Oil price forecast: Can record hedge fund shorts push WTI below $55?

.png)

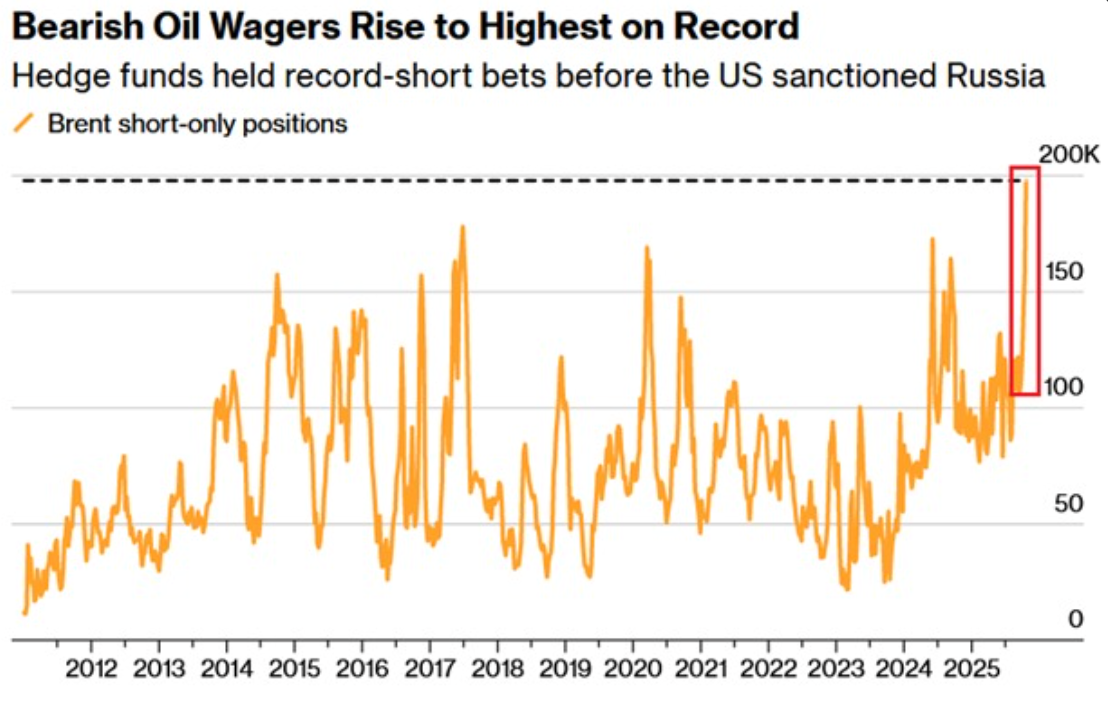

According to analysts, WTI crude could slide toward $55 per barrel as hedge funds pile into record short positions and oversupply fears dominate the market. Short calls on Brent surged by 40,233 contracts in the week ending 21 October, bringing total bearish positions to 197,868 - the most on record.

This marks the third consecutive weekly increase and a doubling of short exposure in just three months. Institutional traders are signalling a clear message: supply is rising faster than demand, OPEC+ is pumping more barrels, and global demand remains too weak to absorb the excess.

Still, with fresh U.S. sanctions on Russian oil and OPEC production politics adding new variables, short-covering rallies back toward $65 per barrel remain possible. The battle between macro fundamentals and geopolitical risk continues to define oil’s volatile range.

Key takeaways

- Record hedge-fund shorts: Brent and WTI short positions have doubled since July, signalling broad institutional pessimism.

- Short-term volatility: U.S. sanctions on Russia lifted Brent +10% in a week, but analysts expect the effect to fade.

- Bearish fundamentals: Rising OPEC output, record U.S. supply, and weak demand point to continued downside pressure.

- Structural shift: U.S. shale costs are climbing, setting the stage for longer-term tightening once oversupply eases.

- Price risk: If oversupply persists, WTI could test $55, though a short-covering rally toward $65 remains possible.

Hedge fund oil trading takes control of the narrative

Speculative funds are now at their most bearish on record. In the week ending 21 October, short positions in Brent futures surged by over 40,000 contracts, marking the third consecutive weekly increase. This sharp rise suggests confidence that near-term fundamentals - particularly oversupply and weak demand - will push prices lower.

By comparison, short-only positions stood at just 26,000 contracts a year ago. The current build-up mirrors the mid-2018 and 2020 oil corrections, when rising inventories and a strong U.S. dollar fuelled steep sell-offs.

OPEC oil production increases are overwhelming the market

Oil prices rallied nearly 8% last week after the U.S. announced sanctions on Russia’s Rosneft and Lukoil, but quickly lost steam as OPEC signalled more output ahead. Eight member states are backing another production hike in November, roughly 137,000 bpd, as Saudi Arabia leads an effort to reclaim market share.

This deliberate oversupply strategy aims to undercut higher-cost U.S. producers while keeping a lid on global prices. With both OPEC+ and non-OPEC producers such as the U.S., Brazil, and Canada expanding supply, the market remains saturated despite geopolitical tension.

Demand weakness compounds the pressure

Analysts from Standard Chartered cut their 2026–2027 oil price forecasts by $15 per barrel, citing a shift to contango - where futures prices exceed spot prices, signalling near-term softness.

Global demand growth has slowed as trade frictions and tariff uncertainty weigh on consumption. The International Energy Agency and S&P Global both expect oil to dip below $60 early next year as oversupply persists.

Even with record refining runs, estimated above 85 million bpd, the market may not be able to absorb the extra barrels.

