What Powell’s dovish tilt and Ueda’s hawkish stance mean for USD/JPY

The U.S. dollar slipped to a four-week low after Federal Reserve Chair Jerome Powell signalled that downside risks to employment were growing, fuelling expectations for a September rate cut. At the same time, Bank of Japan Governor Kazuo Ueda pointed to accelerating wage growth in Japan, reinforcing expectations that the BoJ may resume tightening by October. The combination highlights a policy divergence that could decide whether USD/JPY climbs toward 150 or reverses closer to 140.

Key takeaways

- Powell’s Jackson Hole speech increased market conviction of a September rate cut, with traders pricing 84% odds.

- Markets now expect a total of 53 basis points in cuts by year-end, though the path depends on upcoming U.S. inflation and labour data.

- The dollar index fell more than 1% on Powell’s comments, sending USD/JPY lower before a retracement bounce in Asia trading.

- U.S. debt has surged by $1 trillion in just 48 days, raising long-term concerns about fiscal sustainability and safe-haven appeal.

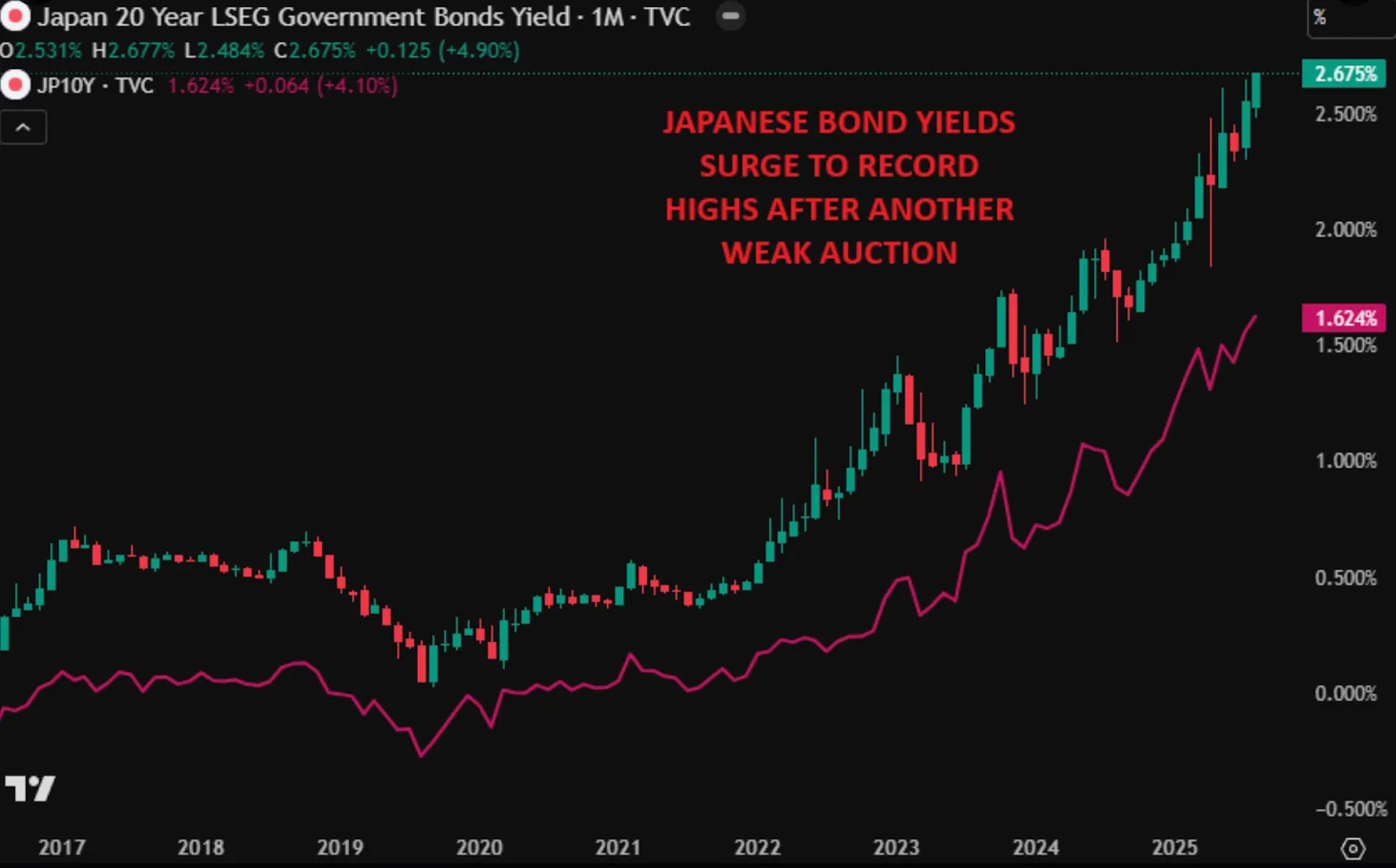

- Ueda flagged broadening wage growth and Japan’s tight labour market, sustaining expectations of a BoJ hike by October.

