Will gold in 2025 remain a hedge or turn policy-driven?

The gold price is struggling to hold above $3,300, raising the question of whether bullion still works as a traditional hedge or has become primarily a policy-driven asset. While the Federal Reserve’s higher-for-longer stance and a firm US dollar are capping upside momentum, steady central bank purchases led by China are providing a structural floor. Geopolitical risks and tariff concerns that once fuelled safe-haven demand appear to have less impact, suggesting that gold’s identity may be shifting.

Key takeaways

- Gold trades near $3,318 after a notable downturn, with a death cross formation looming.

- The Fed’s cautious stance and persistent inflation risks keep the US dollar strong, limiting safe-haven appeal.

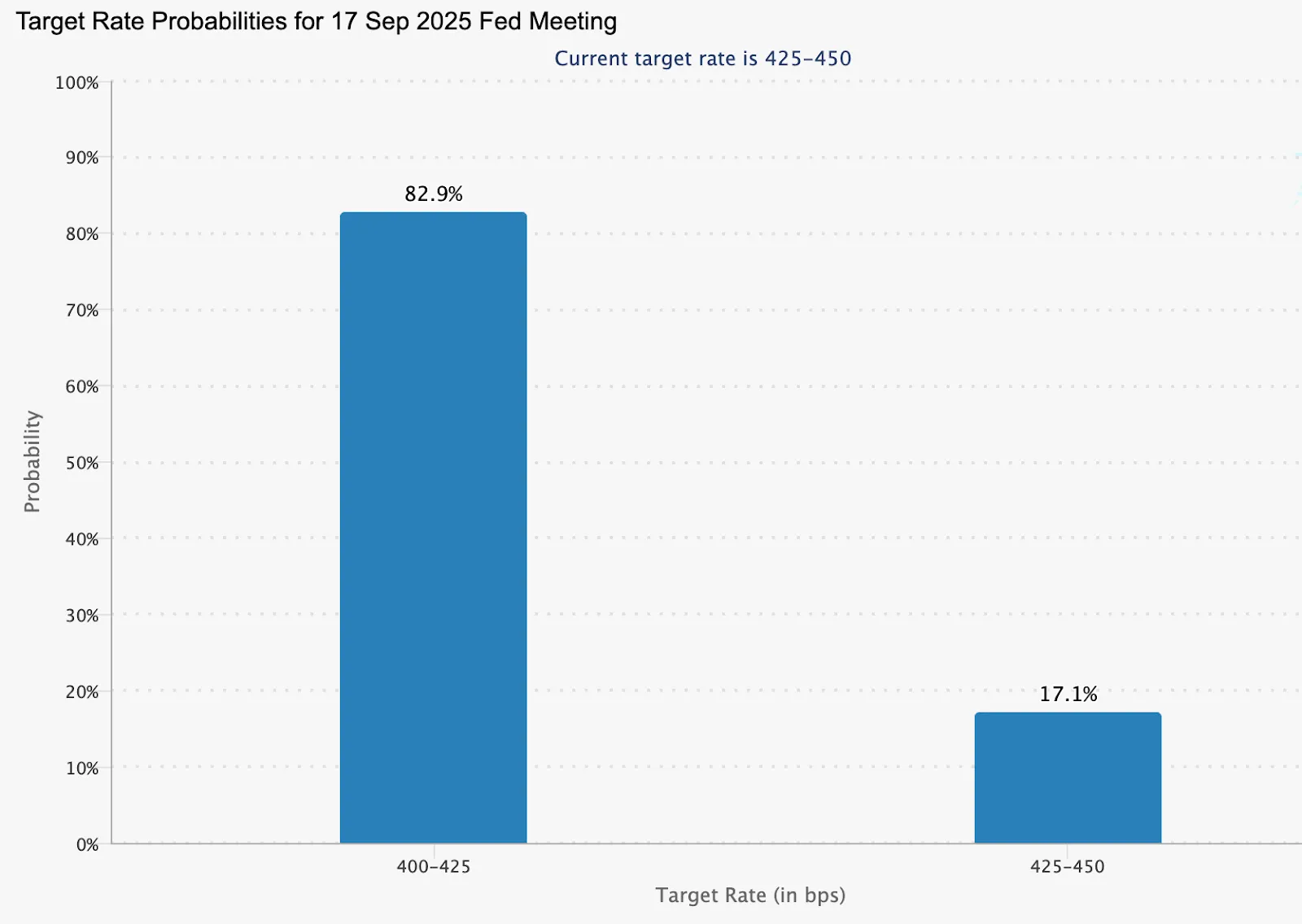

- Odds of a September Fed rate cut are 82.9%, down from 100% last week, reflecting tempered easing expectations.

