AI lag and tariff risks challenge Apple stock despite potential Fed easing

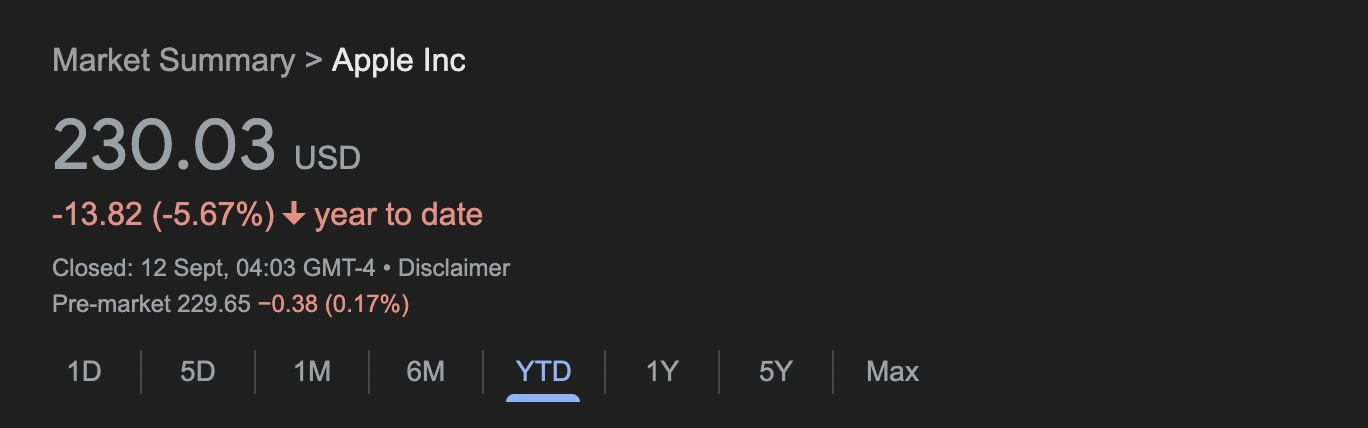

Apple stock has stalled near $230 as investors weigh the prospect of Federal Reserve rate cuts against concerns over tariffs, rising costs, and delays in artificial intelligence innovation. With technology stocks now commanding 37% of the S&P 500, Apple’s relative underperformance compared to peers highlights the risks of relying on monetary easing alone to lift the stock.

Key takeaways

- Apple has lost about 5.7% year-to-date, underperforming Nvidia, Microsoft, and the broader Nasdaq despite its $3.41 trillion valuation and ~5.7% weighting in the S&P 500.

- August CPI data showed headline inflation at 2.9% and core inflation at 3.1%, reinforcing expectations of a 25 bps Fed cut at the September FOMC.

- Rate cuts could support Apple’s balance sheet, cash returns, and services valuations, but product-cycle risks and tariff exposure remain.

- Analyst price targets for AAPL range from $200 (Phillip Securities) to $290 (Melius Research), reflecting the split between valuation caution and faith in services and design upgrades.

- Apple’s AI rollout, branded “Apple Intelligence,” is widely seen as lagging rivals like Google’s Gemini and Microsoft’s Copilot.

Tech’s concentration risk and Apple’s weight

The U.S. equity market has become more dependent on technology than at any point in history. The ten titan tech stocks now make up 38% of the S&P 500, surpassing the Dot-Com bubble’s 33% peak in 2000.

This weighting has doubled in just five years, largely driven by megacaps such as Nvidia, Microsoft, and Alphabet.

Apple alone accounts for nearly 6.8% of the index, making it both a bellwether and a vulnerability. While Nvidia has surged over 32% year-to-date on AI demand and Microsoft continues to rally on cloud and AI exposure, Apple stock has fallen 5.67% YTD, creating a sharp divergence within the so-called Magnificent Seven.

Macro backdrop: inflation and Fed policy

The August 2025 CPI report, released on 11 September, confirmed that inflation remains sticky but contained:

- Headline CPI rose to 2.9% YoY, the highest since January.

- Core CPI held at 3.1% YoY, with a 0.3% monthly increase driven by shelter and goods.

- Tariffs on imports pushed apparel prices higher (+0.2% YoY), groceries accelerated to 2.7% YoY, and electricity costs surged more than 6% YoY, partly due to AI data centre demand.

