2026 için zor varlık sorusu: Neden platin odakta

Zor varlıklar artık niş bir koruma aracı gibi davranmıyor. 2025’te altın kararlı bir şekilde rekor seviyelere yükseldi, gümüş neredeyse %150 arttı ve platin %120’den fazla yükseldi – analistlere göre, bu hareketlerin ölçeği kısa ömürlü bir güvenli liman arayışından daha derin bir şeyi işaret ediyor. Aynı zamanda, ABD doları ve uzun vadeli Treasury gibi geleneksel defansif varlıklar, jeopolitik riskler arttığında performans göstermekte zorlandı.

Yatırımcılar altın ve gümüşteki ilk dalganın ötesine bakarken, dikkatler bir sonraki adımın ne olacağına kayıyor. Arz kısıtlamaları sıkılaşırken, stratejik sınıflandırmalar değişirken ve jeopolitik gelişmeler emtia piyasalarını giderek daha fazla şekillendirirken, platin 2026 için unutulmuş bir dipnot olmaktan çıkıp ciddi bir soru haline geliyor.

Zor varlık değişimini ne tetikliyor?

Grönland üzerindeki ABD–Avrupa geriliminin yeniden alevlenmesi değerli metallere olan talebi güçlendirdi, ancak bu talebi yaratan o olmadı. Altın ve gümüş, jeopolitik gerilimler yeniden gündeme gelmeden önce de yükselişteydi; bu yükselişi ABD’deki mali disiplin, para politikası güvenilirliği ve kurumsal güvenilirlik konusundaki artan endişeler tetikledi. Risk olayları sırasında uzun vadeli Treasury getirilerinin yükselmesi, artık büyümeden ziyade güvenin sorgulandığına dair tekrarlayan bir sinyal haline geldi.

Bu ortam, portföy oluşturmadaki kritik bir zafiyeti ortaya çıkardı. Devlet vaatlerine dayanan varlıklar – para birimleri ve devlet tahvilleri – belirsizlik arttığında artık tutarlı bir koruma sağlamıyor. Sonuç olarak, sermaye tamamen finansal sistemin dışında kalan varlıklara yöneldi. Bu anlarda ilk olarak altın fayda sağlasa da, tarih gösteriyor ki zor varlık teması benimsendiğinde kapsamı genişleme eğiliminde oluyor.

Neden önemli?

Analistlere göre, bu döngüyü önceki risk dönemlerinden ayıran şey, geleneksel güvenli limanlara olan güvenin aşınması. Dolar ve yen, eskiden olduğu gibi defansif akımları çekmekte zorlanırken, ABD Treasuries jeopolitik strese daha düşük değil, daha yüksek getirilerle tepki verdi.

Piyasalar, ABD açıklarının büyüklüğüne ve para politikasının önümüzdeki yıllarda siyasi baskı ile karşılaşabileceği algısına karşı giderek daha hassas görünüyor.

Analistler, zor varlıklara yönelimi taktiksel değil, yapısal olarak tanımlamaya başladı. Saxo Bank’tan Ole Hansen, metallerin artık “manşet odaklı korkudan ziyade sistem düzeyinde şüpheye” tepki verdiğini savunuyor. Bu bağlamda, zor varlıklar içinde çeşitlendirme, ilk pozisyon almak kadar önemli hale geliyor ve bu da dikkatin neden altının ötesine genişlediğini açıklıyor.

Metal piyasasına etkisi

Analistlere göre altın hâlâ temel dayanak, ancak gümüşteki aşırı yükseliş soru işaretleri doğurmaya başladı. Mevcut seviyelerde, gümüş özellikle fiyat hassasiyeti yüksek sektörlerde endüstriyel talepte bir çöküşü tetikleme riski taşıyor. Bu, yükseliş senaryosunu geçersiz kılmasa da karmaşıklaştırıyor ve yatırımcıları değerli metaller arasında göreli değeri yeniden değerlendirmeye teşvik ediyor.

