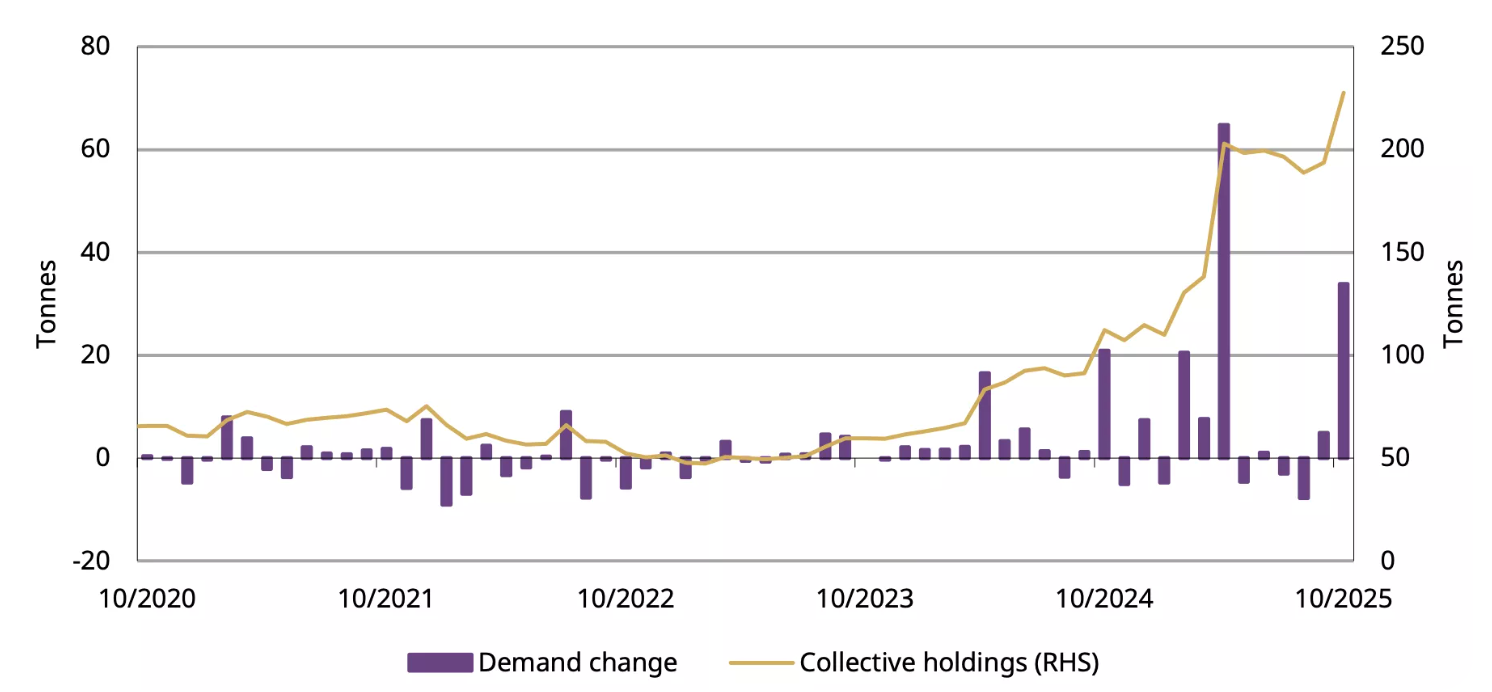

In China, investor appetite for gold remains vigorous even during the correction. ETF inflows jumped RMB 32 billion (US$4.5 billion) in October, pushing total holdings to a record 227 tonnes.

Physical demand, measured by withdrawals from the Shanghai Gold Exchange, rose 17 tonnes year-on-year to 124 tonnes, defying seasonal softness. The data suggests that investors see dips as opportunities, not red flags.

Globally, the story is similar. Soft US employment data and climbing jobless claims have tempered the dollar’s strength, nudging investors back into gold and silver.

Still, there’s awareness that a stronger NFP print or easing geopolitical risk could stall momentum. Even so, mean reversion isn’t a bearish event - it’s the market’s way of restoring order after a speculative sprint. And order, in uncertain times, is the most bullish foundation of all.

Expert outlook

Most analysts agree that gold’s medium-term trajectory remains higher, although near-term volatility will hinge on the US jobs data and the Fed’s stance in December. Independent trader Tai Wong says, “soft data is slightly boosting hopes for a December cut - helping gold and silver, which are trying to break a three-day losing streak.” That sentiment captures the current equilibrium: cautious optimism tempered by macro prudence.

If the NFP report underperforms, gold could swiftly retest $4,200, according to analysts. If it surprises to the upside, a dip toward $3,950 would complete a textbook mean reversion cycle before stabilising. Either way, the long-term bull case - driven by de-dollarisation, AI-driven labour disruption, and inflation inertia - remains intact. The question isn’t whether gold rises again, but when.

