Results for

.webp)

Market news – Week 3, March 2023

Bitcoin declined for a third successive week. After crossing the 25,000 USD mark in February, it was trading below 20,000 USD last week.

Bitcoin declined for a third successive week. After crossing the 25,000 USD mark in February, it was trading below 20,000 USD last week.

Forex

The EUR/USD pair gained marginally to close out the week at 1.0640 USD as the collapse of the Silicon Valley Bank overshadowed the expectation around the much-awaited inflation data (due on Tuesday, 14 March). This data will also inform the US Federal Reserve’s (Fed) policy rate decision. In his testimony before the Senate last week, Fed chair Jerome Powell struck a hawkish note, raising expectations of an increase in interest rates and longer into the future if inflation isn’t subdued.

Meanwhile, the non-farm payrolls (NFP), which were released on Friday, 10 March, again exceeded expectations after January’s bumper numbers and came in at 311,000 — analysts had predicted it to be around 205,000. The numbers made the case for a stronger performance for the dollar, but the potential boost in the dollar was kept in check by the unemployment rate, which went up to 3.8%.

The GBP/USD pair remained largely flat over the week and closed out at 1.2033 USD. Meanwhile, the USD/JPY pair failed to consolidate above the 137 USD mark and eventually ended the week at 135.80 USD following the release of the NFP data.

This week will see the release of the all-important Consumer Price Inflation (CPI) data, which is due on Tuesday, 14 March. Retail sales data will be released on Wednesday, 15 March, while the Initial Jobless Claims numbers will be out the following day on Thursday, 16 March.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

Gold prices remained bullish to close out the week at 1,867.87 USD. The surge in the price of the yellow metal has been fuelled by the falling US Treasury yields as the markets anticipate a 50 basis point hike in the March meeting of the Federal Open Market Committee (FOMC). Gold prices are inversely correlated to the US Treasury yield: when one goes down the other goes up.

The US Federal Reserve’s and the US Treasury’s intervention in the banking system to soften the impact of the failure of the Silicon Valley Bank further boosted the prices of the yellow metal.

Meanwhile, oil prices registered considerable gains over the week, rising 1% on Friday, 10 March, over the better-than-expected employment numbers. However, expectations of rate hikes by the Fed and other major economies have clouded growth prospects for the crude, and will likely have a stunting effect on oil prices if rate hikes decisions come to pass.

In a move that could likely temper any supply concerns, major oil-producing nations Saudi Arabia and Iran — both members of the Organization of the Petroleum Exporting Countries (OPEC) — resumed their diplomatic relations on the supply side after a series of undisclosed discussions in Beijing. The move comes close on the heels of the Russian decision to reduce its oil output by half a billion barrels a day in March.

Cryptocurrencies

Cryptocurrencies endured a torrid week on the back of crypto-focused Silvergate Bank’s announcement (on Thursday, 9 March) that it would voluntarily liquidate. It joins the lengthening list of cryptocurrency institutions to unravel in the aftermath of the November 2022 implosion of Futures Exchange (commonly known as FTX). Digital coins dipped further on Friday, 10 March, following the news of the collapse of the Silicon Valley Bank.

After 3 consecutive weeks of decline, Bitcoin — the world’s largest cryptocurrency — was trading at 21,996.80 USD, while Ether — the second-most widely traded digital token — was changing hands at 1,576.81 USD at the time of writing. The total value of digital assets was down below the 1 trillion USD mark and stood at 976.192 billion USD on Sunday, 12 March.

In a development that raises the spectre of regulations in the cryptocurrency industry, the New York attorney general labelled Ether a security, bracketing it with assets such as stocks and bonds. The attorney general’s reference was made on Thursday, 9 March, during her lawsuit against KuCoin — one of the biggest cryptocurrency platforms in the US. It triggered a fall in the price of Ether and it hit a 2-month low on Friday, 10 March.

Meanwhile, in the proceedings against FTX founder and CEO Sam Bankman-Fried, who is fighting to stay out of jail, the judge expressed his displeasure about the proposed terms of bail — which includes having an internet-less flip phone and a laptop with limited capability — for the 31-year-old. Bankman-Fried has been charged with stealing billions of dollars from FTX customers. His fraud trial is scheduled for October 2, 2023. While its founder awaits trial, the effects of the implosion of FTX are still being felt by the cryptocurrency industry 4 months after its bankruptcy.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on DTrader.

US stocks

Name of the indexFriday’s close*Net change*Net change (%)Dow Jones Industrial Avg (Wall Street 30)31,909.64-1,481.33-4.44Nasdaq (US Tech 100)11,830.28-460.53-3.75S&P 500 (US 500)3,681.59-184.05-4.55Source: Bloomberg

*Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

The US stock market took a huge tumble over the course of the last week as each of the 3 major indices — the Dow Jones, Nasdaq, and S&P 500 — fell over 3.75% each. The decline was a result of hawkish comments from the US Federal Reserve and potential cascading effects arising from the failure of the Silicon Valley Bank — the largest bank by deposits in Silicon Valley.

The S&P 500 was the biggest loser, going down by 4.55% — reaching its lowest point since early January. The Dow Jones lost 4.44%, while the Nasdaq declined 3.75% over the course of the week.

The US jobs report released on Friday, 10 March, helped alleviate concerns about significant rate increases. This came after Fed chair Jerome Powell cautioned that policymakers might raise rates beyond expectations if future data indicates high inflation, despite nearly a year of tightening measures.

Stocks this week will be tested by the result of the inflation report which is due on Tuesday, 14 March. A hotter-than-expected CPI report will raise fears of a big policy rate hike by the Fed. Furthermore, retail sales data — which measures the change in the sales volume at the retail level in the US — is due to be released a day later on Wednesday, 15 March.

Now that you’re up-to-date on how the financial markets performed last week, you can improve your strategy and trade CFDs on Deriv MT5.

Market news – Week 2, March 2023

After a poor showing the week before, the US stock indices rebounded last week, with the Nasdaq rising the highest.

After their poor showing in the week prior, the US stocks indices rebounded last week with the Nasdaq rising the highest.

Forex

The EUR/USD pair experienced gains following weakness in the US dollar to close out the week at 1.0631 USD. The pair saw wide fluctuations over the course of the week before the euro rallied on Friday, 3 March, to register some gains.

Meanwhile, the GBP/USD pair also registered weekly gains, closing the week at 1.2045 USD; while the USD/JPY pair was down to 135.84 USD.

