Yenning potentsial carry trade savdolari USDJPY o‘sishiga sabab bo‘lishi mumkinmi?

Eslatma: 2025 yil avgustdan boshlab, biz Deriv X platformasini taklif qilmaymiz.

Har kuni treyderlar yen carry trade haqida 2006 yil kabi shivirlayotganini eshitmaysiz. Ammo hozir mana shunday vaziyat yuzaga keldi. Trumpning Yaponiya bilan “tarixiy” savdo kelishuvi, katta raqamlar va bojxona drama bilan birga, sarlavhalarda ko‘p tilga olingan bo‘lsa-da, valyuta bozori bunga unchalik ta’sirlanmagan ko‘rinadi. USDJPY 147 ostiga tushib ketdi, dollar momentumida sustlashish bor, va asl hikoya ehtimol jimjit qaytib kelayotgan carry trade bo‘lishi mumkin.

Yaponiya hali ham past foiz stavkalariga yopishib olgan va Fed hali burilish uchun tayyor emas, shuning uchun ilgari yenni qarzga olib, yuqori daromad izlash juda jozibali bo‘lgan shart-sharoitlar yana qaytib kelishi mumkin.

Bozorlarni harakatga keltirishi kutilgan Yaponiya-ABSh savdo kelishuvi

Prezident Trumpning aytishicha, AQSh Yaponiya bilan “ehtimol eng katta kelishuvni” amalga oshirdi. Katta da’vo. Kelishuvga Yaponiya tomonidan AQShga taxminan 550 milliard dollarlik investitsiya kiritilishi kiritilgan – bu raqam obligatsiya daromadlaridan ko‘ra ko‘proq e’tibor tortdi – va AQShga kirayotgan yapon mahsulotlariga 15% o‘zaro bojxona solig‘i joriy etildi. Buning evaziga Yaponiya o‘zining mashhur himoyalangan bozorlarini AQSh avtomobillari, yuk mashinalari va hatto guruchga ochishga rozi bo‘ldi.

Yaponiyaning eng yuqori savdo muzokarachisi Ryosei Akazawa X’da g‘alabali “Vazifa bajarildi” deb yozdi. Ammo bozorlar deyarli reaksiyaga kirmadi. USDJPY aslida pasaydi, dollar indeksi esa yumshadi.

Barcha siyosiy teatrga qaramay, treyderlar Vashington sarlavhalaridan ko‘ra foiz stavkalari kutilmalari va xavf dinamikasiga ko‘proq e’tibor qaratishdi.

Carry trade nima va nega u hozir muhim?

Carry trade haqida eshitganmisiz? U qaytib kelmoqda va hozir nega muhimligini tushuntiramiz. Asosida, bu arzon qarz olib, boshqa joylarda yuqori daromadli aktivlarga sarmoya kiritishdir. Yillar davomida Yaponiya deyarli nol foiz stavkasi muhiti bilan moliyalashtirish uchun eng maqbul valyuta bo‘lib xizmat qilgan.

U 2008 yildan keyin moda bo‘lmadi, QE yillarida qisqa muddatga qaytdi, so‘ngra o‘zgaruvchanlik qaytishi va global daromadlarning yaqinlashishi bilan yana yo‘qoldi.

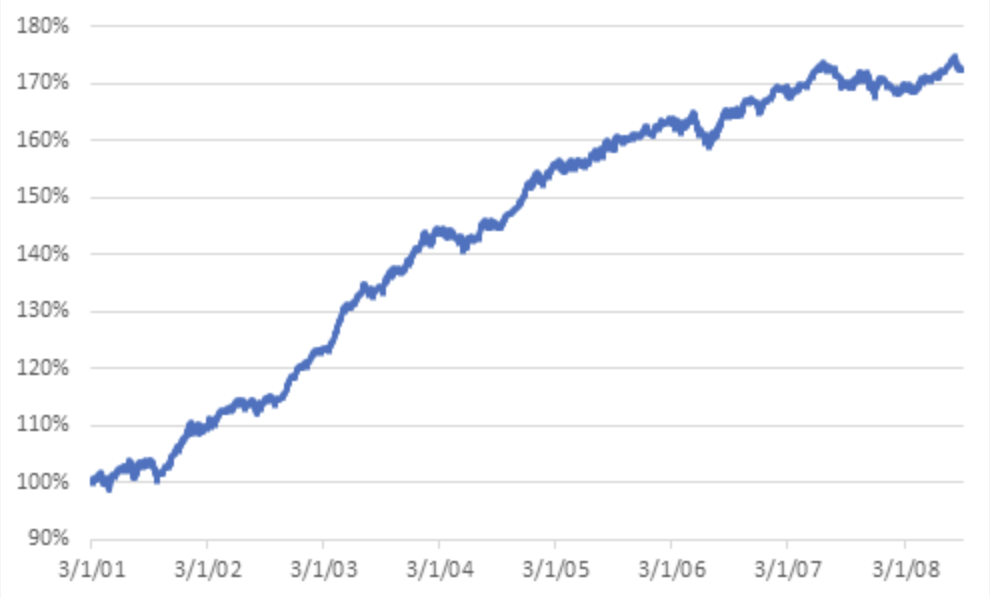

Quyida moliyaviy inqirozdan oldingi carry trade umumiy daromadlari ko‘rsatilgan.