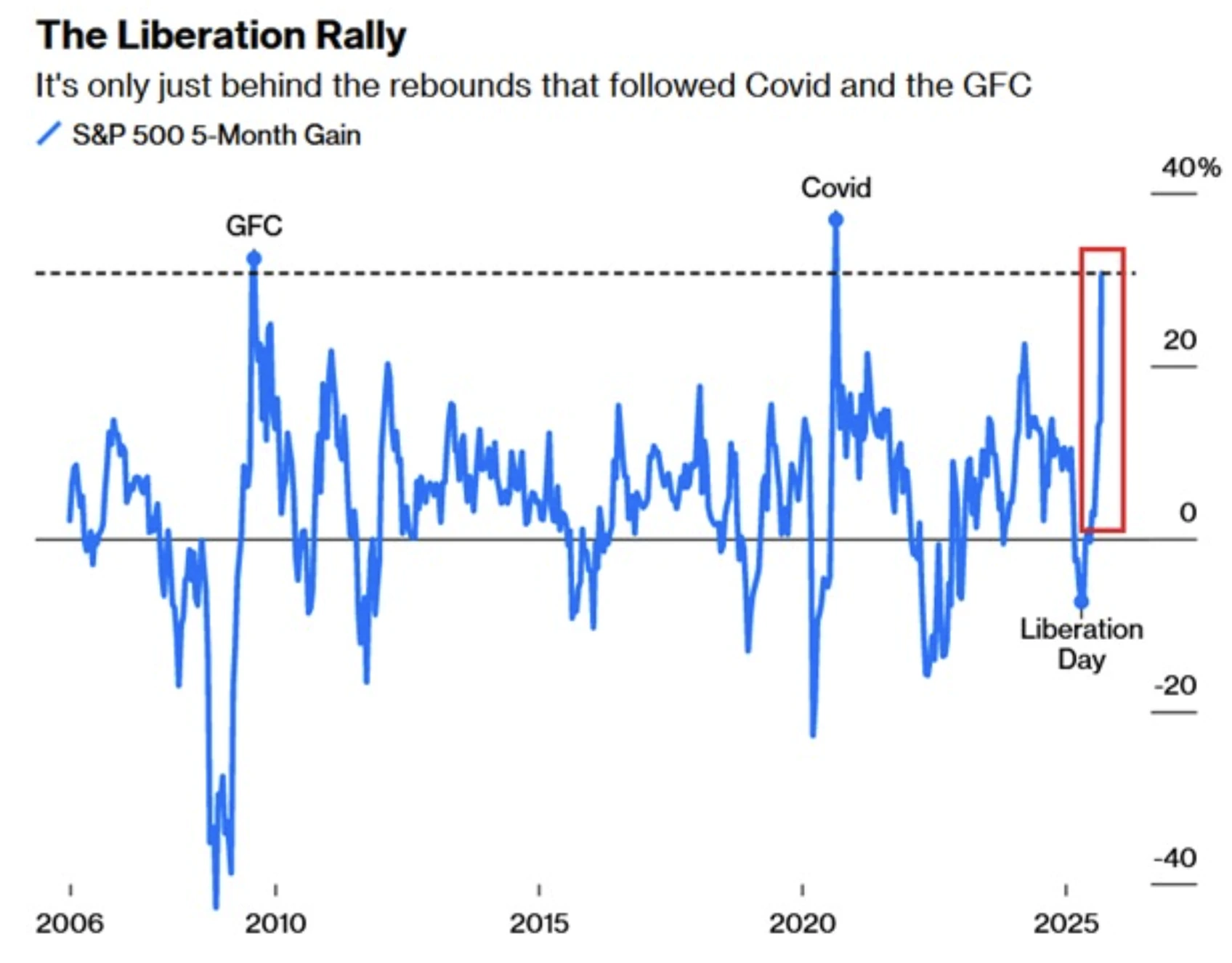

The S&P 500 has jumped 31% in five months, its third-biggest rally in 20 years - just one point shy of the post-2008 recovery.

The Nasdaq is up 0.7%, and the Dow is surpassing 46,000 for the first time. Futures now price in a 92.5% probability of a 25 bps Fed cut at the September 17–18 FOMC meeting.