There is a strong likelihood of volatility in the US dollar this week with the US Federal Reserve chair Jerome Powell set to give a 2-day testimony to the US Senate (scheduled for Tuesday and Wednesday, 7–8 March), and the release of the non-farm payrolls (NFP) data on Friday, 10 February. The latter has been billed as the most highly-anticipated economic report of the week since it comes on the back of the January data that showed over half a million new job additions in the US economy and revealed the lowest unemployment level since 1969.

Among other reports, the US crude oil inventories and the jobless claims data are also due this week. While the former will be released on Wednesday, 8 March, the latter will be out a day later on Thursday, 9 March.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

Gold prices saw a bullish revival last week after their recent bear run, rising on the back of the weakness in the US dollar — since gold is priced in US dollars, a depreciated currency makes it more affordable for international buyers — and strong economic data in China. The yellow metal closed out the week at 1,856.36 USD.

The risk of a likely increase in the US lending rates kept the precious metal prices from rising further. However, China is a major consumer of gold and its upbeat economic performance could see the prices of the yellow metal rise further.

Similarly, oil prices marked a recovery from their recent downturn and gained nearly 1 USD per barrel on Friday, 3 March, to close the week higher. The surge in crude prices was driven by optimism around demand from China, the world’s top oil importer. China’s services sector in February grew at its fastest pace in 6 months, while its manufacturing sector registered a stunning growth not seen since April 2012.

Meanwhile, following a Friday, 3 March, Wall Street Journal (WSJ) report about the United Arab Emirates (UAE) considering leaving the Organization of the Petroleum Exporting Countries (OPEC) and increasing oil production, prices fell more than 2 USD per barrier. However, the prices recovered after a Reuters report refuted the WSJ story. The UAE is OPEC's third-largest oil exporter after Saudi Arabia and Iraq.

Cryptocurrencies

Last week, the cryptocurrency industry was left reeling from the fallout of the troubles at cryptocurrency-friendly US bank Silvergate Capital as prices of digital tokens fell.

Following the November 2022 implosion at Futures Exchange (commonly known as FTX), which had been a large client of the bank, Silvergate saw nearly 70% of its digital-asset-related deposits leave its coffers in the fourth quarter of 2022. The bank, in a report to the Securities and Exchange Commission (SEC), stated that it would need to delay the filing of its annual report as it analysed the impact of several events on its business.

Bitcoin’s price on Friday, 3 March, marked a 2-week low for the cryptocurrency as investors digested the fallout from Silvergate Capital and evaluated its ability to stay in business. The digital token was trading at 22,436 USD at the time of writing, while Ethereum — the world’s second-largest cryptocurrency — was trading at 1,565 USD. The global cryptocurrency market capitalisation stood at 1.03 trillion USD on Sunday, 5 March.

Meanwhile, in a development that will likely boost the cryptocurrency space, payments firm Visa has said that it has no plans to slow down its cryptocurrency plans despite reports hinting otherwise amid a brutal bear market. Visa also filed new trademark applications in October last year, which hinted at its potential plans for a cryptocurrency wallet and a metaverse product.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on DTrader.

US stocks

*Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

The 3 major US stock indices rebounded last week after their downturn the week before and registered substantial gains. The Nasdaq was the biggest gainer with a 2.58% rise. The S&P 500 was up 1.90%, while the Dow Jones registered a 1.74% upswing for the week. For the S&P 500, the latest result snapped a string of three weekly losses in a row.

The stocks were boosted by the positive developments in the US economy in February. The Institute for Supply Management (ISM) survey — which tracks economic activity across the US services sector — on Friday, 3 March, described companies as “mostly positive about business conditions”, and showed its highest reading since June 2022. Similar services sector expansion was reported on Friday in the Eurozone and China.

Out of the 11 equity sectors, only information technology managed to report a positive outcome in February. Meanwhile, the S&P 500, which registered a 6.2% rise in January, was down a staggering 17.2% from its record high on January 3, 2022.

As the fourth-quarter earnings season concluded, it revealed an average 4.9% decline in earnings in the S&P 500 companies. This marks the first quarterly decline since the third quarter of 2020. The energy sector was the strongest performer, with earnings growth of 57.0% in the latest quarter.

Now that you’re up-to-date on how the financial markets performed last week, you can improve your strategy and trade CFDs on Deriv MT5.

.webp)

