Results for

Market Radar: Big banks’ Q4 earnings report, Eurozone inflation, US retail sales, Bitcoin price trajectory

This week’s market radar features big banks' Q4 earnings reports, UK and Eurozone inflation, US and China retail sales, and Bitcoin price trajectory.

Join us in this week's Market Radar where we explore the key decisions and data releases that are influencing market trends.

This week, we explore:

- Morgan Stanley & Goldman Sachs Q4 earnings report

- UK and Eurozone inflation data

- US and China retail sales

- Bitcoin price trajectory

Stay informed with our weekly market analysis on Market Radar.

Yen on the rise: Will the Bank of Japan hold its dovish stance?

Explore the factors driving the yen higher, the potential economic impacts, and whether the central bank is likely to intervene to halt the currency's gains.

The Japanese yen reached 143.50 against the dollar on Tuesday, 9 January 2024. This swing, however, comes amidst a backdrop of mixed signals and uncertainties surrounding the Bank of Japan's (BOJ) monetary policy trajectory.

The Bank of Japan’s plan to pivot from its dovish stance may have been affected by the need to assess the adverse impact of the 1 January Noto Peninsula disaster on the economy. Plus, falling inflation rates in Tokyo reaffirmed speculations that the BoJ will not exit the negative interest rates policy in January.

Inflationary pressures and Tokyo’s leading indicator

Tokyo's core consumer price index (CPI) climbed 2.1% year-on-year in December, aligning with market expectations and following November’s 2.3% increase. This data, closely monitored as a leading indicator of nationwide trends, will be a focal point for the BOJ’s upcoming policy meeting on January 22-23.

BOJ Governor Kazuo Ueda emphasised the need for continued monetary easing until current cost-push inflation transitions to a demand-driven price surge supported by robust wage gains. However, concerns arise from declining household spending, which fell for the ninth consecutive month in November, underscoring the fragility of the Japanese economy.

Analysts anticipate the BOJ’s quarterly meeting with regional branch managers in January to offer insights into policymakers’ confidence regarding sustained wage growth.

Global macroeconomic influences

Meanwhile, the global spotlight turns to the US Consumer Price Index (CPI) this week. A higher-than-expected reading could dampen expectations of an imminent rate cut by the Federal Reserve. Following a strong U.S. employment report, Fed fund rate futures currently indicate a 57.3% probability of a rate cut in March.

Technical analysis of USD/JPY suggests further upside resistance at the 61.8% retracement level of 147.44, with support near 140.

As the global economic landscape undergoes transformation, further developments in the market are eagerly awaited. These shifts, coupled with domestic considerations, will ultimately shape the BOJ's policy trajectory and the fate of the yen.

What this means

On 25 December 2023, BOJ Governor Kazuo Ueda highlighted the potential positive aspects of higher interest rates in normal economic conditions. While reiterating a commitment to pursue stable inflation through monetary easing patiently, the minutes indicate that the Governor is inclined to wait for the April wage results.

A shift away from ultra-loose monetary policies by the BOJ or an earlier-than-expected rate cut by the Fed could contribute to a heightened sentiment favouring the purchase of yen.

A beginner's guide to the various types of ETFs

Learn the benefits of ETFs and diversify your portfolio by discovering the most popular types of ETFs that suit your trading style.

Exchange-traded funds (ETFs) have exploded in popularity over the last decade, offering traders an efficient way to gain exposure to markets at a low cost. While the most popular ETFs track major indexes, further exploration reveals a diverse world of specialised ETFs catering to specific sectors, factors, and trading strategies.

Much like flavours at an ice cream shop, ETFs come in many varieties — from conservative vanilla index funds to more adventurous rocky road sector stakes. Whether you crave stability, growth, or something in between, the ETF menu has options to satisfy your trading appetite.

In this beginner's guide, we'll explore the major ETF categories, including stock, bond, commodity, and more. You'll learn the distinguishing features of each type, their typical holdings, and the role they can play in a trader’s portfolio.

The different types of ETFs

- Stock or Equity ETFs: Stock ETFs are funds that hold baskets of stocks that mimic various stock market indexes. Stock ETFs allow traders to gain exposure to a diverse collection of equities in a single purchase.