Quyida esa moliyaviy inqirozdan keyingi carry trade umumiy daromadlari ko‘rsatilgan.

Ammo hozir biror narsa o‘zgarayapti. Fed hali ham foiz stavkalarini pasaytirishni rejalashtirishi mumkin, ammo yopishqoq inflyatsiya va bojxona bosimi uni ehtiyotkorlikka undamoqda. Shu bilan birga, Yaponiya sekinlashayotgan o‘sish, zaif ish haqi ma’lumotlari va nozik siyosiy fon bilan siqilish imkoniga ega emas. Bu carry trade uchun yoqadigan foiz stavkalari farqini yaratadi.

USDJPY ayniqsa tez o‘smayapti

Bularning barchasiga qaramay, USDJPY ko‘tarilmayapti. Aksincha. Juftlik yaqinda 147.00 darajasidan pastga tushdi, momentum indikatorlari charchoq belgilarini ko‘rsatmoqda. U yil boshida foiz stavkalari farqlari va xavfga tayyorlik kayfiyati asosida ko‘tarilgan edi. Ammo hozir? Treyderlar to‘xtab qoldi.

Sabablardan biri shundaki, BoJ global siqilishlarga qaramay, chetda qolmoqda. Tahlilchilar Yaponiya yumshoq inflyatsiya ma’lumotlari va siyosiy o‘zgarishlar siyosatchilarni ehtiyotkorlikka undayotganini ta’kidlaydi. Shuningdek, Yaponiya haqiqatan ham AQSh iqtisodiyotiga 550 milliard dollar kiritishi mumkinmi, degan noaniqlik mavjud, shuning uchun bozor qiziqmoqda, lekin ishonganicha yo‘q.

Siyosat va siyosat Tokyo shahrida uchrashadi

Yaponiyaning ichki fonini ham unutmaylik. Bosh vazir Shigeru Ishiba partiyasi yuqori palata ko‘pchiligini uch o‘rin bilan yo‘qotdi. U kichik koalitsiya hamkorlarining yordami bilan hokimiyatda qolmoqda, ammo uning ta’siri zaiflashmoqda va bu muhim.

Kamroq ko‘pchilik iqtisodiy islohotlarda harakatlanish imkonini kamaytiradi, ayniqsa AQSh talablarining kuchayishi bilan. Shunga qaramay, bozorlar natijani asosan qabul qildi, chunki ular Ishibani yoqtirishmaydi, balki yuqori soliqli muxolifatga o‘tish ehtimolini kamaytirgani uchun. Hozircha BoJ uchun hatto kamroq sabablar bor.

Shivir, hali qichqiriq emas

Demak, yen carry trade qaytdimi? To‘liq kuch bilan emas. Ammo uni qo‘llab-quvvatlagan shart-sharoitlar – past o‘zgaruvchanlik, foiz stavkalari farqi va jim BoJ – qayta paydo bo‘lmoqda. USDJPY juftligi portlash qilmayapti, lekin endi faqat sarlavhalarga asoslanib savdo qilmayapti.

Yen uchun xavfsiz boshpana talabining kamayishi, ayniqsa savdo kelishuvi 1 avgust bojxona muddati neytrallashtirilgani bilan bog‘liq. Yaponiya investitsiya raqami faktga qaraganda ko‘proq shov-shuv bo‘lishi mumkin, ammo tahlilchilar aytishicha, markaziy banklarning farqlanishi va eski strategiyalarning qaytishi haqidagi struktural hikoya og‘irlikka ega.

Carry trade qichqirmaydi. U hech kim qaramayotganda jimjit qaytadi. Treyderlar hali ham Trumpning bojxona taktikalari yoki Yaponiya investitsiya va’dasining ishonchliligi haqida bahslashmoqda, ammo orqa fonda yen o‘zining eski rolini – boshpana emas, balki moliyalashtirish vositasi sifatida – jimjit topmoqda.

Agar bu momentum kuchaysa? USDJPY tinglashni boshlashi mumkin.