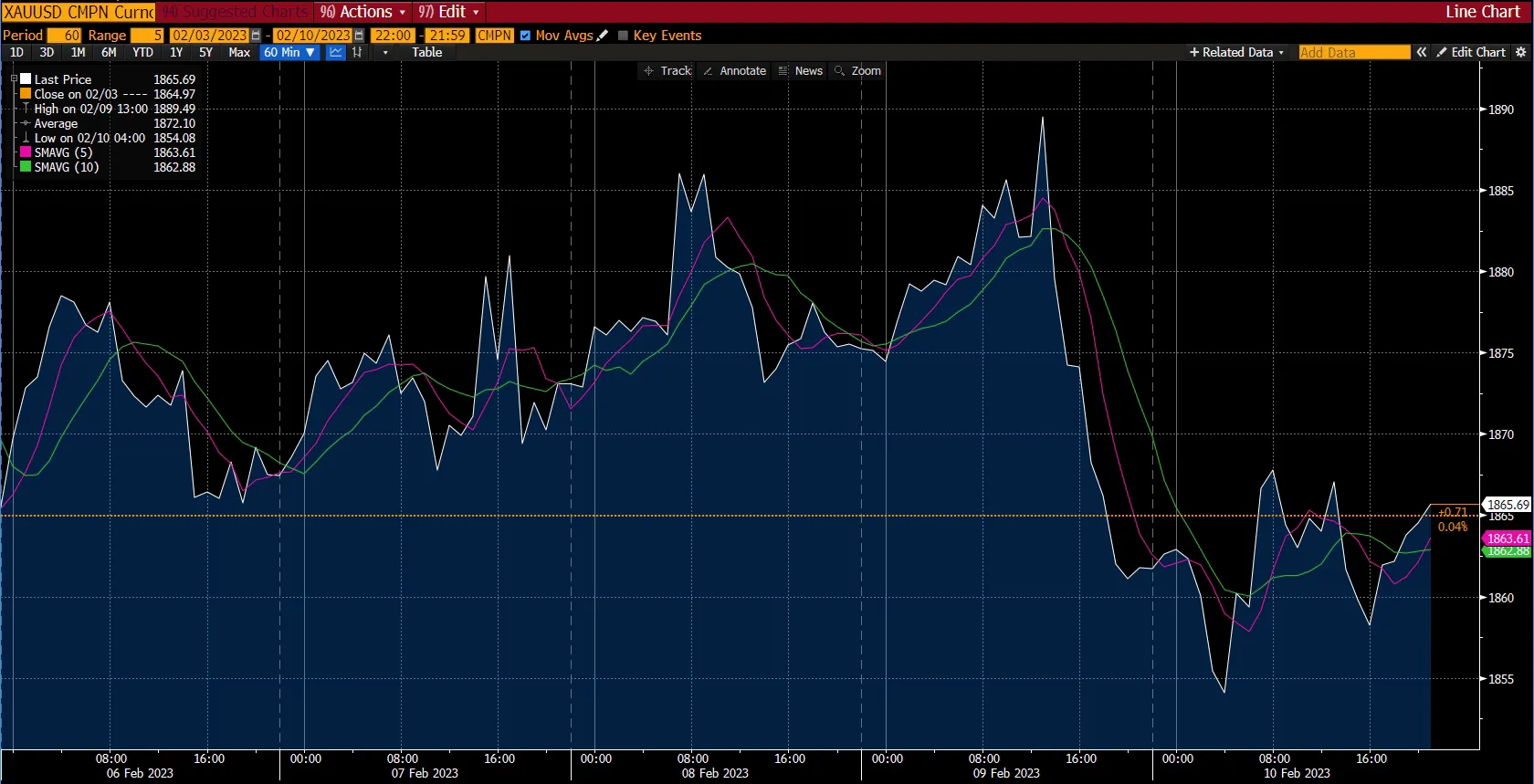

Market news – Week 3, February 2023

Regulatory action against cryptocurrency exchange platform Kraken had a cascading effect on digital assets as their prices stumbled.

Regulatory action against cryptocurrency exchange platform Kraken had a cascading effect on digital assets as their prices stumbled.

Forex

Source: Bloomberg.

The EUR/USD pair fell for a second successive week as the euro ended the week at 1.0677 USD. The US dollar rose the highest on Monday, riding on the resounding non-farm payrolls (NFP) data and the 25 basis points rate hike by the US Federal Reserve (Fed) announced last week.

Fed chief Jerome Powell, in his remarks on Tuesday, 7 February, reiterated the need for further policy rate hikes this year. However, he also acknowledged an easing in inflationary pressure, raising investors’ hope for a policy pivot in the future.

The strength in the USD kept the GBP/USD pair to a marginal gain over the week, and the pair closed last week at 1.2058 USD. The British pound sterling wasn’t helped by the gross domestic product (GDP) data released in the United Kingdom on Friday, 10 February, that showed a stagnant economy in the final three months of 2022.

On the events front, the Customer Price Index (CPI) data in the US is scheduled to be released on Tuesday, 14 February. Crude oil inventories and retail sales data are set for a Thursday, February 15, release. Meanwhile, Producer Price Index (PPI) data — which calculates the variation in the cost of goods manufactured and sold — will be released a day later on Friday, February 16.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

Source: Bloomberg.

Gold prices maintained their level from the week prior to close last week at 1,865.69 USD. The precious metal rose to nearly 1,890 USD on Thursday, 9 February, before it lost all of its gains under bearish pressure.

A slew of data releases — especially the inflation data — slated for this week will have a bearing on the price movements of the precious metal. The US Fed’s rate hike decisions are heavily dependent on the direction of inflation in the country.

After successive weeks of slumps, US crude oil prices rose almost 9% for the week and reached nearly 80 USD a barrel on Friday, 10 February. Among the reasons for the rise was Russia’s Friday announcement of a production cut in March by half a million barrels per day, in response to the sanctions imposed on the country in the wake of the war in Ukraine.

Cryptocurrencies

Source: Bloomberg.

Action taken by the Securities and Exchange Commission (SEC) against cryptocurrency exchange platform Kraken last week had an immediate impact on the industry as major digital tokens traded in the red. The global cryptocurrency market capitalisation stood at 997 billion USD on Sunday, 12 February.

The SEC reached a 30 million USD settlement with Kraken that will force it to wind up a programme offering investment returns to its American users who committed digital assets to the company. In a complaint on Thursday, 9 February, the SEC alleged that the practice, known as “staking”, reflected an unregistered offer and sale of securities. According to the regulatory body, Kraken failed to adequately disclose the risks of participating in the programme, which had advertised annual yields as high as 21%.

Meanwhile, Bitcoin, the world’s largest digital currency by market capitalisation, was trading at 21,789.80 USD at the time of writing. The second-most traded cryptocurrency, Ethereum, also lost its key support level at 1,600 USD and was trading at 1,515.34 USD.

In a significant development, banks in the European Union are required to place the maximum possible risk weight on cryptocurrency assets under a draft law published by the European Parliament on Friday, 10 February. Under the law, banks would have to disclose their direct and indirect exposure to cryptocurrencies. Meanwhile, the European Commission is also preparing more fine-grained rules for the sector. Such regulatory action in the cryptocurrency market will likely contain the volatility often seen in the space.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on DTrader.

US stocks

*Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

After gaining 6.2% in January, the S&P 500 fell 1.11% last week, making it the index’s biggest weekly drop since December 2022. The Nasdaq, which had risen for five consecutive weeks, was down 2.13% last week. Meanwhile, the Dow Jones slipped a marginal 0.17%.

Stocks that took a beating in 2022 have been surging this year so far. However, analysts predict that the trend won’t last long, with the looming Federal Reserve rate hike uncertainty as it attempts to keep inflation in check. Netflix, which fell 51% last year is up 18% this year, while Meta Platforms stock has gained 45% in 2023 after a steep 64% fall last year.

As the fourth-quarter earning season is heading to a close, analysts have subdued forecasts for the first-quarter — which companies begin reporting in April. It follows the general trade for the first month of a quarter, however, the average reduction is more than what has been seen over the last 5 years.

The Consumer Price Index (CPI) report, which is scheduled to be released on Tuesday, 14 February, will show whether inflation extended into January. Investors will also be keen on the retail sales data due to be released on Wednesday, 15 February.

Now that you’re up-to-date on how the financial markets performed last week, you can improve your strategy and trade CFDs on Deriv MT5.

Market news – Week 4, February 2023

Oil prices fell for the week as traders worry about the interest rate decision by the US Federal Reserve amid inflation fears. Read more in our report.

Oil prices were down for the week and major cryptocurrencies finally saw a rally after two weeks of slow movements.

Forex

Source: Bloomberg.

The EUR/USD pair ended the week with minor gains with the euro at 1.0694 USD by the week’s close. There were many factors that kept the dollar in check — geopolitical tensions between the US and China as the latter’s intention to supply Russia with weapons for the ongoing war in Ukraine, hawkish comments from the European Central Bank (ECB), similar remarks from US Federal Reserve officials, and a smaller-than-expected decline in inflation.

