Silver tightens as Copper falters: Are metals entering a supply-led rally?

Yes - the evidence increasingly points to a supply-led rally taking shape across key metals. Silver inventories have collapsed to multi-year lows, while copper production in Chile, the world’s largest supplier, continues to fall even as prices remain historically elevated. This is not a sugar rush. It is a structural squeeze.

When prices rise alongside shrinking stockpiles and weakening output, markets tend to quickly reprice risk. Silver and copper now sit at the centre of that adjustment, with physical availability, not speculative appetite, setting the tone for what comes next.

What’s driving the tightness in Silver and Copper?

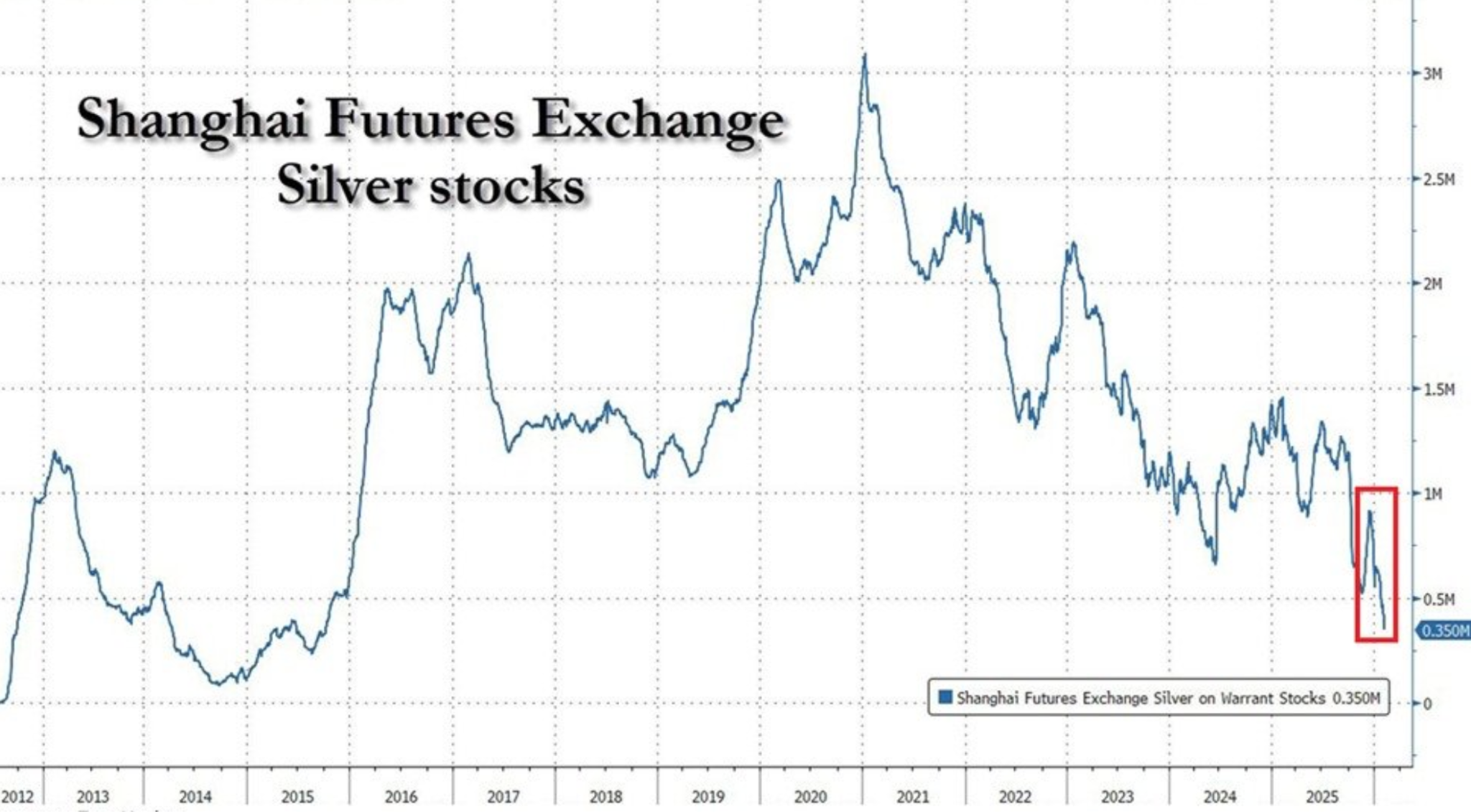

Silver’s story begins with physical scarcity. Deliverable inventories on the Shanghai Futures Exchange have fallen to around 350 tonnes, the lowest level since 2015 and an 88% decline from the 2021 peak.