- Traders see USD/JPY capped near 147.50 resistance, with a breakout toward 150 or reversal toward 140 hinging on Fed-BoJ timing.

Powell’s dovish tilt: Fed rate cut expectations

At Jackson Hole, Powell told an audience of global economists and policymakers that “downside risks to employment are rising. And if those risks materialise, they can do so quickly.”

Markets immediately interpreted the statement as a dovish shift, raising bets on near-term easing. According to CME and LSEG data:

- 87% chance of a quarter-point cut at the 17 September FOMC meeting.

- Around 53 bps of cuts are priced in for the rest of 2025.

This pivot comes after months of shifting expectations:

- Early August: weak payrolls boosted cut bets.

- Mid-August: hot producer price inflation (PPI) and robust business surveys forced traders to scale back expectations.

- Post-Jackson Hole: Powell’s remarks effectively “cleared the bar” for dovishness, reviving confidence that cuts are imminent.

Goldman Sachs analysts noted that Powell’s message “cleared the market’s low bar for dovishness following a steady erosion in Fed cut pricing. It will be up to the data to determine the pace and depth of cuts.”

U.S. debt pressures weigh on the dollar

Beyond monetary policy, the U.S. fiscal backdrop is deteriorating rapidly. Federal debt has increased by $1 trillion in just 48 days, equivalent to $21 billion per day. Since 11 August 2025, alone, an additional $200 billion has been added, pushing totals close to $38 trillion.

Government spending now consumes 44% of GDP annually, levels not seen since World War II or the 2008 crisis - except this time, without an economic emergency.

Bond auctions have already shown signs of weakening demand, with investors requiring higher yields to absorb new issuance.

For FX markets, this creates a dual pressure:

- If the Fed cuts, the U.S. yield advantage erodes.

- If debt keeps ballooning, investors may question the dollar’s safe-haven appeal.

The combination leaves the dollar vulnerable even before accounting for Fed dovishness.

Trump’s attacks add credibility risk

Adding to dollar pressure is growing political friction. President Donald Trump has repeatedly criticised Powell - first for not cutting rates and more recently for cost overruns in the Fed building renovation.

Last week, Trump escalated by targeting Fed Governor Lisa Cook, saying he would fire her if she did not resign over mortgage holdings in Michigan and Georgia. These interventions have raised questions about the Fed’s independence, further clouding the U.S. policy outlook.

For global investors, a dovish Fed combined with political pressure risks undermining confidence in U.S. monetary stability, amplifying dollar weakness.

Ueda’s hawkish stance: Labour market drives BoJ outlook

In sharp contrast, BoJ Governor Kazuo Ueda struck a more confident tone at Jackson Hole. He noted that wage hikes are spreading from large enterprises to small and medium firms and are likely to accelerate further due to a tightening job market.

