Will the Fed cut rates faster in 2026 than the market expects?

Will the Federal Reserve cut interest rates faster in 2026 than markets expect? According to analysts, the growing divide inside the Fed suggests that the outcome cannot be ruled out. While official projections still signal a cautious path, some policymakers argue that inflation has cooled enough to justify deeper and faster easing.

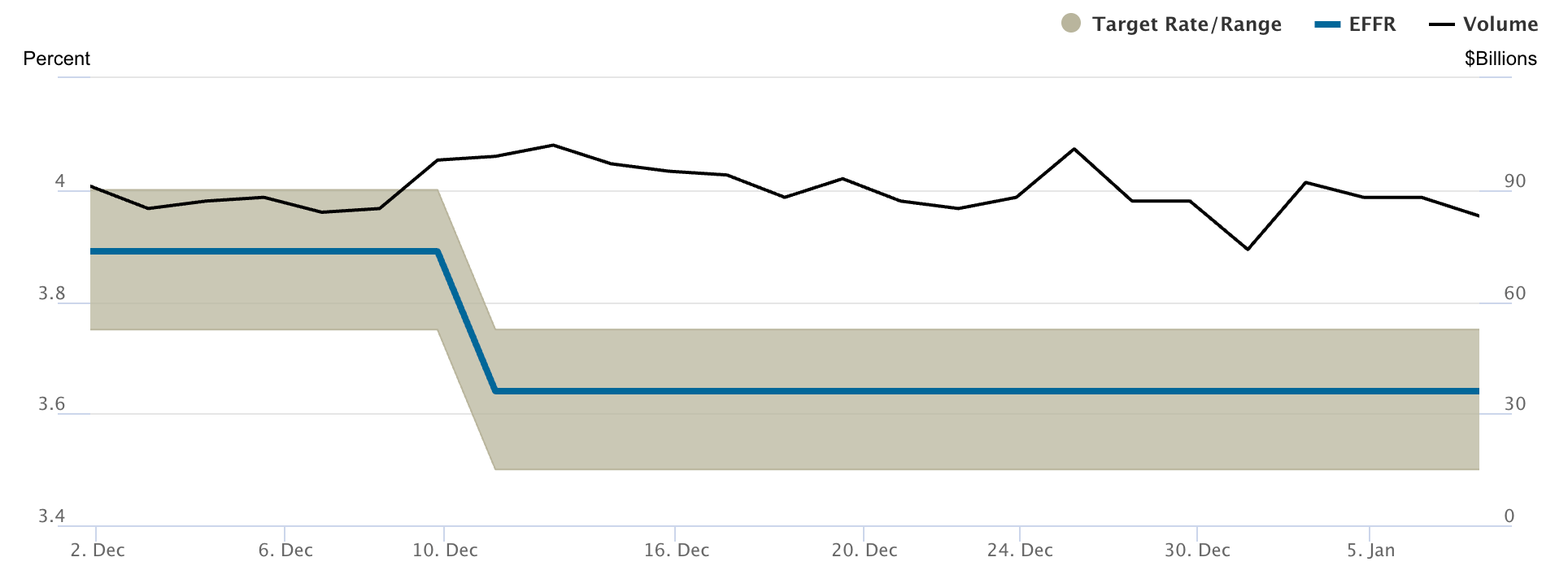

With the Federal Funds Rate currently sitting between 3.50% and 3.75%, the debate now centres on whether monetary policy is still unnecessarily restrictive.

That question has taken on greater urgency after Fed Governor Stephen Miran publicly called for up to 150 basis points of rate cuts this year. His stance contrasts sharply with market pricing and with other officials advocating patience. As labour market data softens and inflation drifts closer to target, investors are watching closely for signs that the Fed may ultimately move faster than it currently signals.

What’s driving the Fed’s rate cut debate?

The core of the disagreement lies in how Fed officials interpret progress on inflation and labour market slack. Miran argues that underlying inflation is already running near 2.3%, close enough to the Fed’s 2% target to allow meaningful rate cuts without risking a resurgence in prices. From his perspective, keeping rates elevated is suppressing hiring rather than containing inflation.

Other policymakers are less convinced. Several regional Federal Reserve bank presidents favour holding rates steady until more post-shutdown data clarifies the true state of employment and price pressures. They warn that inflation has a history of re-accelerating when policy eases too early, especially if demand proves more resilient than expected.

Politics has added another layer to the debate. Miran, appointed temporarily to the Board of Governors by President Donald Trump, has echoed concerns from the White House about recession and stagflation risks. While the Fed operates independently, the renewed political scrutiny underscores how sensitive rate policy has become as growth slows.

Why it matters

This split matters because markets trade expectations, not just outcomes. Even subtle shifts in Fed rhetoric can reprice bonds, equities, and currencies within minutes. When policymakers openly disagree, volatility tends to rise as investors reassess whether official guidance still reflects the likely policy path.

Economists also warn that the cost of waiting may be higher than the Fed assumes. Bloomberg Economics notes that restrictive monetary policy affects employment with a lag, meaning current job losses may reflect decisions made months earlier. If the Fed delays easing until unemployment rises more sharply, it may be forced into larger cuts later, potentially destabilising markets.

Impact on markets and consumers

For consumers, the pace of rate cuts directly affects borrowing costs. Credit cards, auto loans, and home-equity lines remain closely tied to short-term rates, keeping household finances under strain even as inflation eases. Faster cuts would gradually lower monthly payments and improve disposable income, particularly for borrowers on variable rates.

Analysts noted that the markets are already reacting to the uncertainty. Bond yields have become increasingly sensitive to labour data, while equity valuations now hinge on whether growth can stabilise without further policy support. A faster-than-expected easing cycle would likely weaken the US dollar, support risk assets, and steepen the yield curve, signalling confidence in a soft landing.

If the more hawkish faction prevails, tighter conditions may persist for a longer period. That outcome would favour defensive equities and keep volatility elevated as investors adjust to a slower-moving Fed.

Expert outlook

Based on reports, official Federal Reserve projections currently indicate only one rate cut in 2026, highlighting the gap between internal forecasts and Miran’s calls for aggressive easing. The new Federal Open Market Committee voting rotation also leans more hawkish, reducing the likelihood of rapid policy shifts in the near term.

However, analysts stress that data will ultimately drive decisions. Employment indicators such as jobless claims, wage growth, and participation rates will carry more weight than headline inflation alone. If labour market cooling accelerates without a rebound in prices, pressure for faster cuts will intensify.

For now, the Fed’s division reflects uncertainty rather than dysfunction. Policymakers are grappling with how a post-pandemic economy responds to prolonged restraint - and that uncertainty may shape monetary policy throughout 2026.

Key takeaway

The Federal Reserve enters 2026 divided between caution and urgency. While official forecasts still favour limited easing, calls for deeper cuts reflect growing concern about labour market weakness. If jobs data continues to soften without reigniting inflation, the Fed may ultimately cut rates faster than markets expect. Investors should closely monitor employment indicators, as they may influence the pace of policy shifts.

The performance figures quoted are not a guarantee of future performance.