Bu yeniden değerlendirmede platin öne çıkıyor. 2025’teki güçlü performansına rağmen, hâlâ tarihsel zirvelerinin oldukça altında ve son yıllarda altının gerisinde kaldı. Daha da önemlisi, arz-talep dinamikleri giderek daha kırılgan görünüyor. Altından farklı olarak, platin hem bir yatırım aracı hem de kritik bir endüstriyel girdi; bu da onu üretim, düzenleme ve jeopolitikteki değişimlere karşı daha hassas kılıyor.

Platin arz kısıtları ve endüstriyel gerçeklik

Platin talebinin yaklaşık %42’si hâlâ otomotiv sektöründen geliyor ve burada katalitik konvertörlerde kullanılıyor. Yıllarca, elektrikli araçların hızla yaygınlaşacağı beklentisi fiyatlar üzerinde baskı oluşturdu. Bu varsayımlar artık revize ediliyor. TD Securities, özellikle ABD’de içten yanmalı motor talebinin önceki tahminlerden daha dirençli kalmasını bekliyor ve bunun platin ve paladyuma destek sağlamaya devam edeceğini öngörüyor.

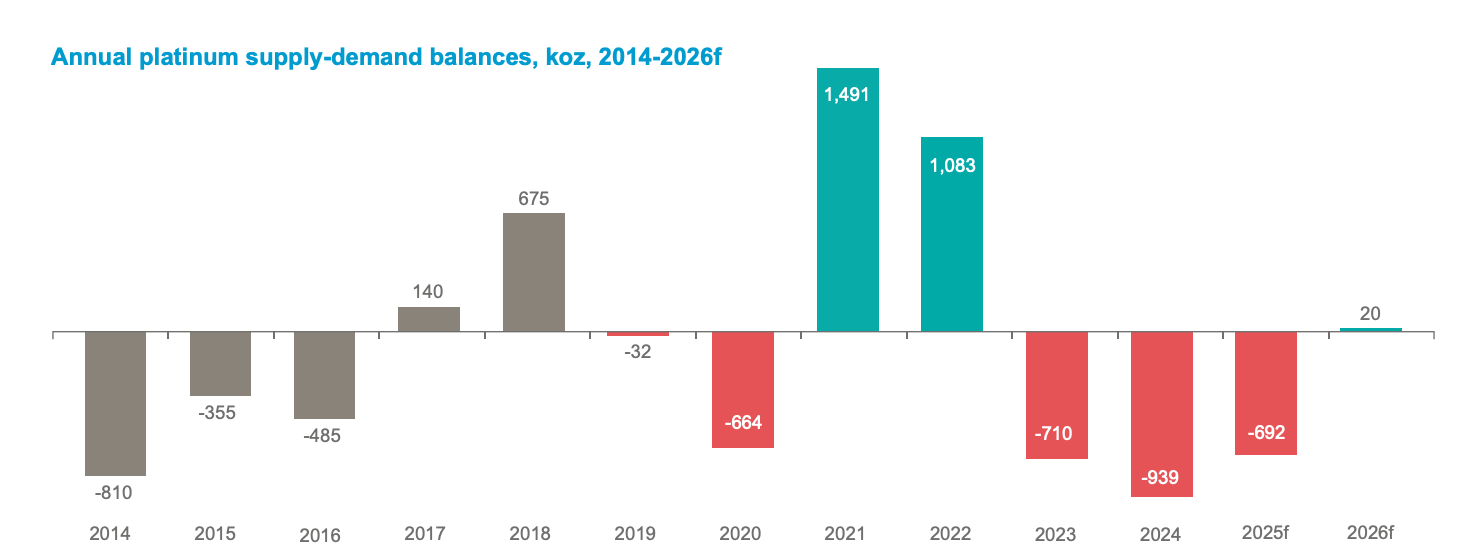

Aynı zamanda, arz daralıyor. World Platinum Investment Council, yer üstü stoklarının artık yalnızca yaklaşık 5 aylık talebi karşıladığını, bunun da 3 yıl üst üste açık verilmesinin ardından gerçekleştiğini bildirdi.

Yeni madencilik projelerine yapılan sınırlı yatırımlar, üretim artışını sınırladı ve piyasayı şoklara karşı savunmasız bıraktı. MKS PAMP’tan Nicky Shiels’e göre, sektör “geçici dengesizliklerden ziyade kalıcı yapısal açıklarla” karşı karşıya.