- China added 60,000 oz in July, marking its ninth consecutive month of gold buying.

- Central banks collectively purchased 415 tonnes in H1 2025, down 21% year-on-year but still historically strong.

- Silver diverges from gold, with high prices discouraging coin sales but encouraging ETF inflows.

Fed policy exerts pressure on gold

The primary driver for gold in 2025 has been the Federal Reserve’s stance. Markets initially priced in two rate cuts this year, with the first expected in September, but stronger US data and sticky inflation have trimmed those expectations.

The CME FedWatch Tool shows an 82.9% probability of a September cut, down from 100% a week earlier.

Alt text: Bar chart showing Fed target rate probabilities for the 17 September 2025 meeting.

Source: CME

US housing data released this week added to the dollar’s strength, while the Fed’s July minutes are unlikely to provide clarity as they pre-date July jobs and CPI numbers. The immediate focus is on Jerome Powell’s upcoming remarks at the Jackson Hole Symposium. His guidance will be critical in determining whether gold stabilises or breaks lower.

Gold Safe haven appeal weakens

Gold’s reaction to geopolitical events has been subdued. Despite successful talks between US, EU, and Ukrainian leaders and discussions of a potential Putin-Zelenskiy meeting, gold has not rallied meaningfully. Similarly, President Trump’s decision to rule out ground troops in Ukraine - while suggesting possible air support - had little effect.

In previous years, such developments might have triggered a stronger bid for bullion. Now, with the threat of a trade war dissipating and tariffs largely removed from the equation, gold’s role as a safe haven appears diminished. Investors are watching the Fed more closely than they are global flashpoints.