Stock ETFs like VOO and IVV can provide long-term CFD trading exposure to a selection of stocks from the S&P 500 in proportions that aim to mimic the index's performance. These are considered some of the best ETFs for long-term global ETF index tracking.

- Sector and Industry ETFs: Sector and industry ETFs, like those on Deriv, provide targeted exposure to specific market segments compared to broader market ETFs. They allow tactical stakes based on economic and market analysis.

For example, Deriv offers ARKK.arcx. The ARK Innovation ETF buys domestic and foreign equity securities of companies that are expected to benefit from developments in artificial intelligence, automation, DNA technologies, energy storage, fintech, and robotics.

- Bond ETFs: Bond ETFs track a specific bond market index. These are traded on stock exchanges like individual stocks, which makes them a liquid and accessible option.

Popular options include the iShares Core US Aggregate Bond ETF (AGG) for US bonds and the iShares iBoxx High Yield Corporate Bond ETF (HYG) for corporate bonds.

These examples are useful CFD trading tools for accessing the bond markets. Their diversified baskets of securities make them potentially suitable options for long-term trading strategies.

- Style ETFs: Style ETFs track indexes of stocks filtered by specific characteristics like market capitalisation, value, growth, and dividend yield.

Value ETFs like IVE and VTV buy stocks that appear underpriced by the market based on metrics like price-to-earnings and price-to-book ratios.

Growth ETFs like IVW and VUG buy stocks with strong earnings and revenue growth.

- Commodity ETFs: Commodity ETFs hold futures contracts for individual natural resources like oil, gold, or silver.

For instance, commodities ETFs like GLD can bring CFD trading exposure to gold and other resources. Traders sometimes use these for short-term CFDs, while others hold them long term.

- Volatility ETFs: Volatility ETFs are exchange-traded funds that provide exposure to market volatility through the use of various derivative strategies.

Unlike traditional ETFs that simply track an index, volatility ETFs aim to allow traders to speculate on or hedge against fluctuations in the overall volatility of the market. They attempt to profit from volatility increases and declines as a trading vehicle.

Here is an overview of these major ETF categories, their distinguishing features, typical holdings, and their role in a trader's portfolio:

.png)

With their diversity of exposures and strategies, ETFs offer traders an extensive menu to customise their trading portfolios. Whether you prefer simplicity or specificity, passive indexing or active speculation, ETFs offer something for every portfolio strategy and risk tolerance. By understanding the diversity of the ETF landscape, you can thoughtfully select exposures to suit your trading goals and appetite.

Open a demo or real trading account on Deriv and check out our suite of ETF offerings. Practise with virtual funds in a demo account, or start trading ETFs with real money and take advantage of the opportunities ETF trading offers.

2024's trilemma: Inflation, stagflation or soft landing

Gain sharp insights into US inflation, Eurozone stagflation, AI's impact on semiconductors, Japan's interest rate conundrum, and key emerging market trends. A must-read for shaping your trading strategies in 2024.

Forget crystal balls; success in 2024 hinges on navigating a changing landscape moulded by tightening monetary policies and shifting power dynamics in 2023.

While a base case scenario paints a picture of gradual growth, hidden currents of risk and opportunity swirl right beneath the surface. This 2024 outlook dissects the key trends and challenges market investors can navigate to unlock potential success in the year ahead.

US: Soft landing, but watch out for inflationary tailwinds

Excess consumer savings are waning, and higher interest rates are impacting demand for goods, services, and housing. While a temporary weakening of US quarterly Gross Domestic Product (GDP) growth is expected at the beginning of 2024, a full-blown recession is not anticipated by a wider set of economic analysts.

The Federal Reserve foresees continued moderation of overall inflation and slower economic growth in 2024 before reaching its 2% Consumer Price Index (CPI) target by the fourth quarter of 2026.

The Federal Reserve, playing a delicate balancing act, eyes both slowing growth and persistent inflation. Their recent pause on rate hikes hints at an acknowledgement of sluggishness, aligning with core Personal Consumption Expenditure (PCE) readings potentially dipping below projections.

