Gold price outlook: Central banks are providing a floor

Gold’s remarkable steadiness near $4,050 per ounce is no accident, according to reports. Beneath the noise of fading rate-cut bets and dollar strength lies a deeper structural force: relentless buying by the world’s central banks. From Beijing to Ankara, policymakers are quietly rewriting the rules of monetary safety, using gold as their hedge against political risk, currency instability, and waning trust in the U.S. financial order.

This demand has become the invisible hand supporting bullion, according to analysts. Even as speculative traders pull back and ETF flows flatten, sovereign buyers are helping to anchor the market.

With the People’s Bank of China extending its 12-month gold-buying streak and other central banks following suit, gold’s downside risk now looks more like a pause than a collapse - a floor reinforced by nations, not funds.

What’s driving gold right now?

The latest U.S. jobs data has reset expectations across global markets. The September Nonfarm Payrolls report showed a gain of 119,000 jobs, more than double what economists expected, while unemployment inched up to 4.4 %.

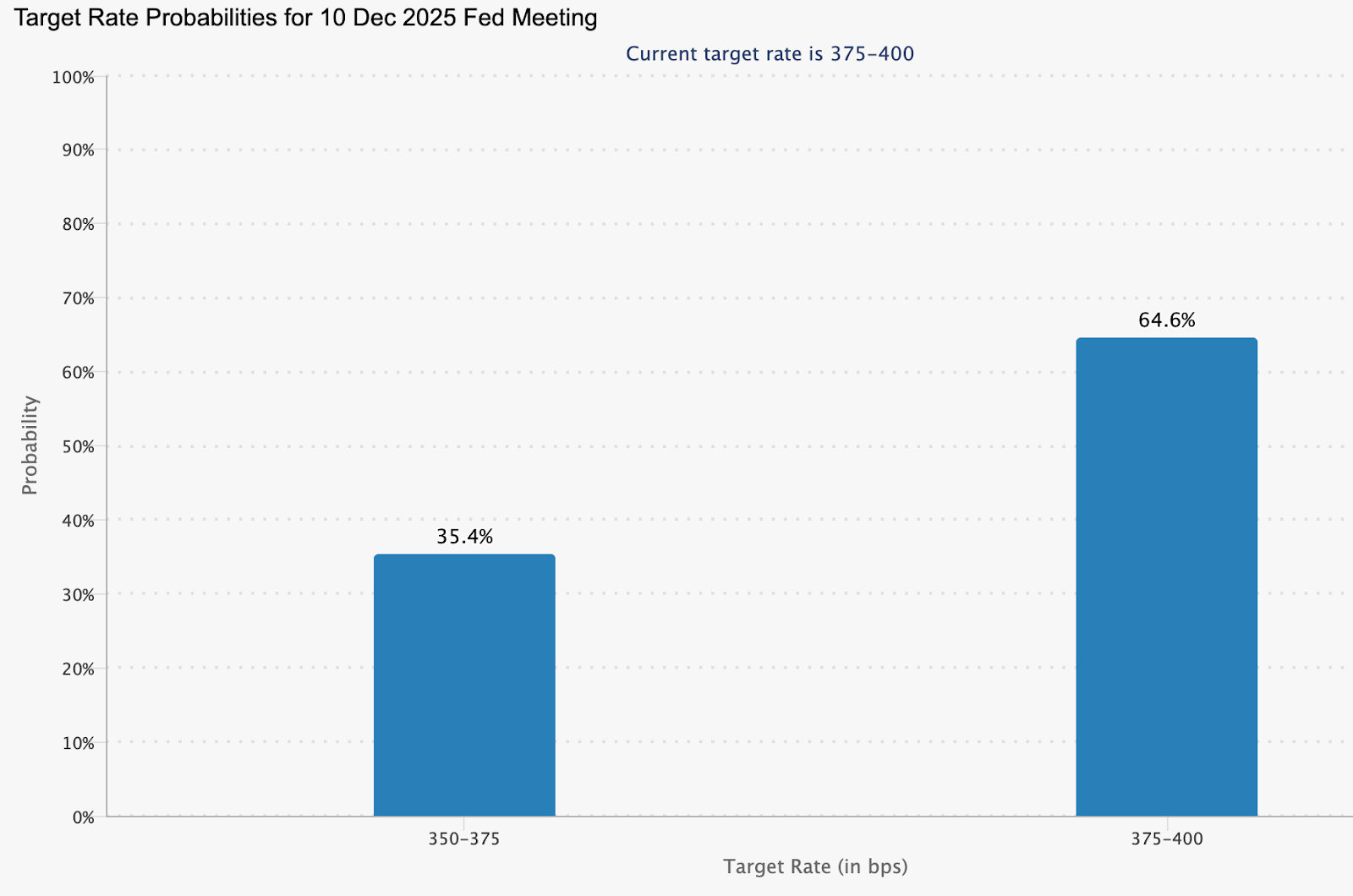

On the surface, the data appears mixed - strong hiring but softening momentum - yet it was enough to prompt investors to dial back their calls on a December rate cut from the Federal Reserve.