For Apple, Fed easing could provide three benefits:

- Balance sheet strength: Lower rates support Apple’s $100B+ buyback and dividend programme.

- Valuation uplift: Discount rates on service earnings fall, raising their present value.

- Market momentum: Broad-based tech rallies may help Apple’s stock even if its fundamentals lag.

But while the Fed can provide liquidity and support, it cannot solve Apple’s structural innovation gap.

iPhone Air features: Apple shares post-event

Apple’s September product launch introduced four new handsets - iPhone Air, iPhone 17, iPhone 17 Pro, and iPhone 17 Pro Max. The iPhone Air, at 5.6 mm, is the slimmest iPhone ever and thinner than Samsung’s S25 Edge. It features:

- A19 Pro processor chip optimised for AI tasks.

- Two new custom communications chips.

- Titanium frame and ceramic shield glass for durability.

Analysts praised the Air as Apple’s first major design shift in eight years, with potential to drive upgrades in the next 12 months. However, it comes with trade-offs:

- Only one rear camera, compared with two on the base iPhone 17 and three on Pro models.

- eSIM-only design, problematic in China, where eSIMs face regulatory hurdles.

- Questions about whether Apple’s “all-day battery life” claim holds up in practice.

Despite consumer enthusiasm - early reviews praised the form factor - Apple shares fell 3% post-event, reflecting investor concerns about pricing, tariffs, and AI competitiveness.

Apple AI lag and competitive pressure

Apple’s cautious approach to artificial intelligence remains a sticking point. Its “Apple Intelligence” features have been criticised for trailing Google’s Gemini and Microsoft’s AI ecosystem. Nvidia’s explosive performance highlights the premium investors now place on AI leadership - a trend from which Apple has yet to benefit.

This is not just about perception: AI delays could undermine Apple’s services growth and user engagement, areas that underpin bullish analyst forecasts. Without credible AI differentiation, Apple risks being seen as a premium hardware company in a software-driven market.

Apple stock performance analyst outlook

Apple’s valuation debate is one of the sharpest among megacaps:

- Phillip Securities: Reduce, $200 target, citing overvaluation and lack of AI breakthroughs.

- UBS: Neutral, $220 target, acknowledging enthusiasm for iPhone Air but cautious overall.

- Rosenblatt: Neutral, raised target from $223 to $241, noting camera and battery improvements.

- TD Cowen: Buy, $275 target, highlighting design innovation and custom chips.

- BofA Securities: Buy, raised target from $260 to $270, citing ecosystem health features.

- Melius Research: Buy, raised target from $260 to $290, citing services growth and reduced tariff risks.

The result: price targets spanning $200–$290, reflecting deep uncertainty over whether Apple is a growth play, a value trap, or a stabiliser in a concentrated market.

Risks and scenarios for Apple investors

- Bull case: Fed easing supports valuations, iPhone Air drives upgrades, services continue double-digit growth, and AI features improve gradually.

- Bear case: Tariffs and inflation squeeze margins, AI strategy falls further behind, and China sales weaken, leaving Apple vulnerable to underperformance.

- Market-wide risk: With Apple at - 7% of the S&P 500, prolonged stagnation could weigh on index performance, exposing the fragility of tech’s 37% weighting.

Technical analysis of Apple stock levels

At the time of writing, Apple stock is seeing a modest recovery after a three-day step down, hovering near a key support level. This price action suggests a possible bounce as tech stocks continue to dominate the S&P 500.

- Volume analysis: Recent trading sessions show buy pressure dominating, reinforcing the bullish case.

- Upside scenario: If momentum holds, Apple stock could target the $240.00 resistance level.

- Downside scenario: If sellers reassert control, the stock may first retest the $226.00 support, with a further move lower opening room towards the $202.00 support.

This technical picture reflects the market’s broader indecision: short-term bullish signals offset by longer-term risks tied to macro and competitive headwinds.

Investment implications

Apple’s trajectory in late 2025 depends on whether macro support from Fed easing can outweigh micro-level challenges. The stock’s $3.5 trillion valuation makes it too big to ignore, but analysts remain split on whether it can keep pace with AI leaders. Investors face a choice: treat Apple as a stable cash-return giant benefiting from Fed cuts, or recognise it as the weak link in tech’s concentrated market dominance.

Speculate on Apple's next moves with a Deriv MT5 account today.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.