However, memories of transitory inflation remain fresh, and worries about resurgent price pressures due to exceptional growth or potential oil shocks linger. As Jerome Powell himself warns, further rate hikes haven't been ruled out. Three quarter-point rate cuts are on the table for 2024, according to Federal Open Market Committee (FOMC) December minutes, but it’s uncertain when they will be implemented.

Adding to the complexity is the shifting landscape of Treasury yields. The Fed’s reduced buying power and ballooning US budget deficit create a perfect storm for rising long-term rates. Waning foreign demand for Treasuries and Japan’s loosening of yield curve control further fuel the upward trajectory. Nevertheless, it’s crucial to remember that these yields are merely correcting from historically low levels and a prolonged inversion. US equity markets are poised to navigate the initial half of the year, drawing guidance from underlying fundamentals and economic data releases, with potential shifts or geopolitical uncertainties looming thereafter.

China: Growth slump meets long-term goals

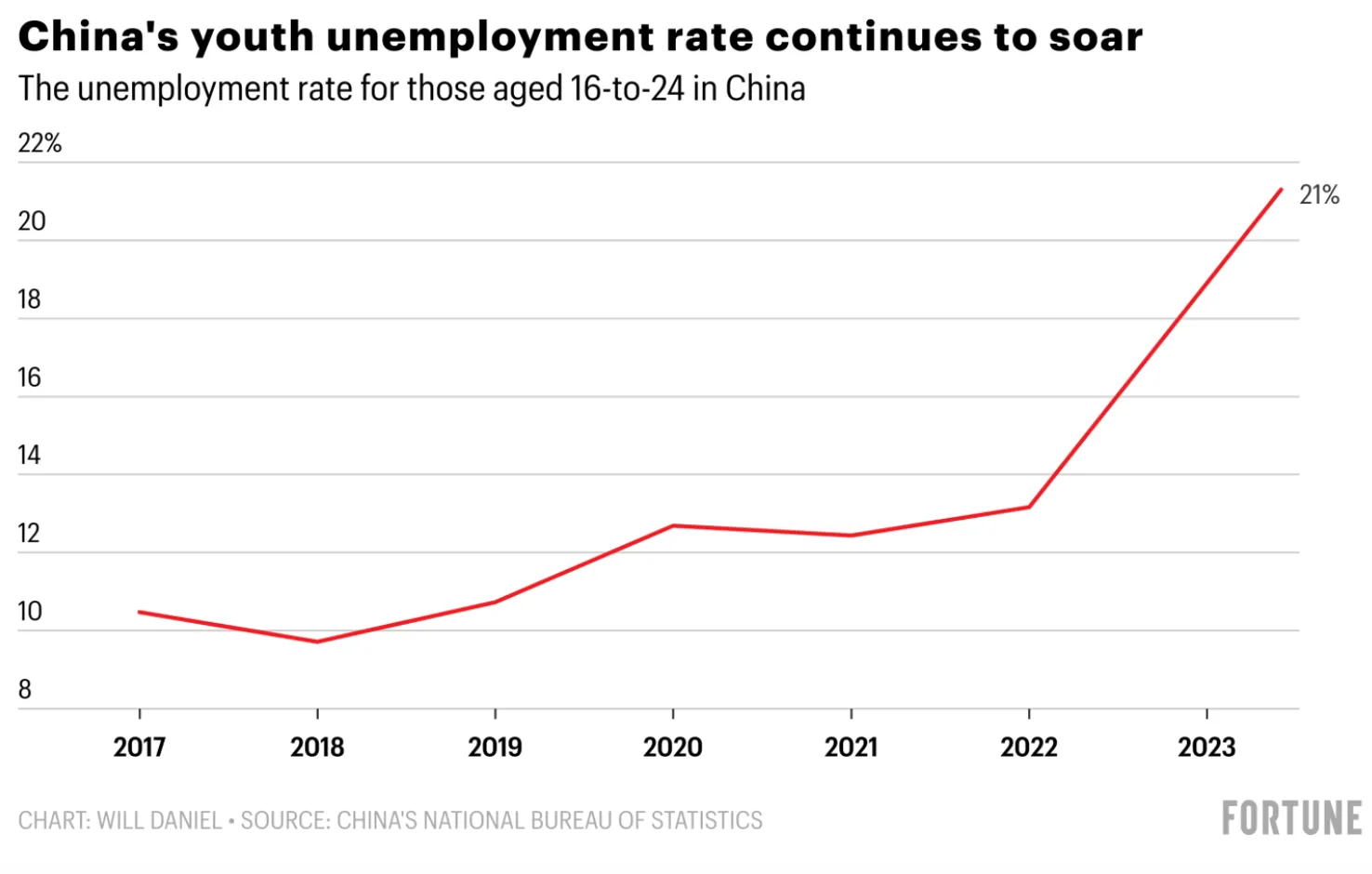

2024's initial optimism for a post-pandemic China sputtered out as an extended housing slump, rising youth unemployment, and regulatory uncertainties slammed the brakes on the market. With construction and real estate long fuelling the engine of the economy, the property crisis ripples deep, triggering significant equity selloffs.

A glimmer of hope shines from a potential yuan rally in 2024, the first in three years. A narrowing interest rate gap could stanch capital outflow, as predicted by a Bloomberg survey. However, limited rate cuts and an unclear bailout for the property sector cast shadows on the rebound. Foreign investors remain on the sidelines, awaiting decisive government action before diving back in. Despite challenges, Chinese leaders express unwavering confidence in their long-term vision for the nation's economic transformation. Structural reforms target common prosperity and sustainable growth, exemplified by China's commitment to peak carbon emissions in 2030 and achieve carbon neutrality by 2060.

Japan to finally end interest rates

The yen faces renewed pressure following a significant New Year's Day earthquake in Japan, complicating the Bank of Japan's efforts to eliminate negative interest rates this month. While it's not likely that there will be changes in January, most people expect the negative interest rates to end in April or later in 2024. This suggests that there could be increased volatility in the value of the Japanese yen.