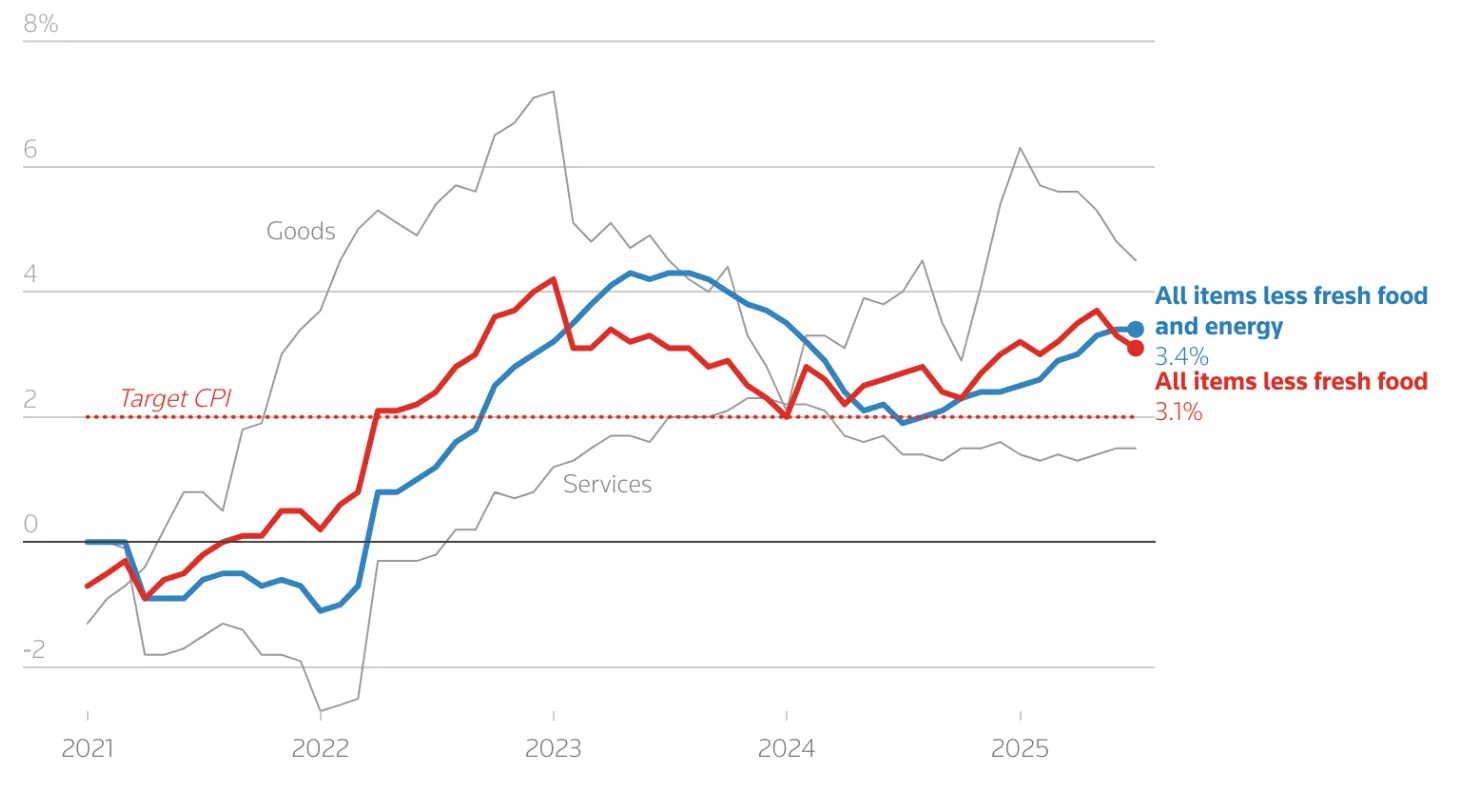

Japan’s core CPI rose 3.1% year-on-year in July, above forecasts and still well above the BoJ’s 2% target, even as inflation slowed for a second consecutive month.

This combination of sticky inflation and rising wages supports the case for the BoJ to resume rate hikes after pausing after January’s increase. Markets now see the probability of an October hike at around 50% - a coin toss.

USD/JPY: Central bank policy divergence in focus

The Fed leaning dovish while the BoJ leans hawkish sets up a clear inflection point for USD/JPY:

- Upside case (150): If U.S. data proves strong enough to delay cuts, or if safe-haven flows rise due to fiscal or geopolitical stress, USD/JPY could test 150.

- Downside case (140): If Powell delivers a September cut and Ueda follows with a BoJ hike in October, the divergence could spark a sharper yen rebound.