Meanwhile, the GBP/USD pair had a relatively flat performance, with the GBP ending the week marginally low at 1.2043 USD. Further, at a rate of 134.13 per USD, the Japanese yen experienced a 0.13% decline over the week against the greenback.

This week will see 4 trading days as the US financial markets will be closed on Monday, 20 February, on account of the Presidents’ Day holiday. The remainder of the week is packed with scheduled high-impact economic data releases.

The US Federal Open Market Committee (FOMC) meeting minutes will be released on Wednesday, 22 February. The fourth quarter gross domestic product (GDP) and the jobless claims data in the US will be released on Thursday, 23 February, while the Personal Consumption Expenditure (PCE) — which measures the fluctuations in the cost of commodities and amenities acquired by individuals — will be released a day later on Friday, 24 February.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

Source: Bloomberg.

Gold prices continued to be sluggish, closing the week at 1,842.57 USD. The instability in the yellow metal’s prices has largely been influenced by US-related factors, notably the Federal Reserve's aggressive stance in response to robust economic data such as non-farm payrolls, inflation, and retail sales.

There’s a large amount of important economic data due for release this week, especially with the PCE data — the Fed’s preferred inflation barometer — due on Thursday, 23 February. If the PCE numbers follow in the footsteps of the inflation data from last week, it could give a boost to the dollar and expose gold to further bearish pressure.

Meanwhile, oil prices ended the week lower as traders worried about the US Fed’s interest rate decision after two officials on Thursday, 16 February, warned of additional rate hikes in a bid to curb inflation. Signs of ample supply — increase in crude inventories in the US and expectations of Russian suppliers maintaining their current output — also played a role in keeping prices in check last week. Oil settled at 2 USD a barrel on Friday, 17 February.

Cryptocurrencies

Source: Bloomberg.

After a subdued fortnight, major cryptocurrencies saw a rally last week that pushed the total market capitalisation of digital assets up to 1.17 trillion USD on Sunday, 19 February.

Bitcoin, the world’s most popular cryptocurrency, climbed 14% for the week and crossed the 24,000 USD mark for the first time since August 2022. It peaked as high as 24,650 USD on Saturday, February 18. Bitcoin has come a long way since last November when it sank below 16,000 USD. Ethereum, the world’s second-largest cryptocurrency, nearly touched the 1,700 USD mark, reaching a high of 1,695.82 USD on Friday, 17 February.

Meanwhile, in a development that could see regulation in the decentralised cryptocurrency space, the Group of 20s — or G20 — Financial Stability Board (FSB) on Thursday, 16 February, said that it would take steps to tackle vulnerabilities in decentralised finance (DeFi) following the November 2022 collapse of Future Exchange — the cryptocurrency exchange platform also known as FTX.

Two weeks after China distributed millions of dollars worth of its Central Bank Digital Currency (CBDC) across the country, Japan announced on Friday, 17 February, plans to test run its own CBDC pilot programme with digital yen, beginning April 2023. Central banks across the world are at various stages of their own CBDC development as they seek to enter the electronic currency space with digital versions of their legal tenders.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on DTrader.

US stocks

Name of the indexFriday’s close*Net change*Net change (%)Dow Jones Industrial Avg (Wall Street 30)33,826.69-42.58-0.13Nasdaq (US Tech 100)12,358.1853.260.43S&P 500 (US 500)4,079.09-11.37-0.28Source: Bloomberg.

*Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

The major US stock indices continued their moderate performance last week, starting the week strongly before their gains faded out by the end of it. The S&P 500 slipped 0.28%, the Dow Jones was down 0.13%, while the Nasdaq gained a measly 0.43%.

There was good news on the data front as January retail sales in the United States increased by 3% on a seasonally adjusted basis, marking the largest monthly rise in almost two years.

Meanwhile, the fourth-quarter earnings continued their below par performance thus far, with nearly four-fifths of the S&P 500 firms having announced their results. Based on the numbers released until now and forecasts for the remainder of the earnings season, analysts expect a 4.7% decline compared to the same quarter last year.

Investor focus will be on the release of the minutes from the US Federal Reserve’s meeting when it announced a 25 basis point rate hike. It will be released on Wednesday, 22 February. Meanwhile, a number of big retailers are due to announce their earnings in the coming days with the results of Walmart and Home Depot due this week.

Now that you’re up-to-date on how the financial markets performed last week, you can improve your strategy and trade CFDs on Deriv MT5.

Disclaimer:

Options trading and the Deriv X platform are unavailable for clients residing in the EU.

.webp)

Market news – Week 1, March 2023

Favourable data releases in the United States propelled the US dollar higher, while major cryptocurrencies saw their recent rise stalled.

Favourable data releases in the United States propelled the US dollar higher, while major cryptocurrencies saw their recent rise stalled.

Forex

The EUR/USD pair was down for the week, closing the week at 1.0546 USD after recent favourable data releases that boosted the US dollar. There was a surprise rebound in the Personal Consumption Expenditure (PCE) Price Index and an upsurge in the households’ spending in January, which raised expectations that the United States Federal Reserve will continue its rate-hiking spree until the summer as it attempts to keep inflation in check. The minutes from the Fed’s meeting — when it announced a 25 basis point hike in the lending rates — showed that Fed officials believe that rate hikes will continue to be a necessity, unless they see more evidence of ease in inflation.

Meanwhile, its fourth quarter gross domestic product (GDP) data showed that the pace of the US economy was slower than anticipated. The US GDP grew at an annualised rate of 2.7% in the latest quarter — 0.2% lower than the estimated 2.9%. Slower rate of consumer spending is one of the reasons for the downward revision to the GDP data.

The GBP/USD plummeted following the release of the economic data in the US and hit a low of 1.1927 USD, closing the week barely above the monthly low. The USD/JPY reached its highest level since December 2022 and reached a peak of 136.46 USD on Friday, 24 February.

A number of important data releases are lined up this week as well. Conference Board (CB) Consumer Confidence data will be released on Tuesday, February 28 and ISM Manufacturing Purchasing Managers Index (PMI) report is scheduled for a Wednesday, March 1 release. Initial Jobless Claims data is due on Thursday, March 2, while ISM Non-Manufacturing Purchasing Managers Index (PMI) numbers will be out a day later on Friday, 3 March.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

The rally in the US dollar after favourable PCE data spelled doom for gold prices as they tumbled down to 1,814.19 USD at the close of the week. A number of data releases due for next week will further decide the trajectory of the yellow metal.

In the week that marked a year since the start of the war in Ukraine, oil prices remained largely flat, as the possibility of reduced Russian exports provided some support, while mounting inventories in the United States and apprehensions regarding the global economic activity exerted downward pressure on the crude prices.