Eurozone, UK: Battling inflationary pressures

The UK and Europe are expected to experience a mild recession and minimal growth in 2024, characterised by slower growth and stubborn inflation.

Inflation has been more persistent in these regions due to their heavier reliance on commodities and energy imports. Energy and commodity prices are expected to stay above pre-crisis levels, influenced by geopolitical uncertainties and anticipated US rate cuts. Consequently, key interest rates in the EU and the UK are projected to remain higher for longer to control inflation.

Higher interest rates tend to have visible effects on government debt, leading to a continued rise in national debt. With substantial debt from the pandemic and the conflict in Ukraine, the capacity of EU and UK governments to stabilise their economies is diminishing. Limited options for additional fiscal stimulus result in a stagflation scenario, unlike the US, where growth remains resilient and inflation is under control.

Emerging markets: Standing on their own

As interest rates in the US cool and the dollar eases its grip, JP Morgan predicts a resurgence in emerging markets during the latter half of 2024. This momentum is fuelled by a global shift in supply chains, escaping the long shadow of China's dominance.

Beneficiaries of this realignment include regions like Latin America, Europe, the Middle East and Africa (EMEA), the Association of Southeast Asian Nations (ASEAN), and India. These rising stars offer a potent cocktail of cost-effective labour, robust manufacturing, and a treasure trove of essential commodities. Boasting a bustling manufacturing scene, a vast workforce, and natural resources like energy, copper, and lithium (the lifeblood of electric vehicles (EVs) and renewables), Latin America shines as a prime contender.

Rising foreign direct investment (FDI) paints a vibrant picture for ASEAN, with Vietnam leading the charge. Major companies seeking diversification are setting up shop, with Vietnam's stellar growth becoming a textbook case. In the tech arena, Malaysia emerges as a champion of advanced semiconductor packaging and testing, while Singapore reigns supreme as a wafer fabrication hub. Indonesia's nickel wealth and Thailand's established auto supply chain make them vital players in the electric vehicle game.

Narendra Modi's recent electoral triumphs have bolstered India's already impressive growth, fuelled by global supply shifts and competitive labour costs. This translates to record highs for Indian stocks in 2024, with the Sensex and Nifty reaching dizzying new peaks.