That recalibration lifted the dollar and U.S. yields, typically a toxic combination for gold. But the metal barely flinched. The reason is that central-bank demand has altered gold’s sensitivity to policy cycles.

According to data from the World Gold Council, official sector purchases now account for nearly a quarter of annual demand - a structural shift from a decade ago. When the Fed hesitates, central banks don’t.

The People’s Bank of China (PBoC) has reported gold purchases for 12 consecutive months, adding 0.9t in October, which lifted the total to 2,304t, representing 8% of China’s foreign exchange reserves and marking a full year of uninterrupted buying. Turkey, Poland, and India have all joined the trend of accumulation.

Why it matters

Market watchers say this quiet sovereign accumulation is reshaping the role of gold in the global financial system. What used to be a “risk-off” trade is now part of the national reserve strategy. The freezing of Russian foreign assets in 2022 prompted governments to reassess their exposure to the dollar-dominated system, and gold emerged as a neutral alternative.

As Zaner Metals strategist Peter Grant puts it, the latest U.S. jobs data “confirms a slowing yet stable market - but that doesn’t reduce the appetite for safety.”

For policymakers in emerging markets, gold offers something paper assets can’t: insulation from sanctions, inflation, and the politics of currency. For investors, this means that gold’s price is no longer solely a function of interest rates or risk appetite. It’s a geopolitical indicator - a mirror of how much trust remains in the current monetary order.

Impact on markets and investors

The most striking change in this cycle is that gold is holding near record highs even as the U.S. dollar index (DXY) trades at its strongest level in months. The traditional inverse relationship has weakened. According to analysts, both assets are being purchased for the same reason: safety. This dynamic challenges the idea that gold only rallies when rates fall.

For traders, that complicates short-term positioning. With gold now roughly 7% below its October record of $4,380, momentum has cooled, but structural demand remains intact. ETF flows, although mildly negative in recent weeks, show no signs of panic.

Retail investors have trimmed exposure, but the official sector has replaced them as the marginal buyer. For long-term investors, this shift suggests that pullbacks may offer opportunities rather than warnings, especially if macroeconomic uncertainty deepens into 2026.

Expert outlook

Analysts remain divided on how far this central-bank bid can carry the metal. Goldman Sachs still sees the recent weakness as “a blip, not a reversal,” maintaining that both sovereign and private investment demand will underpin prices through 2026. UBS projects a possible climb to $4,900 per ounce within the next two years, assuming continued diversification away from dollar reserves.

The main risk to that outlook lies in monetary complacency. If U.S. data stays firm and the Fed reaffirms its “higher for longer” stance, speculative interest could fade further. But for now, gold’s resilience speaks for itself. The market is adjusting to a new reality - one where central banks, not traders, set the tone.

Gold technical insights

At the time of writing, Gold (XAU/USD) is trading around the $4,030 region, hovering near the $4,020 support level. The RSI is flat and close to the midline, indicating a lack of strong momentum in either direction - a sign of market indecision.

Meanwhile, Bollinger Bands have started to narrow, reflecting lower volatility after recent swings. The price is oscillating near the mid-band, suggesting a potential consolidation phase before the next breakout.

On the upside, $4,200 and $4,365 remain key resistance levels, where traders may expect profit-taking or renewed buying interest if bullish sentiment returns. Conversely, a break below $4,020 could open the door to the $3,940 support, where increased selling pressure or liquidations may occur.

Key takeaways

Gold’s resilience in late 2025 isn’t a mystery - it’s a message analysts expressed. The same institutions that once trusted U.S. Treasuries are now buying bullion to insure against policy, politics, and uncertainty. Traders may fade the rally, but central banks aren’t flinching. As the Fed navigates a divided policy outlook and global reserves continue to shift eastward, the floor under gold looks as firm as the hands holding it.

The performance figures quoted are not a guarantee of future performance.