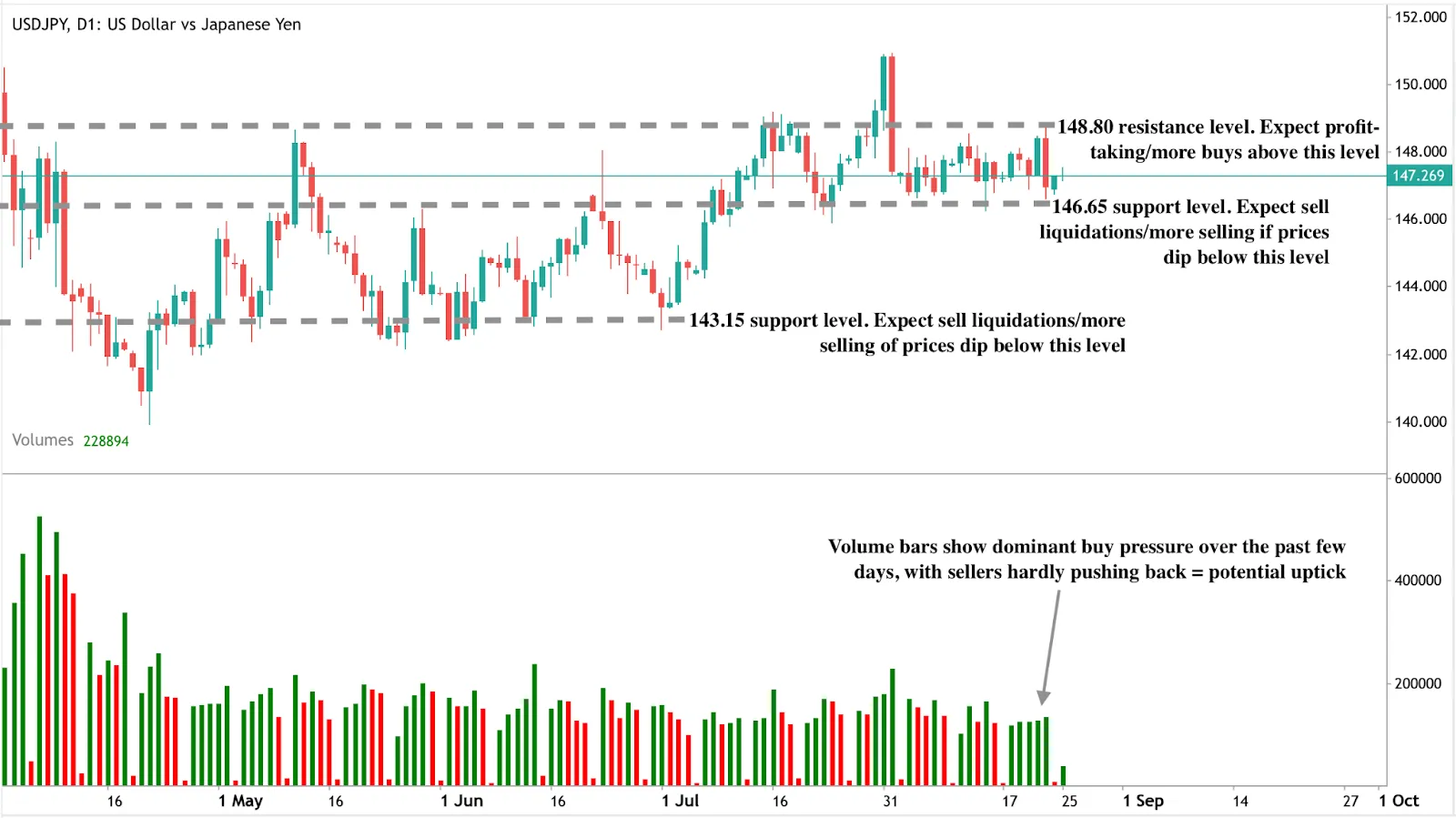

Currently, the pair trades near 147.40–147.50, a key resistance zone. The next catalysts are:

- PCE inflation (Friday) - the Fed’s preferred gauge.

- August payrolls (next week) - critical for confirming labour market risks.

USD/JPY technical analysis

At the time of writing, the pair is trading close to a support level, hinting at a potential price uptick. The volume bars showing dominant buy pressure with little pushback from sellers add to the bullish narrative. Should a price uptick materialise, prices could find resistance at the $148.89 price level. Conversely, if we see a dip, prices could find support at the $146.65 and $143.15 support levels.

Investment implications

For traders, USD/JPY positioning is highly sensitive to Fed-BoJ sequencing:

- Short-term: Tactical selling near 147.50–150 may appeal if U.S. data confirms a September cut.

- Medium-term: Yen strength could build if the BoJ hikes in October while the Fed continues easing.

- Risks: U.S. fiscal instability and political pressure on the Fed could accelerate dollar weakness beyond policy drivers.

With both central banks shifting, the next decisive move in USD/JPY hinges on which policy change comes first: a Fed cut or a BoJ hike.

Frequently asked questions

Why did Powell’s speech weaken the dollar?

Because it increased the likelihood of imminent Fed rate cuts, reducing U.S. yield appeal.

How much easing is priced in?

Markets see an 87% chance of a cut in September and 53 basis points of reductions by year-end.

Why is U.S. debt important for USD/JPY?

Exploding debt raises doubts about U.S. fiscal sustainability, making the dollar less attractive as a safe haven.

What supports BoJ hawkishness?

Broadening wage growth, sticky inflation above 2%, and structural labour shortages.

What are the key levels for USD/JPY?

Upside resistance near 147.50–150, downside support toward 140.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.