While uncertainty may linger, the potential for a robust revival in emerging markets during the second half of 2024 appears tantalising. With lower rates, a weaker dollar, and shifting supply chains, these rising stars stand poised to grab the spotlight and redefine the global economic landscape.

Artificial intelligence: Spotlight on semiconductors

The recent advancement in AI is a game-changer for globalisation. It stands out as a key highlight for 2024 with profound implications for trading and investments.

Generative AI is a type of AI algorithm that creates content based on existing data. It fuels innovation in various industries beyond tech—from transport and healthcare to education and retail. Notable beneficiaries include gaming firms, electric vehicle manufacturers, e-commerce players, and cloud providers.

Analysts forecast a positive outlook for the semiconductor sector in 2024. The industry is anticipated to sustain its recovery from the 2022 downturn and exhibit growth across all segments. Advancements in AI heavily depend on high-end semiconductor chips for processing and analysing data. Ongoing trade tensions between the United States and China in the semiconductor sector have created a supply-demand imbalance. This resulted in increased prices and margins for semiconductors, impacting the valuations of semiconductor companies.

As of 2023, the semiconductor industry has rebounded, and one significant factor behind this resurgence is NVIDIA Corp. (NVDA), a frontrunner in the expanding Graphics Processing Units (GPU) market for AI applications. Nvidia’s stock has surged more than threefold, making it the first chipmaker to achieve a market capitalisation exceeding USD 1 trillion. Another noteworthy player in the AI sector, Advanced Micro Devices Inc. (AMD), claimed the second spot among index components, experiencing a remarkable stock increase of nearly 130% this year.

Beyond chipmakers in the US, Singapore, and Malaysia, as mentioned earlier, other clear beneficiaries include Korea and Taiwan. Korean fabs are developing the next generation High Bandwidth Memory chips that will benefit from the widespread adoption of AI. Taiwan boasts a complete industrial supply chain that supports current and future AI industry trends.

Risks to monitor: Geopolitical, financial instability

In 2024, amid a crucial election year, global geopolitical tensions and risks are on the rise. Two major conflicts and elections in 40 countries, including major ones like the US, UK, and EU, contribute to the uncertainty. Morgan Stanley anticipates increased volatility in higher-risk assets compared to the previous year.

Investment channels and supply chains are intricately linked to the leadership of each country. Ongoing US-China tensions, the Russia-Ukraine conflict, and the persistent Israel/Hamas dispute are substantial risk factors.

Additionally, concerns about slowing economic growth raise questions about the fiscal sustainability of governments and corporate debt. Eastspring Investments, based in Singapore, takes a defensive stance in the US credit space, preferring US Investment Grade over High Yield corporate bonds. Their research indicates potential underpricing of corporate refinancing risks as the maturity wall expands in the coming years.

Both the EU and the US are grappling with a growing threat of defaults on commercial real estate loans, posing risks for financial institutions. Higher funding costs, potential regulatory capital weaknesses, and increasing risks associated with commercial real estate loans, coupled with weakened demand for office space, prompt a review of banks. Moody’s Investors Service has downgraded the credit rating of 10 smaller US banks and may extend this to major lenders like US Bancorp, Bank of New York Mellon, State Street, and Truist Financial, highlighting mounting pressures on the industry.

Despite a surge in bond yields, credit spreads have surprisingly not widened significantly. This phenomenon has played a role in minimising bankruptcies and job losses. Analysts across various top Wall Street banks foresee a slight deterioration in credit conditions in 2024, providing a buffer for companies, jobs, and overall economic growth against a more severe decline.

Conclusion

Navigating the changing investment landscape in 2024 requires a clear understanding of macroeconomic factors, asset allocation strategies, and the role of artificial intelligence within businesses and private assets.

In the initial half of 2024, the trajectory of markets is poised to be heavily influenced by ongoing economic fundamentals, as the ramifications of elections and potential credit risks are yet to be fully assessed.

While investors can typically anticipate and prepare for various risks, the most significant threat often arises from an unexpected "curveball" — an event that catches everyone by surprise. Since these events aren't considered in market prices, they can cause major disruptions when they occur. Recent examples include the unforeseen COVID-19 pandemic and the war in Ukraine, both of which few investors expected. Recognising the unpredictable nature of the financial landscape, it's sensible to account for potential unforeseen challenges in 2024 as well.