The US Crude Oil Inventories data — which tracks the weekly fluctuations in the quantity of commercial crude oil barrels stored by US companies — will be released on Thursday, 2 March.

Cryptocurrencies

Following its spectacular 14% rise in the week prior, Bitcoin started last week strongly and edged close to the 25,000 USD mark, but couldn’t sustain its momentum and lost most of its gains by the end of the week. This happened after top regulators in the US warned banks to guard themselves against liquidity risks posed by cryptocurrency-related clients.

The Federal Reserve, Federal Deposit Insurance Corporation, and Office of the Comptroller of the Currency issued a joint statement on Thursday, 23 February, urging banks to monitor funds placed by crypto-asset-related entities.

Bitcoin, the world’s most popular currency, was trading at 23,398.50 USD at the time of writing, while Ethereum — the second-most traded digital token globally — was trading at 1,639.67 USD. The global cryptocurrency market cap stood at 1.12 trillion USD on Sunday, 26 February.

Meanwhile, the International Monetary Fund (IMF) in a paper titled, ”Elements of Effective Policies for Crypto Assets”, published on Thursday, 23 February, issued a 9-point guidance to countries on ways to deal with cryptocurrency assets, with their first point urging nations against recognising cryptocurrencies as legal tender. Two days later, on Saturday, 25 February, India’s push for regulation of the digital assets industry at a meeting of finance chiefs from the Group of 20 (G20) meeting was endorsed by the IMF and the US.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on DTrader.

US stocks

*Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

The 3 major stock indexes in the United States suffered their worst week of 2023 so far. The S&P 500 was down 2.67%, the Dow Jones 2.98%, and the Nasdaq 3.14%. The bigger-than-expected rise in the PCE index and the release of the US Federal Reserve minutes raised fears of monetary policy tightening by the US Federal Reserve, which weighed on the stocks.

It has been a difficult February for the indexes after spectacular gains in January. The S&P 500, for instance, gained 6.2% in January, but has just endured its third successive week in the red. A slew of data releases have amplified worries of the Fed tightening interest rates after a 25 basis point hike in early February as it attempts to battle inflation. Analysts believe that the markets have not sufficiently accounted for the possibility of a recession — which remains a looming threat.

Among the stocks that slid the most, Tesla, Amazon, and Nvidia ended the week in red.

The scheduled release of important data points this week will provide a cue to the direction the markets will take in the near future.

Now that you’re up-to-date on how the financial markets performed last week, you can improve your strategy and trade CFDs on Deriv MT5.

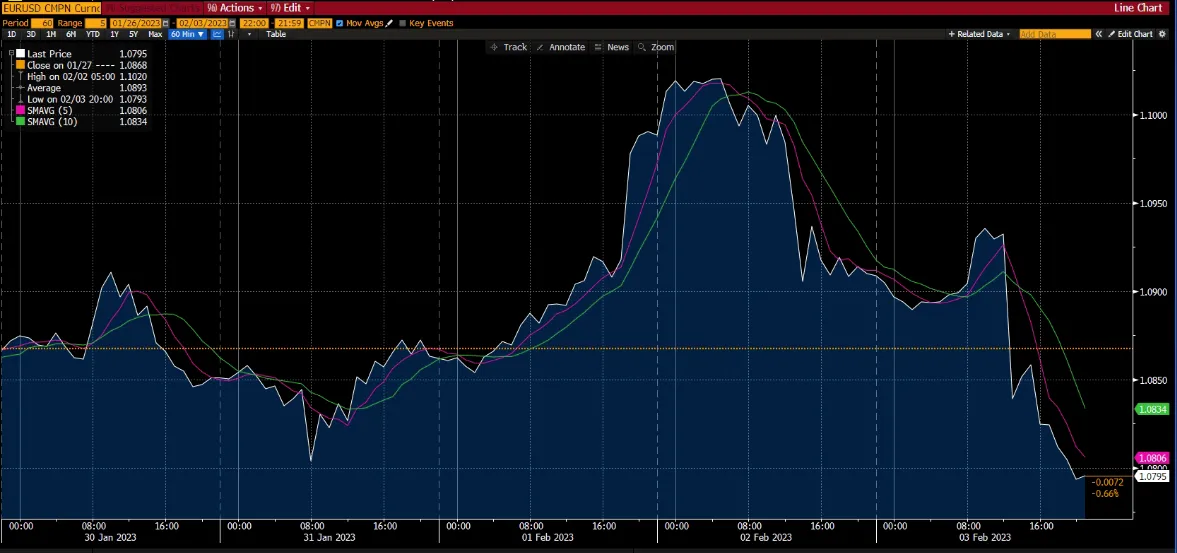

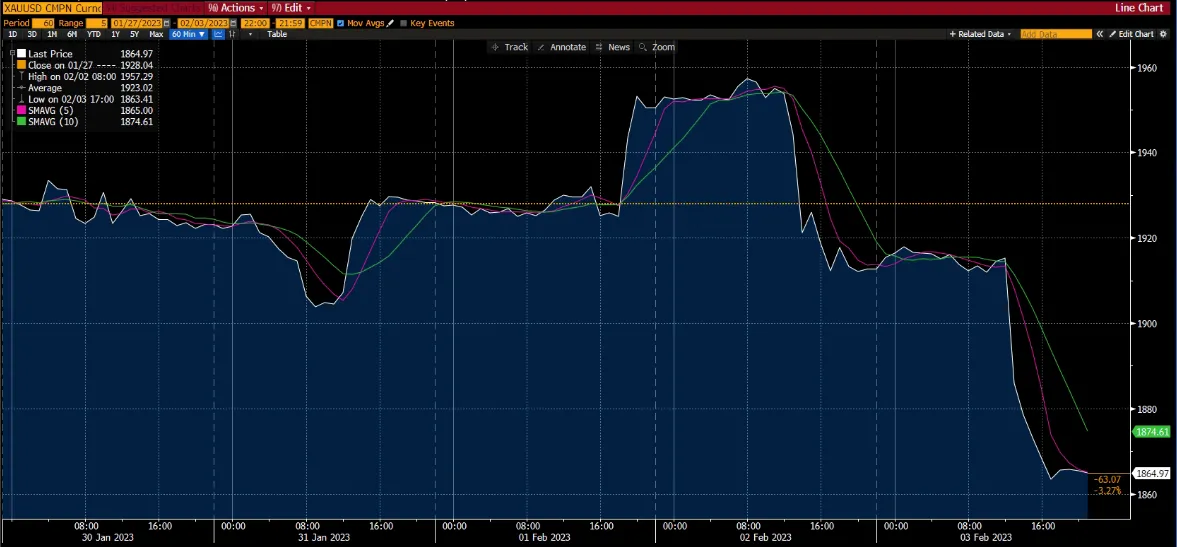

Market news – Week 2, February 2023

The S&P 500 registered a cumulative 6.2% rise in January, signaling the likelihood of a strong performance in the US stock market this year.