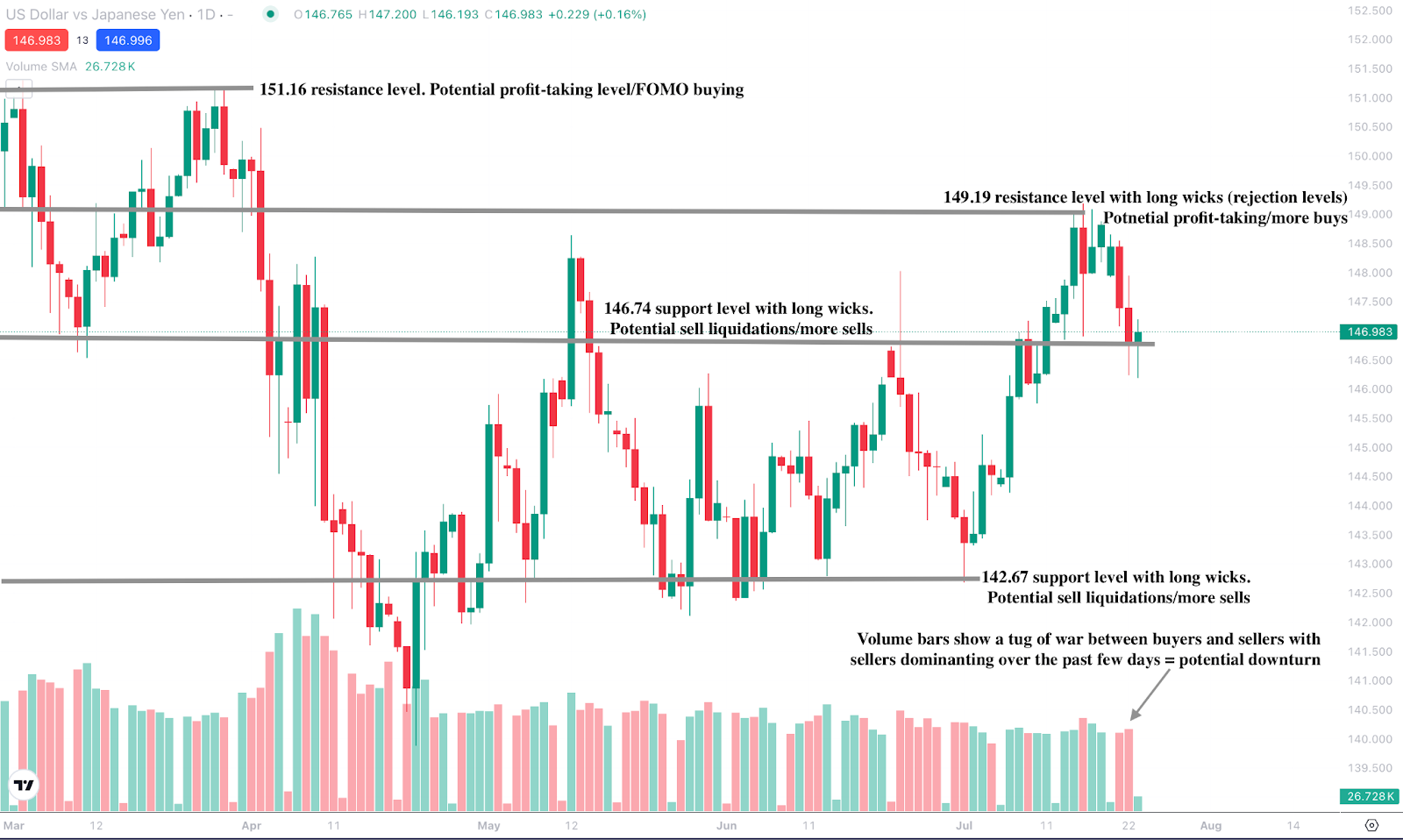

USDJPY texnik ko‘rinishi

Hozirgi vaqtda juftlik oldingi pasayishlardan biroz tiklandi, qo‘llab-quvvatlash darajasida harakatlanmoqda, yuqoriga siljish ehtimolini ko‘rsatmoqda.

Biroq, hajm diagrammalari so‘nggi ikki kunda kuchli sotish bosimini ko‘rsatmoqda, xaridorlardan esa kam qarshilik bor, bu xaridorlar qat’iy harakat qilmasa, yanada pasayish bo‘lishi mumkinligini bildiradi. Pastga harakat $146.74 va $142.67 qo‘llab-quvvatlash darajalarida to‘xtashi mumkin. Aksincha, yuqoriga harakat $149.19 va $151.16 narx darajalarida qarshilikka duch kelishi mumkin.

Bugun Deriv MT5 hisobingiz bilan USDJPY harakatlarini savdo qiling.

Mas’uliyatdan voz kechish:

Keltirilgan natijalar kelajakdagi natijalar kafolati emas.