Market Radar: Japan’s inflation rates, US CPI and PPI data, UK mortgage rates

This week’s Market Radar discusses the impact of Japan inflation rates, US CPI and PPI data, and UK mortgage rates.

Join us in this week’s Market Radar as we discuss the economic landscape, starting from Japan's inflation puzzle to the impact of US CPI and PPI data, and UK mortgage rates.

This week, we explore:

- Japan's inflation rates

- UK mortgage rates

- US CPI and PPI data

Stay informed with our weekly market analysis on Market Radar.

.webp)

Market recap: Week of 2–5 Jan 2024

Stay informed with our weekly market recap from 2–5 Jan, 2024. Get insights on the latest trends and developments in the financial world.

Japan earthquake

Nikkei 225: On 1 January 2024, Japan faced an Earthquake. Reflecting on the 2011 aftermath, the Nikkei 225 dropped 86 points to 10,348 yen on 11 March 2011. Subsequent concerns over the earthquake’s impact on earnings triggered a flood of sell orders.

Within days, the index plummeted to 8,605 from 10,348. The event serves as a reminder of the market’s sensitivity to seismic events and the subsequent investor reactions.

Stlouisfed: On 1 January 2024, Japan experienced an earthquake, prompting a look back at the impact on USDJPY after the 2011 earthquake. Following the 2011 event, the JPY appreciated significantly. From 10 March to 17 March 2011, the yen strengthened by about 5% against the USD.

Responding to the heightened market volatility, G-7 financial authorities announced measures on Thursday, 17 March 2011. The yen swiftly rebounded, nearly returning to its pre-earthquake levels.

Apple stock

CNBC: Apple shares dip 4% post-Barclays downgrade, citing concerns about weakening iPhone 15 sales as a potential precursor to iPhone 16 and broader hardware projections.

Meanwhile, Bloomberg reports Chinese government discouraging state employees from using iPhones, a claim denied by Chinese authorities.

Market responsiveness to both internal and external factors underscores the delicate balance in tech stocks.

GBP/USD rally

Market Screener: HSBC’s Dominic Bunning deems the GBP/USD rally, soaring from $1.20 in October to $1.27 in late November, as ‘completely unjustified’ based on interest rate differentials.

Predicts pound’s retreat as focus shifts to overall yield spreads, anticipating GBP/USD slide towards 1.20. S&P Global Market Intelligence’s Rob Dobson notes a contraction in UK manufacturing output at year-end 2023, attributing it to tough conditions domestically and in key export markets.

Meanwhile, the dollar gains traction on the year’s first trading day, backed by higher U.S. yields amid anticipation of crucial economic data.

Chip stocks

Reuters:

- U.S. chip stocks on a downward trend, PHLX semiconductor index down 2.1%.

- AMD, Qualcomm, Broadcom contribute to losses with drops exceeding 2%.

- BofA Global Research suggests exposure to Nvidia, Marvell Technology, NXP Semiconductors, ON Semiconductor.

- Chip index down nearly 7% since 27 December record high close.

- Wells Fargo recommends KLA and Applied Materials as top picks.

- Market volatility in the semiconductor sector after its strongest year since 2009.

UK politics

Bloomberg:

- UK executives push for urgent interest rate cuts to boost the economy.

- PM Rishi Sunak hints at a general election by Jan 2025; the exact month remains uncertain.

- Conservatives trail Labour by ~20 points in polls; Sunak faces pressure to retain power.

- March Budget crucial for Tories’ fortunes, potential tax cuts in focus.

US economic outlook

Reuters:

- Economists predict 170,000 jobs added in Dec, fewer than previous month’s 199,000.

- ADP report shows largest monthly job increase since August, private payrolls up by 164,000.

- Initial claims for state unemployment benefits drop by 18,000.

- Dollar strengthens against most currencies on Thursday, fueled by robust U.S. labour market data.

- Market expectation of multiple Fed rate cuts this year dampened.

- UBS’s Brian Rose: “In the short run, we think the dollar could gain a bit; market is too aggressive in pricing in Fed rate cuts. Our base case is the Fed will wait until May before cutting.”