The S&P 500 registered a cumulative 6.2% rise in January, signaling the likelihood of a strong performance in the US stock market this year.

Forex

The US dollar followed up its rise from the week prior to register a strong performance last week, with the EUR/USD pair closing at 1.0795 USD. The currency was propped up by the US Federal Reserve’s (Fed) marginal rate hike, its acknowledgment of easing inflation, and a sharp increase in jobs in the US.

The Fed announced a 25 basis point interest rate hike on Wednesday, 1 February. The small increase was expected and is half the hike announced at the last Fed meeting in November 2022. The upbeat non-farm payrolls (NFP) data — which revealed an addition of 517,000 new jobs in January — was much higher than analysts’ expectations. The unemployment rate in the US is now down to 3.4%, a level not seen since 1969.

The rising dollar ensured that the GBP/USD pair ended the week at 1.2055 USD. After a steady start to the week, the pair started to decline on Thursday, 2 February, the day the Bank of England (BoE) and the European Central Bank (ECB) both raised their policy rates by half a basis point.

On the events front, Fed chief Jerome Powell is scheduled to speak on Tuesday, 7 February. The Initial Jobless Claims report — which measures the number of individuals who filed for unemployment benefits — will be released on Thursday, 9 February. Meanwhile, the fourth-quarter gross domestic product (GDP) data in the United Kingdom will be released on Friday, 10 February.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

Gold prices declined sharply, ending the week at 1,865 USD an ounce. The strong employment numbers in the United States — which has raised inflation fears — contributed to the weakness in the yellow metal as did the policy rate hikes by the BoE and the ECB last week. Gold prices were also impacted by the heightened geopolitical tensions between the US and China amid the sighting and subsequent downing of an alleged Chinese spy balloon off the California coast on Saturday, 4 February.

Fed chief Powell’s remarks on Tuesday, 7 February, will be closely watched as a hawkish stance from the central banker will likely push gold prices further down.

Like gold, oil prices slumped too. The price of US crude oil was impacted by an increase in supply in the United States, and fell nearly 8% for the week to around 73 USD per barrel, the lowest it has reached in nearly a month.

Meanwhile, on Saturday, 5 February, Saudi Arabia's energy minister Prince Abdulaziz bin Salman Al-Saud warned that sanctions and underinvestment in the energy sector could result in shortage of oil supplies in the future. Saudi Arabia is the world’s largest supplier of crude. Russia has been heavily sanctioned by the West due to the ongoing war in Ukraine.

Cryptocurrencies

Cryptocurrencies traded mostly in the green last week, after Fed chair Powell acknowledged that inflation has started to ease in remarks he made following a quarter-point rate hike by the US central bank.

The rate hike and Powell’s comments appeared to have gone down well in the cryptocurrencies markets, which had been trading sideways in the lead-up to the speech. In the hours after Powell’s remarks, market capitalisation increased by nearly 4%. The global cryptocurrency market stood at 1.06 trillion USD on Sunday, 5 February.

After an impressive rally in January, Bitcoin’s rise has been subdued in February so far. The world’s largest cryptocurrency was trading at 22,936.30 USD at the time of writing, after reaching a high of 23,705.10 USD during the week. Ethereum, the world’s second-most popular cryptocurrency, was trading at 1,629.37 USD.

Meanwhile, in a significant development in the centralised digital currency space, the Chinese government distributed millions of dollars worth of its Central Bank Digital Currency (CBDC) across the country over the Lunar New Year period. Unlike the decentralised cryptocurrencies, the CBDCs are issued and controlled by the countries’ central banks.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on DTrader.

US stocks

*Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

The S&P 500 index was on the up for a second successive week and registered a 1.62% rise. Nasdaq registered its fifth straight week of growth to end the last week up by 3.34%. Meanwhile, the Dow Jones was down 0.15%.

With last week’s results, the S&P 500 rose 6.2% in January on the back of hopes that the Federal Reserve will be able to keep inflation in check without hampering the economy. This marks the first instance in 4 years that the index has ended a January in green. The S&P 500’s January performance bodes well for the US stocks as the index has seen a positive February – December period 83% of the time it has seen a gain in the first month of the year.

With half of the earnings season gone, about 70% of the companies in the S&P 500 index have exceeded analysts’ expectations, a figure lower than the five-year average of 77%.

However, some investors are cautious, believing that the stocks have gotten ahead of themselves. Furthermore, the blowout employment data has renewed inflation concerns and bets of a more hawkish US Federal Reserve in the near future.

Now that you’re up-to-date on how the financial markets performed last week, you can improve your strategy and trade CFDs on Deriv MT5.

Market news – Week 4, January 2023

Gold prices continued their upward surge as uncertainty in the markets — amid weak economic reports in the US and recession fears — drove investors to seek refuge in the yellow metal.

Gold prices continued their upward surge as uncertainty in the markets — amid weak economic reports in the US and recession fears — drove investors to seek refuge in the yellow metal.

Forex

The euro continued to benefit from the weak US dollar as the EUR/USD pair finished last week at 1.0860 USD, extending its winning streak against the dollar. It was a week of volatility for the pair, but the euro gained despite wide fluctuations.

The European Central Bank’s (ECB) near-term policy outlook has been the driver for the volatility in the pair. At the World Economic Forum in Davos on Thursday, 19 January, ECB president Christine Lagarde said that the central bank will continue raising interest rates in its bid to drive down inflation to 2%.

Meanwhile, the US dollar registered its biggest daily gain against the Japanese yen in nearly 2 weeks as the Bank of Japan (BoJ) chief reiterated his "extremely accommodative" monetary policy stance in a bid to achieve its inflation target.

On the events front, a raft of market-moving releases are lined up. The fourth-quarter gross domestic product (GDP) data will be released in the US on Thursday, 26 January, while the core Personal Consumption Expenditure (PCE) data — which measures inflation — will be released on Friday, 27 January. If either release misses expectations, it will raise the volatility in the EUR/USD pair.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

Gold prices continued their surge for a fifth straight week to end the last week at 1,926.03 USD an ounce, rising on hopes of a slower rate hike by the US Federal Reserve (Fed). The precious metal had broken the 1,900 USD barrier for the first time in 7 months in the week prior.