Central bank gold purchases provide structural support

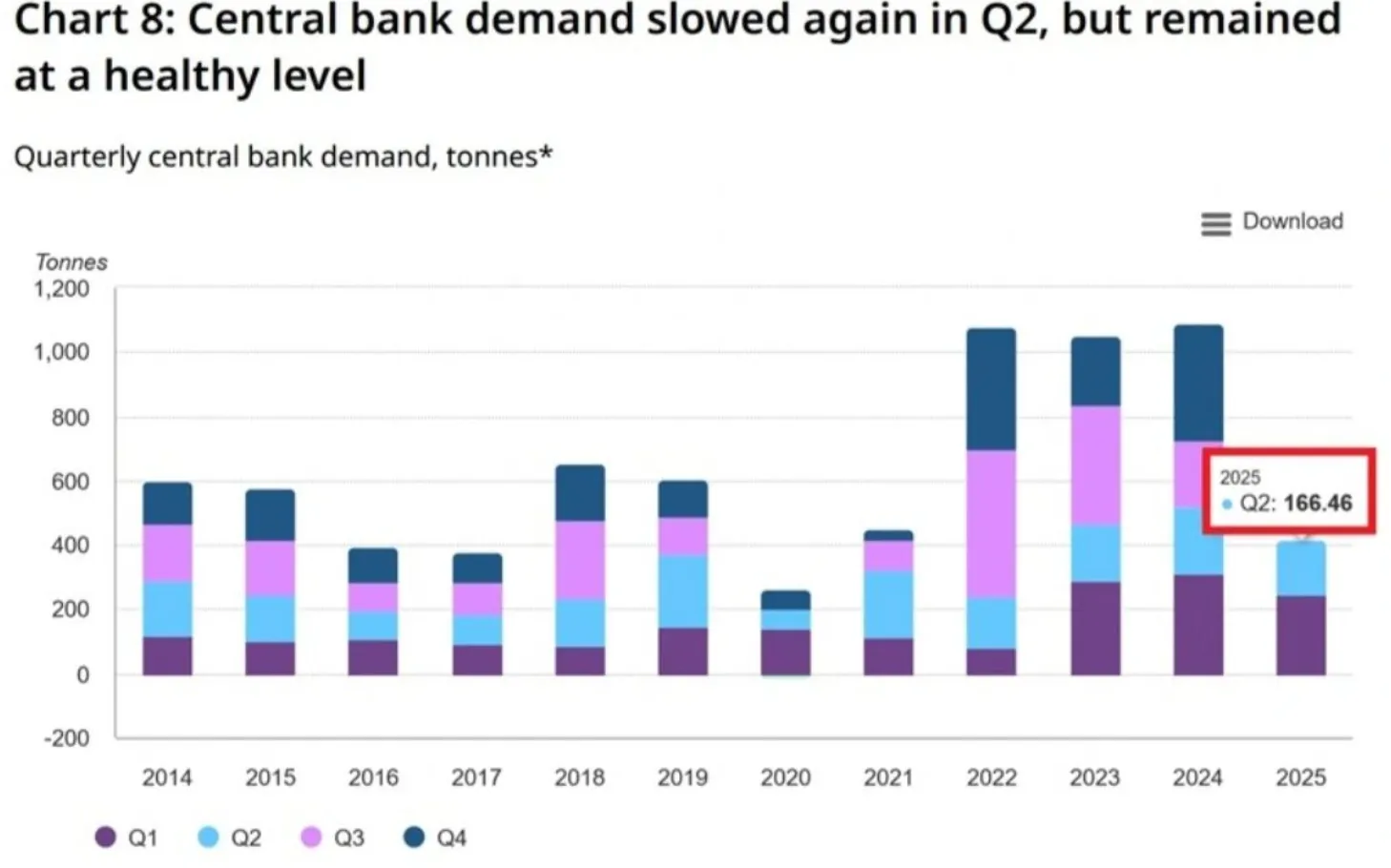

While short-term trading is dictated by Fed expectations, central banks continue to underpin gold demand. China’s central bank added 60,000 ounces in July, marking the ninth consecutive month of accumulation and bringing reserves to 73.96 million ounces.

Globally, central banks bought 166.5 tonnes in Q2 and 415 tonnes in H1 2025. Although this is 21% lower than last year’s record pace, it remains strong compared to historical norms.

Alt text: Stacked bar chart showing quarterly central bank gold demand in tonnes from 2014 to 2025.

Source: World Gold Council, Metals Focus

Refinery services provider Heraeus notes that gold is unaffected by US tariffs and has held steady in the face of global turbulence. The firm highlights that if the Fed does eventually cut rates, a weaker dollar could help gold prices recover.

Gold vs silver performance

Silver presents a contrasting picture. On 15 August, prices closed at $37.9/oz, near multi-month highs.

Alt text: Daily candlestick chart of Silver (XAG/USD) on TradingView from May to August 2025.

Source: TradingView

High prices have discouraged physical coin sales but boosted exchange-traded fund (ETF) inflows. This indicates that investors remain interested in exposure to silver but prefer financial instruments over physical purchases.

The divergence underscores a broader theme: while gold is increasingly policy-driven, silver is attracting demand through financial markets and industrial relevance, reshaping how each metal responds to macroeconomic conditions.

Gold price technical analysis

At the time of writing, gold is hovering around the $3,318 level after a notable downturn, with a death cross formation on the cards. This suggests the potential for a further downturn. However, the volume bars show dominant buy pressure, hinting at a possible upmove.

Alt text: Gold (XAU/USD) 4-hour candlestick chart with 50-day (orange) and 200-day (blue) moving averages, showing resistance levels at 3,345, 3,360, and 3,400.

Source: Deriv MT5

- If the death cross materialises, gold could see another leg down.

- If price action defies the looming formation, an uptick could target resistance at $3,345 and $3,360.

- A stronger rally would likely face a resistance wall near the $3,400 level.

Market impact and scenarios

- Bearish scenario: A confirmed death cross and break below $3,248 would signal a deeper trend change, reinforcing the Fed-driven bearish bias.

- Neutral scenario: Holding within the $3,282–$3,311 range would keep gold range-bound, awaiting Powell’s guidance and future inflation data.

- Bullish scenario: A dovish Fed shift or weakening dollar could trigger a rebound, supported by ongoing central bank buying.

Investment implications

For traders, gold’s technical setup highlights the $3,248–$3,400 zone as critical for near-term strategies. Short-term signals favour caution until Powell’s comments clarify the Fed’s direction.

For portfolio managers, gold is showing signs of an identity shift. Its safe-haven function is fading, with Fed policy cycles and central bank strategies increasingly dictating price action. While silver may offer more dynamic investor-driven opportunities, gold’s strategic role in central bank reserves ensures its long-term relevance.

Frequently asked questions

Why is the gold price under pressure?

Because the US dollar remains firm as the Fed resists aggressive rate cuts, reducing gold’s traditional safe-haven demand.

Is gold still a safe haven?

Recent muted reactions to geopolitical risks suggest gold is increasingly policy-driven rather than crisis-driven.

What role do central banks play?

They continue to accumulate gold, with China leading the way, providing long-term demand even as short-term momentum weakens.

How is silver behaving differently?

Silver’s high price has reduced coin sales but boosted ETF inflows, highlighting financial investor appetite.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.