- Majority of analysts (36 of 59) see a greater risk in their three-month forecast: the dollar trading stronger against major currencies than currently predicted.

Europe’s economic indicators

Financial Review:

- ECB closely examines domestic drivers, with salaries in the spotlight.

- German inflation accelerates less than expected in December.

- Consumer prices rise 3.8%, below economists’ 3.9% prediction.

- Muted boost from energy may restrain wage demands.

- French inflation report echoes a comparable scenario earlier in the day.

- ECB aims for a faster return to the 2% inflation target.

- Trade Idea 2024: Morgan Stanley suggests shorting EURUSD.

Trader’s guide to navigating stock market volatility

How to navigate the 2024 trading landscape with VIX insights, adaptive strategies, and a deep understanding of stock market volatility.

The stock market is known for its ups and downs, and understanding and navigating these fluctuations is crucial for traders.

In this comprehensive guide, we will explore the concept of stock market volatility, its causes, and its impact on investment strategies. We will also provide practical insights and strategies to help you steer through the ever-changing market landscape.

What is stock market volatility?

Stock market volatility is a measure of how much the stock market's overall value fluctuates up and down. It can also refer to the volatility of individual stocks. Volatility is commonly calculated using the statistical measure called standard deviation, which represents how much an asset's price varies from its average price.

External events that create uncertainty often contribute to increased stock market volatility. For example, during the early days of the Covid-19 pandemic, the stock market experienced significant volatility, with major stock indexes rising and falling by more than 5% each day. This uncertainty led to frantic buying and selling as investors grappled with the unknown.

The year 2023 has brought unique challenges. With the S&P 500 and Nasdaq experiencing significant downturns, and amidst a backdrop of inflation and aggressive monetary policies by the Federal Reserve, understanding market dynamics is more critical than ever.

It's important to note that volatility doesn't measure the direction of stock price movements. Instead, it measures the size of the price swings. Volatility can be thought of as a measure of short-term uncertainty.

Types of volatility

There are two main types of volatility: historical volatility and implied volatility.

1. Historical volatility: Historical volatility is a measure of how volatile an asset was in the past. It provides insight into how much an asset's price has fluctuated over a specific time period. Historical volatility can help traders understand the potential range of future price movements based on past performance.

2. Implied volatility: Implied volatility is a metric that represents how volatile traders expect an asset to be in the future. It is derived from the prices of put and call options. Implied volatility is often used in options pricing models, as it helps determine the market's expectations of future price movements.

How do we measure stock market volatility?

There are several methods used to measure stock market volatility, including metrics specific to individual stocks and broader market indices.

1. Beta: Beta is a metric that measures a stock's historical volatility relative to a benchmark index, such as the S&P 500. A beta of more than one indicates that a stock has historically moved more than the benchmark index. A beta of less than one implies a stock that is less reactive to overall market moves.

2. VIX (Volatility Index): The VIX, also known as the fear gauge, is a measure of the expected volatility in the stock market over the next 30 days. The VIX is calculated by the Chicago Board Options Exchange (CBOE) and is often used as an indicator of market sentiment. A significant increase in the VIX may indicate heightened fears and anticipation of large stock price movements.

Factors influencing volatility

Stock market volatility can be influenced by a combination of micro- and macro-economic factors. Understanding these factors can help traders anticipate and navigate periods of increased volatility.

1. Macroeconomic factors: Macroeconomic factors refer to broader economic conditions that can impact the stock market as a whole. These factors include:

- Shocks and uncertainties: Events such as economic downturns, policy changes, or global crises can create unpredictability and increase the probability of volatility.

- Monetary policy: Changes in interest rates, money supply, and inflation can influence market volatility.

- Political and societal events: Political instability, elections, or geopolitical tensions can create market uncertainty and volatility.

2. Microeconomic factors: Microeconomic factors relate to specific companies, industries, or sectors. These factors can influence the volatility of individual stocks or sectors. Examples include:

- Company-specific news: Earnings reports, mergers and acquisitions, or changes in management can impact a stock's volatility.

- Industry-specific trends: Technological advancements, regulatory changes, or shifts in consumer behaviour can affect the volatility of certain industries.