Weak US economic reports and hawkish remarks by the US Fed officials, which fuelled recession fears, have contributed to the gains in the yellow metal — gold prices tend to gain when investors seek refuge from the uncertainty in the markets.

Elsewhere, oil prices gained for a second consecutive week on the back of positive economic signs from China, boosting prospects of increased fuel demand by the world’s largest oil importer. The International Energy Agency (IEA) on Wednesday, 18 January, said that China’s lifting of Covid-19 curbs should lead to record high global demand for oil.

The price cap on Russian oil — which was enforced in the aftermath of the ongoing war in Ukraine — has dented global supplies and is another reason for the boost in crude prices.

Cryptocurrencies

Over the last week, cryptocurrencies faced yet another surge, with most tokens making significant gains. With their latest run, the global cryptocurrency market capitalisation went past the 1 trillion USD mark and stood at 1.05 trillion USD on Sunday, 22 January.

Ahead of the Lunar New Year holiday celebrations in Asia, Bitcoin rallied to its highest levels since August 2022, surging at the start of the weekend for a second straight week. The price of the world’s largest cryptocurrency briefly crossed 23,000 USD during the week.

The latest jump in its price brings Bitcoin up almost 39% since the start of January, although it is still nearly 67% off from its all-time high of 68,789.63 USD (reached in November 2021). The token is currently trading at 22,714.80 USD at the time of writing. Meanwhile, Ethereum — the second-largest digital currency by market capitalisation — was trading at 1,629.30 USD on Sunday, 22 January.

But it's not all good news in the digital assets industry. US-based cryptocurrency investment firm Genesis has become the latest casualty of the crisis unleashed in the industry following the November 2022 implosion at Futures Exchange — commonly known as FTX. Genesis has filed for bankruptcy protection, listing aggregate liabilities ranging from 1.2 billion USD to 11 billion USD. The development followed the US Securities and Exchange Commission’s (SEC) announcement on Thursday, January 12, that it had charged Genesis and crypto exchange Gemini with selling unregistered securities through their interest-bearing product.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on Deriv Trader.

US stock markets

*Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

After gaining for successive weeks, US stocks experienced their first downturn of 2023. Mixed fourth-quarter earnings results, announcement of mass layoffs at major technology firms, and the prospects of an impending recession all contributed to the reverse in the markets last week.

The Dow Jones had a larger decline of 2.70%, compared to the S&P 500's 0.66% drop. However, the Nasdaq increased by 0.67%.

Companies accounting for over 50% of the S&P 500's market value are scheduled to announce their earnings over the next two weeks, including Microsoft (Tuesday, 24 January), Tesla (Wednesday, 25 January), and Intel (Thursday, 26 January). Next week, Apple and Alphabet (Google's parent company) will release their numbers. Both firms are among the largest in the world by market value.

Their results will have significant market impact on the market movements as investors will be eager to see if these tech giants — renowned for their spectacular growth over the last few years — will be able to maintain their performance in the aftermath of significant downsizing that some of them have announced over the last few weeks. Microsoft announced 10,000 layoffs on Wednesday, 18 January, while Alphabet on Friday, 20 January, revealed plans to cut 12,000 jobs. Amazon and Facebook-parent Meta have also announced major redundancies in recent weeks.

Now that you’re up-to-date on how the financial markets performed last week, you can improve your strategy and trade CFDs on Deriv MT5.

.webp)

Market news – Week 3, January 2023

Bitcoin led the charge — crossing the 20,000 USD mark —- as cryptocurrency prices surged over the last week, raising expectations of another bull run.

Bitcoin led the charge — crossing the 20,000 USD mark —- as cryptocurrency prices surged over the last week, raising expectations of another bull run.

Forex

The EUR/USD pair achieved its highest level since May 31, 2022 as the US dollar continued its slide. The euro climbed up to 1.0780 USD on Thursday, 12 January, before slowing down the next day as the US dollar recovered on the back of the Consumer Price Index (CPI) data. Inflation slowed down in December 2022, raising expectations of a 25 basis points hike by the US Federal Reserve in February.

The British pound mounted a surge of its own as the GBP/USD pair reached a 4-week high at 1.2240 USD. The GBP traded just above 1.2200 USD on Friday, 13 January. following the better-than-expected gross domestic data (GDP) in the United Kingdom.

Meanwhile, the Japanese yen continued its bull run on the back of softening inflation in the US and expectations of an aggressive stance by the Bank of Japan.

The events calendar this week will see the release of the Initial Jobless Claims data (which measures the number of individuals who filed for unemployment insurance over the past week) and the Producer Price Index (PPI) data (which measures the change in the price of goods sold by manufacturers) on Wednesday, 18 January.

Level up your trading strategy with the latest market news and trade CFDs on your Deriv X account.

Commodities

Gold prices finished their fourth straight week in positive territory after climbing over the 1,900 USD mark on Thursday, 12 January, for the first time in 7 months. The upward price movement was driven by the selling pressure on the US dollar following the release of the core inflation data in the United States.

China is scheduled to release its fourth quarter GDP data on Tuesday, 17 January. Growth in GDP will help push gold prices higher as China is the largest consumer of gold in the world. On the other hand, the effects of a negative GDP print — which is likely owing to Covid-19 disruptions in China — is expected to be short-lived.

Oil prices ended the last week on their biggest weekly gain since October 2022, riding on a weak US dollar and expectations of an increase in demand from China — the world’s largest oil importer. China’s industrial production is starting to ramp up as the coronavirus scare in the country has subdued.

The Organization of the Petroleum Exporting Countries, or OPEC, is scheduled to release its monthly report on Tuesday, 17 January.

Cryptocurrencies

The cryptocurrencies market continued its upward trend from last week and traded higher after the US CPI data showed signs of cooling down in inflation. The surge lifted the global cryptocurrency market capitalisation above 975 billion USD on Sunday, 15 January. It marks a considerable improvement from the 850 billion USD mark it was at last week, a level it has struggled to reach since the November 2022 implosion at Futures Exchange (commonly known as FTX — a leading cryptocurrency exchange) before its bankruptcy.

During its ongoing bankruptcy proceedings, an attorney for FTX told a US court on Wednesday, 11 January, that it has recovered more than 5 billion USD in liquid assets but the extent of losses suffered by its customers in the collapse of the cryptocurrency exchange is still unknown.

Bitcoin, the world’s largest cryptocurrency, is showing early signs of another bull run as it broke the 20,000 USD resistance on Saturday, 14 January. Before the recent breakout, the price of Bitcoin had been trapped in a small range between 16,000 USD and 17,000 USD for weeks. The token was trading at 20,863.60 USD at the time of writing. On the other hand, Ethereum, the second largest digital currency by market capitalisation, was trading at 1,551.64 USD on Sunday, 15 January.