That drawdown reflects years of steady industrial demand combined with limited mine growth and aggressive export flows. In 2025, China shipped large volumes of silver to London, easing global bottlenecks while hollowing out domestic reserves.

Price action has started to reflect that fragility. Even as XAG/USD dipped towards $82.50 this week on profit-taking and a firmer US Dollar, selling pressure remained shallow. Traders appear reluctant to push prices materially lower, given already stretched physical availability. Silver is no longer trading purely on macro headlines; supply is exerting its own gravity.

Copper’s constraint is more structural and arguably more troubling. Chile’s copper exports rose 7.9% year-on-year in January to $4.55 billion, but the increase was driven by a 34% jump in prices, not higher volumes. Output has now declined annually for five straight months, as ageing mines, falling ore grades, labour disruptions and operational setbacks take their toll.

Why it matters

When prices rise without production responding, markets are forced to reassess long-term assumptions. Analysts at Bloomberg Intelligence have warned that Chile’s struggles reflect a broader mining reality: new copper supply is increasingly expensive, slow to develop, and vulnerable to disruption. High prices alone are no longer enough to unlock meaningful output growth.

Silver faces a parallel problem. Much of its supply comes as a by-product of other mining activity, limiting producers’ ability to respond quickly to price signals. As one London-based metals strategist put it, “Silver looks cheap until you try to find it.” In tight physical markets, even modest demand shocks can trigger outsized price moves.

Impact on markets, industry, and inflation

For markets, the implication is a shift in regime. Metals rallies driven by supply constraints tend to be more persistent than those driven by cyclical demand. Silver’s sensitivity to US macro data remains intact, but each pullback now runs into the reality of depleted inventories. That changes trader behaviour, encouraging dip-buying rather than momentum selling.

For industry, especially renewables and electrification, the stakes are higher. Silver is critical to solar panel manufacturing, while copper underpins everything from power grids to electric vehicles. Persistent supply tightness raises input costs and complicates long-term planning, feeding through into broader inflation dynamics.

For policymakers, this creates an uncomfortable backdrop. Even if demand cools, constrained metals supply can keep price pressures alive. That complicates the narrative around disinflation and reinforces commodities’ role as a structural inflation hedge rather than a cyclical trade.

Expert outlook

Silver’s near-term path will continue to pivot around US data, including Retail Sales and delayed labour market reports. Signs of economic cooling or softer inflation would likely support prices, particularly given silver’s safe-haven appeal amid ongoing geopolitical uncertainty in the Middle East.

Copper’s outlook is slower-moving but no less consequential. Mining analysts broadly agree that Chile’s production issues will not be resolved quickly. New projects face technical, environmental and political hurdles, while existing operations struggle with declining grades. Even if prices consolidate, the absence of surplus capacity suggests copper is entering a prolonged period of structural tightness.

Silver technical outlook

Silver has stabilised after a sharp retracement from recent highs, with price consolidating near the middle of its recent range following an extended upside move. Bollinger Bands remain widely expanded, indicating that volatility is still elevated despite the recent moderation in price action.

Momentum indicators reflect this pause: the RSI has flattened around the midline after dropping from overbought territory, suggesting a neutral momentum profile following the earlier extreme conditions.

Trend strength remains elevated, as evidenced by high ADX readings, indicating that the broader trend environment remains strong even as short-term momentum has cooled. Structurally, price continues to trade well above earlier consolidation zones around $57 and $46.93, underscoring the scale of the prior advance.

Key takeaway

Silver and copper are no longer trading on sentiment alone. Shrinking inventories and faltering production suggest metals markets are entering a supply-led phase, where scarcity sets the price floor. Silver’s tight physical market and copper’s mining constraints point to sustained upside risk, even amid macro volatility. The next chapter depends less on demand surprises and more on whether supply can recover at all.

The performance figures quoted are not a guarantee of future performance.