Jeopolitik, kritik metaller ve stratejik stoklama

Platin görünümü, siyaset tarafından da yeniden şekillendirildi. Kasım 2025’te US Geological Survey, platin ve paladyumu kritik metaller olarak sınıflandırarak stratejik önemlerini artırdı. Bu tanımlama, hem kurumsal hem de devlet düzeyinde arz güvenliği, ticaret politikası ve stok yönetimi tartışmalarını yoğunlaştırdı.

Devam eden Section 232 soruşturması kapsamında ABD tarifesi olasılığı, ertelense bile, “ne olur ne olmaz” stoklamaya yönelik bir kaymayı güçlendirdi. Londra gibi fiziksel piyasalarda, bu durum materyalin dolaşımdan çekilmesiyle yapay bir sıkılığa yol açtı. Stratejik kaynakların giderek daha fazla ulusal varlık olarak görüldüğü bir dünyada, fiyat oluşumu artık yalnızca ekonomik bir süreç değil.

2026 için uzman görünümü

2026’da platin için yapılan tahminler, fırsat ile risk arasındaki bu gerilimi yansıtıyor. MKS PAMP, fiyatların ons başına 2.000 $’a ulaşabileceğini öngörürken, TD Securities yılın ikinci yarısında ortalamaların 1.800 $’a daha yakın olmasını bekliyor. Daha temkinli tarafta ise BMO Capital Markets, fiyatların 1.375 $ civarında olacağını ve herhangi bir arz fazlasının spot piyasalar üzerindeki baskıyı hafifletebileceğini savunuyor.

Bu görüşleri birleştiren unsur, stoklara ilişkin belirsizlik. WPIC senaryoları, borsaya devam eden girişlerin açıkları derinleştirebileceğini, sürekli çıkışların ise piyasayı 2026’da fazlaya bile itebileceğini gösteriyor. Bu hassasiyet, platin’in neden giderek daha fazla stratejik bir soru olarak görüldüğünü ve altın ticaretinin basit bir devamı olmadığını ortaya koyuyor.

Öne çıkan mesaj

Zor varlık rallisi artık sadece altınla ilgili değil. Yatırımcıların riske, güvene ve çeşitlendirmeye bakışında daha derin bir değişimi yansıtıyor. Gümüş, endüstriyel talebi zorlayan seviyeleri test ederken, platin arz sıkılığı, stratejik önem ve jeopolitik riskle şekillenen bir metal olarak öne çıkıyor. 2026 için izlenmesi gereken kritik sinyaller; stoklar, ticaret politikası ve yatırımcı talebinin altının ötesine, daha geniş değerli metaller kompleksine yayılıp yayılmayacağı olacak.

Platin teknik görünümü

Platin, keskin bir yukarı ivmenin ardından yüksek seviyesini koruyor ve fiyat, üst Bollinger Band boyunca işlem görürken son zirvelerine yakın konsolide oluyor. Bantların sürekli genişliği, yükseliş hızının yavaşlamasına rağmen kalıcı yüksek volatiliteyi yansıtıyor.

Momentum göstergeleri, bir dönüşten ziyade bir yavaşlama gösteriyor; RSI daha önce aşırı seviyelere ulaştıktan sonra tekrar orta çizgiye yaklaşıyor. Yapısal açıdan bakıldığında, genel hareket 2.200 $ bölgesinin üzerinde sağlam kalmaya devam ediyor; önceki kırılma bölgeleri olan 1.650 $ ve 1.500 $ ise mevcut fiyatların oldukça altında kalarak son yükselişin büyüklüğünü vurguluyor. Genel olarak, mevcut fiyat hareketi, hâlâ yüksek volatilite rejiminde zirvelere yakın bir duraklamayı yansıtıyor.

Deriv Blog’da yer alan bilgiler yalnızca eğitim amaçlıdır ve finansal ya da yatırım tavsiyesi olarak değerlendirilmemelidir. Bilgiler zamanla güncelliğini yitirebilir ve bahsi geçen bazı ürün veya platformlar artık sunulmuyor olabilir. Herhangi bir işlem kararı vermeden önce kendi araştırmanızı yapmanızı tavsiye ederiz. Belirtilen performans rakamları, gelecekteki performans için bir garanti değildir.