Managing volatility in trading strategies

Volatility in the stock market can present both risks and opportunities for traders. Here are some strategies to consider when managing volatility in your trading portfolio:

- Diversification: Spread your trades across different asset classes to mitigate risks.

- Long-term trading: Focus on long-term growth potential rather than short-term fluctuations.

- Dollar-cost averaging: Trade a fixed amount regularly, regardless of market conditions.

- Rebalancing: Adjust your portfolio periodically to maintain your preferred risk level.

- Seek professional advice: A financial advisor can offer personalised guidance based on your goals and risk tolerance.

Stock market volatility is an inherent aspect of investing. Understanding the causes and impact of volatility can help you make informed trading decisions and develop strategies to navigate market fluctuations.

Remember that volatility and risk are not the same, and long-term traders should focus on the fundamental growth prospects of their trades rather than short-term price swings.

Sign up for a free Deriv demo account and practise measuring stock market volatility risk-free. The demo account comes with virtual funds so you can test these tips and determine which works best for you.

.webp)

How to protect yourself on P2P platforms

Learn how to avoid fraud and scams when using P2P payment services and safeguard your finances on P2P platforms.

Protecting your funds and identity is as crucial as ever. Fraudsters are resourceful in finding ways to exploit your information. Read on to learn how to protect yourself when making peer-to-peer payments.

Peer-to-peer (P2P) platforms have revolutionised sending and receiving money. But convenience and speed often come at a cost: vulnerability to fraud and scams.

As the digital landscape evolves, so do the tactics employed by fraudsters. It pays to know how to protect yourself from digital deception.

Let's explore some essential tips to help you stay safe on peer-to-peer payment systems.

How to avoid P2P scams

Use secure and reliable platforms

- Use peer-to-peer payment platforms that focus on security.

- Choose platforms that offer reliable dispute resolution mechanisms and strong customer support. Deriv P2P is an example of such a platform.

- Research different platforms and read reviews before deciding which one to use.

Enable two-factor authentication (2FA)

- Protect your account by enabling 2FA whenever possible.

- 2FA requires a second verification step when logging in or making transactions.

- This makes it harder for scammers to gain unauthorised access to your account.

Protect your personal information

- Never share sensitive personal or financial information.

- This includes your ID number, credit card details, or login credentials.

- Legitimate platforms will only ask for this information in secure channels.

Only deal with trusted individuals

- It's crucial to only deal with individuals you trust, especially for high-value payments.

- Verify the recipient's identity. Ensure that you're comfortable with the payment before proceeding.

- On Deriv P2P, you can exchange with individuals with reliable ratings and stats.

Double-check user information

- Always double-check and verify the user information before initiating any payment.

- Fraudsters may use similar names or email addresses to deceive you.

- Take the time to confirm the details to ensure you're sending money to the right person.

Be wary of requests for advanced payments

- Be cautious if someone asks you to release funds before they pay you.

- Scammers often try to convince users to send money upfront and disappear afterwards.

- Always ensure you've received the payment before releasing funds.

Regularly monitor your account activity

- Frequently watch your account activity. This includes your P2P account, bank account, and anywhere else you have money going in and out.

- Review transaction details, payment history, and notifications for suspicious or unauthorised activities.

- Report any concerns or suspicions immediately. On Deriv P2P, you can raise disputes via our reliable support team.

Take charge of your safety on P2P platforms

Staying vigilant and following these tips will go a long way in protecting yourself. As technology advances, so do the tactics of scammers. Always stay informed and aware to safeguard your finances.

2024 market outlook on global inflation trends, stocks vs bonds, and key insights

This week, we feature the 2024 market outlook, economy forecast, global inflation trends, stocks vs bonds, and more.

Join us as we share some of the key macro events that would likely shape the financial landscape of and market outlook of 2024:

- Global inflation trends

- Impact on commodities

- Stocks vs bonds

- Eurozone, UK inflationary pressures

- Bank of Japan’s strategic shift, USD/JPY impact

Stay informed with our weekly market analysis on Market Radar.

Sorry, we couldn’t find any results matching .

Search tips:

- Check your spelling and try again

- Try another keyword