Gold technical analysis

At the time of writing, XAU/USD is trading near $4,088, rebounding from the lower Bollinger Band as buyers re-enter the market. The Bollinger Bands are beginning to widen after a period of contraction, suggesting that volatility may be returning.

The RSI is rising sharply from the midline, signalling improving bullish momentum. Key resistance levels are seen at $4,200 and $4,365, where profit-taking or further buying could occur if gold breaks higher. On the downside, a fall below $3,940 would likely trigger sell liquidations, exposing deeper support at $3,630.

Overall, gold appears to be in the early stages of a potential bullish continuation, with the technical setup hinting at renewed upside pressure if momentum sustains above the mid-Bollinger Band.

Key takeaway

Gold’s pullback to the $4,000 zone isn’t weakness - it’s rhythm. A reversion to the mean after a parabolic rise is how sustainable trends reset. Beneath short-term volatility, the drivers of this bull phase - de-dollarisation, central-bank accumulation, and macro distrust - remain fully in play. As the US jobs data and Fed decisions unfold, this pause could mark the quiet before gold’s next major rally.

Bitcoin crashes under $90K as ‘death cross’ bites

Spot prices printed as low as 89,420 dollars, the weakest level since February, only six weeks after setting a record near 126,250 dollars.

Bitcoin slipped below 90,000 dollars on Tuesday, extending a selloff that has erased its 2025 gains and pushed sentiment toward the bleak end of the spectrum. Spot prices printed as low as 89,420 dollars, the weakest level since February, only six weeks after setting a record near 126,250 dollars.

The breakdown coincided with a bearish technical crossover known as a death cross and increasingly hesitant fund flows into U.S. spot ETFs.

Together with macro anxiety around the rate path, these factors have tightened liquidity and amplified swings across majors. The next phase hinges on whether price can quickly reclaim lost support and whether ETF prints stabilise from recent choppiness.

What’s driving the slide

The proximate trigger is technical: Bitcoin fell back through reclaimed support near 93,700 dollars, lost its 200-day moving average, and then registered a death cross as the 50-day slipped beneath the 200-day.

On its own the signal is imperfect, but in weak liquidity regimes it often coincides with multi-week drawdowns as momentum traders de-risk.

Flows add fuel. U.S. spot ETF activity has turned choppy after heavy intake earlier in the year, with trackers showing sequences of outflows or flat prints that blunt marginal demand. When the incremental demand fades, price tends to chase lower liquidity pockets until new buyers emerge. Recent dashboards corroborate the stop-start nature of ETF demand. CoinDesk+1.

The Mt. Gox repayments - a trigger, not the cause

Adding fuel to the fire, over 10,600 BTC (worth roughly $953 million) were transferred from Mt. Gox wallets on 18 November 2025, marking the first such movement in eight months.

The long-running repayment saga, stemming from the 2014 collapse of the world’s then-largest exchange, has left creditors waiting over a decade for compensation.