Take advantage of market opportunities by sharpening your trading strategy and trading the financial markets with options and multipliers on Deriv Trader.

US stock markets

*Net change and net change (%) are based on the weekly closing price change from Friday to Friday.

The major US stock indices continued their good performance from the previous week, with the Nasdaq rising by 4.54%, the S&P 500 by 2.67%, and the Dow Jones by 2.00%. The 2 consecutive weeks of upward movement marks a stark contrast from the end of 2022 when the indices finished the year on an extended bear run.

The stock market movement was helped by the alleviation of selling pressure as data by the University of Michigan Surveys of Consumers showed that the US consumers expect an ease in inflation over the next 12 months.

The beginning of the earnings season will be marked by Morgan Stanley and Goldman Sachs releasing their fourth-quarter earnings results on Tuesday, 17 January. Analysts have been predicting a nearly 4% fall in the Q4 for S&P 500 companies. Such an outcome would mark the first year-over-year decline since the third quarter of 2020, according to analysts.

The retail sales data — which is an indicator of consumer spending — will be released on Wednesday, 18 January. The US financial markets will be closed on Monday, 16 January, on account of Martin Luther King Jr. Day.

Now that you’re up-to-date on how the financial markets performed last week, you can improve your strategy and trade CFDs on Deriv MT5.

.webp)

Weekly market report – 15 Nov 2021

It was a volatile week for U.S. stocks. Following last week's record highs across the three largest indices in the U.S, all the major indices closed lower on Friday, 12 Nov 2021. The Dow Jones Industrial Average dropped 0.6%, while the S&P 500 dipped 0.3%. Additionally, the Nasdaq Composite fell by around 0.7%.

US Indices

It was a volatile week for U.S. stocks. Following last week's record highs across the three largest indices in the U.S, all the major indices closed lower on Friday, 12 Nov 2021. The Dow Jones Industrial Average dropped 0.6%, while the S&P 500 dipped 0.3%. Additionally, the Nasdaq Composite fell by around 0.7%.

Over the past week, Tesla CEO Elon Musk sold around $6.9 billion worth of his company's stock, which affected the tech-heavy Nasdaq Composite. Tesla's share price plummeted 15.4% for the week, marking the company's worst weekly performance in 20 months. The U.S. markets moved down as inflationary pressures appear to be persisting longer and more severely than the Federal Reserve initially anticipated. October's CPI data revealed that inflation is at its hottest levels in over three decades, reporting a price jump of 6.2% from the previous year (YoY). But, stock market investors aren't sweating just yet. Despite a turbulent end to the week, all three major indices are not sitting far from their record highs, suggesting that U.S. equities have managed to shrug off rising inflationary pressures for now. This resistance is most likely down to the fact that rising prices have not coincided with rising real yields of Treasury bonds or a downturn in corporate earnings.

Trade US indices options on Deriv Trader and CFDs on Deriv MT5 Financial and Financial STP accounts.

Forex

Due to the response to high US inflation data and weak UK GDP data (6.6% actually vs 23.6% earlier), the GBP/USD currency pair has been on a downward trend, leading to doubts about whether the Bank of England will hike interest rates in December. On the other hand, EUR/USD was also affected (EUR/USD down by around 1%), mainly due to the US inflation reports and the European Central Bank maintaining its conservatism on the interest rates, citing inflation as 'transitory'. AUD/USD ended the week around the 0.73 mark, losing its gains over the month. This loss was due to the weak Unemployment Rate (5.2% actual vs 4.8% forecast) and the US dollar shooting up after the CPI hit its high (6.2% YoY).

The week's economic calendar includes:

- GDP (Q3) and CPI (October) for the EU

- RBA Meeting Minutes for the AUD

- Retail Sales and Initial Jobless Claims for the USD

- CPI and Retail Sales for the GBP

Trade forex options on Deriv Trader and CFDs on Deriv MT5 Financial and Financial STP accounts.

Commodities

Gold climbed up by more than 2% since last week, mainly because of inflation concerns. Last week's CPI (0.9% actual and 0.6% forecast) and Core CPI (0.6% actual and 0.4% forecast) reports were higher than expected, causing speculation that the Federal Reserve would raise interest rates sooner than anticipated, boosting Treasury yields. Although gold and Treasury Yields have an inverse correlation, gold has managed to keep up the momentum (since gold is considered an inflation hedge).

Silver improved last week, aided by inflation data, which was backed up by the Consumer Sentiment Report (66.8 actual versus 72.5 forecast) citing uncertainty about inflation.

Since last week, there has been a decline in oil prices due to expectations of the Fed interest rate increase to combat inflation and reports that President Biden will release oil from the Strategic Petroleum Reserve to tame down the price.

Among the economic events scheduled for this week are:

- Retail Sales (1.2% forecast vs 0.7% previous)

- Crude Oil Inventories and Initial Jobless Claims (260k forecast vs 267k previous)

If the Retail Sales data is weaker than expected, it may be because of inflation fears, and this negative impact would boost metals in general and vice versa.

Trade commodities options on Deriv Trader and CFDs on Deriv MT5 Financial account.

Cryptocurrency

In the crypto market, prices ended the week mostly lower as bullish investors failed to maintain prices near last week's record highs for Bitcoin ($68,900 level) and Ether ($4800 level). On Thursday, 11 Nov 2021, BTC/USD dropped 0.12%, then declined 1% for the week.

The price of Bitcoin reached an early intraday high of $65,421 on Friday, 12 Nov 2021, before switching its direction. After falling short of its first major resistance level of $65,528, BTC moved lower to a late intraday low of $62,225 and later crashed through its first and second major support levels, at $64,066 and $63,342, respectively. After finding late support, it rose through the major support levels to end the day at around the $64,100 levels.

Ether recorded an all-time high of $4,851 on Wednesday, 10 Nov 2021, surpassing the $4,800 level for the first time. The price dropped slightly towards the end of the week, hovering around the $4,600 mark early Friday morning, 12 Nov 2021.

Additional gains are expected among the cryptocurrency giants, as the Bitcoin network is set to receive its most significant upgrade since 2017. The software upgrade called Taproot will enhance transaction privacy and efficiency. More importantly, it will unlock the potential for smart contracts – a crucial feature of its underlying blockchain technology.

Trade cryptocurrency options on Deriv Trader and CFDs on Deriv MT5 Financial and Financial STP accounts.

Sorry, we couldn’t find any results matching .

Search tips:

- Check your spelling and try again

- Try another keyword