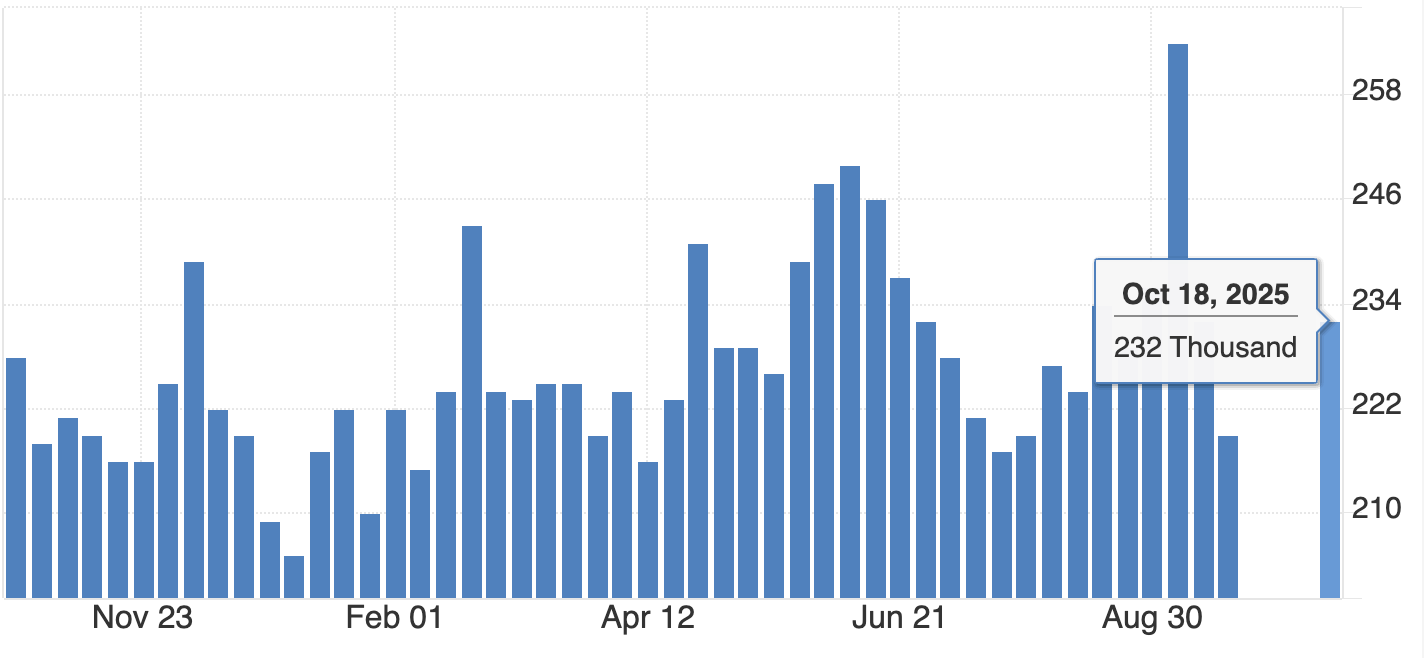

While some feared that repayments could unleash fresh supply, blockchain data shows these movements were administrative, not market sales. Still, perception alone was enough to unsettle sentiment, sparking liquidations and feeding the broader risk-off tone. Analysts now estimate over 230,000 trading accounts were liquidated within 24 hours, totalling more than $1 billion in forced sell orders.

Why this matters

Sentiment has swung hard into fear. CoinDesk flagged “extreme fear” conditions into the weekend and early week, aligning with widely followed gauges that punish downside volatility and negative breadth. In past cycles, similar extremes have marked acceleration phases within larger drawdowns or short-lived exhaustion points.

The macro overlay is not helping. Traders are parsing shifting expectations for U.S. rate cuts and inflation risks tied to policy developments, a mix that reduces risk appetite and tightens crypto liquidity. Reuters’ read-across captures the mood: a near 30 percent retreat from the October peak and growing caution among institutions.

Impact on markets and participants

Price leadership rotated back to bitcoin as traders sold altcoins to manage risk, a pattern visible when social attention and volumes consolidate in the benchmark asset during stress. Ether and other large caps have tracked lower alongside, while crypto-linked equities have generally underperformed on drawdown days, transmitting crypto volatility into listed proxies.

For allocators, ETF prints serve as the cleanest real-time barometer of spot demand. Multi-day flat or negative flows often coincide with fragility in order books and heavier slippage, which is why desks are laser-focused on whether the next sequence turns positive again. If it doesn’t, the unfilled liquidity pocket toward 86,000–88,000 dollars cited by traders continues to be a live risk.

Expert outlook

CoinDesk’s market desk notes that fear spikes of this magnitude have sometimes preceded relief rallies, particularly when realised-loss pressure begins to stabilise and ETF outflows slow. That requires confirmation: a swift reclaim of broken support and evidence of renewed net inflows. Until then, technicals and positioning argue for elevated two-way volatility.

Long-horizon investors continue to point at structural adoption and institutional participation as reasons to stay constructive on multi-year horizons. Dan Tapiero, whose 50T platform backs later-stage crypto companies, frames short-term turbulence as noise against a secular build-out, a view he has reiterated while forecasting a much larger digital-asset economy over the next decade.

Bitcoin price technical insight

Bitcoin (BTC/USD) continues its downward trajectory after forming a death cross, with the 50-day moving average (MA) crossing below the 200-day MA - a classic bearish signal suggesting extended downside pressure. The price is currently hovering near $91,000, after repeatedly failing to hold above key resistance levels at $106,685, $114,000, and $124,650, where prior rallies saw heavy profit-taking and FOMO-driven buying.

The Relative Strength Index (RSI) has dipped into oversold territory, indicating that selling momentum may be overextended and a short-term technical rebound could occur. However, as long as BTC remains below the 50-day MA, the broader trend remains bearish, with traders likely to view any bounce as a chance to sell into strength.

Key takeaway

Bitcoin’s slide below $90,000 reflects a convergence of technical breakdown, hesitant ETF demand, and a risk-off macro tone. The resulting fear spike is typical of late-stage selloffs, but it needs flow confirmation before calling a durable low. Watch for a quick reclaim of the $ 90,000 - $93,000 zone and a run of positive ETF prints to validate any rebound attempt. Until then, expect elevated volatility and tighter liquidity conditions.

Nie znaleźliśmy żadnych wyników pasujących do .

Wskazówki wyszukiwania:

- Sprawdź pisownię i spróbuj ponownie

- Użyj innego słowa kluczowego