Geopolitical shocks can still spark short-covering rallies

The short trade is not risk-free. The Trump administration’s sanctions on Russia drove a brief 10% rally, showing how exposed shorts are to policy moves.

If tensions in Ukraine, Iran, or China–U.S. trade talks escalate, supply disruptions could trigger a short-covering surge, temporarily driving WTI back above $65.

Still, analysts expect such rallies to fade quickly as long as U.S. production remains strong and OPEC continues to loosen output controls.

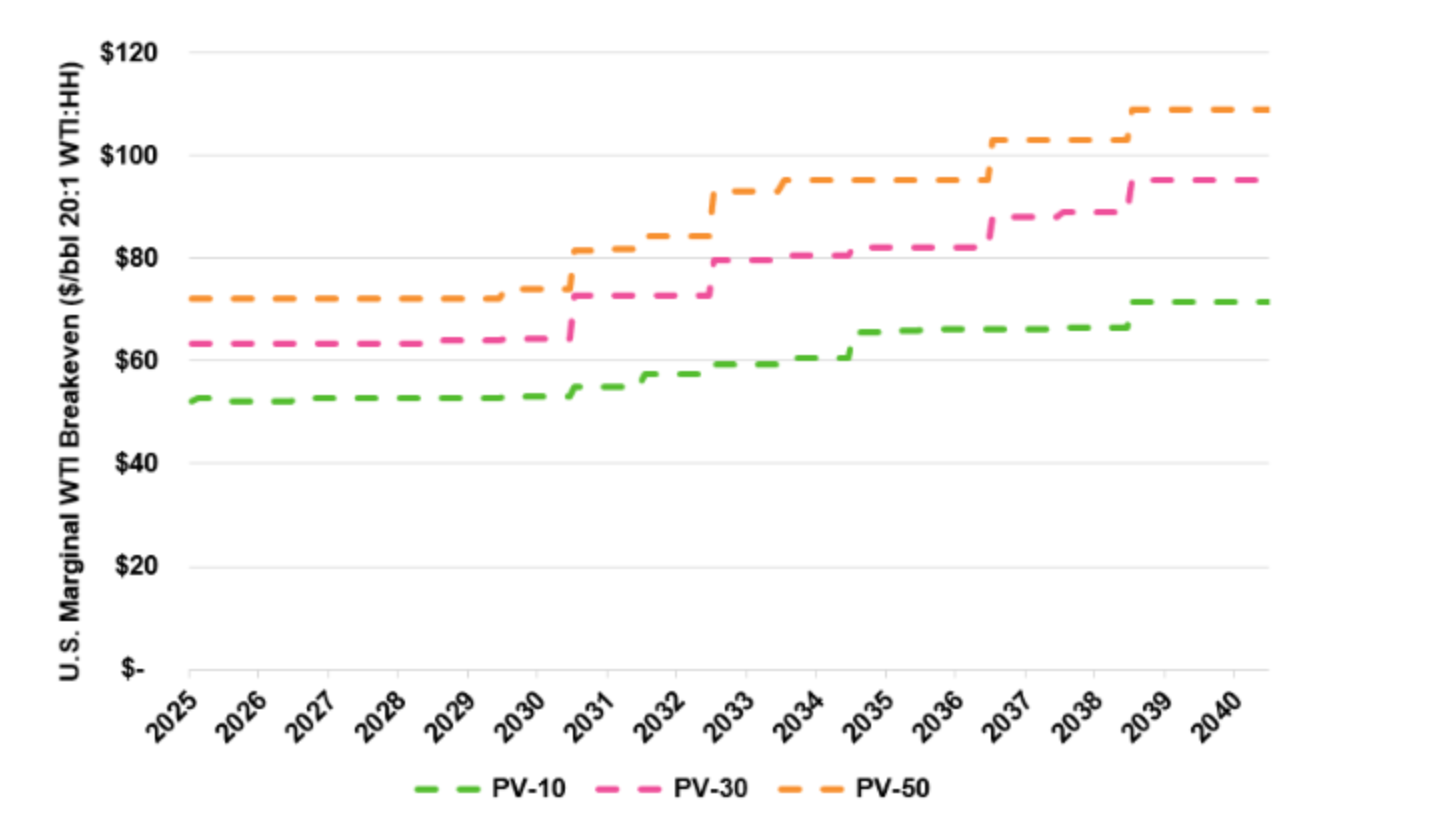

The structural story: rising shale costs and long-term tightness

While the near-term trend is bearish, the cost base of U.S. shale is climbing. Enverus analysts project that marginal production costs could rise from $70 to $95 per barrel by the mid-2030s as producers exhaust their most efficient wells.

This implies that if prices fall too far, supply could contract sharply, setting the stage for future tightness once demand stabilises.

WTI crude oil price prediction: Market impact and price scenarios

If current dynamics persist, analysts see Brent testing $60 and WTI near $55 by early 2026. However, a shift in positioning - such as hedge-fund short-covering or renewed sanctions risk - could trigger rebounds toward $65–$70. For now, the balance of risk remains skewed lower as supply continues to exceed demand.

Commodities traders tracking these scenarios often rely on Deriv’s trading calculator to manage position sizes and evaluate exposure in volatile markets.

Oil price technical insights

Oil is hovering near the upper Bollinger Band on Deriv MT5 following a rebound from recent lows - signalling fading bearish momentum and a potential short-term continuation higher.

The RSI is climbing slowly around the midline, suggesting improving buying pressure but no overbought conditions yet. Key resistance levels sit at 62.35 and 65.00, where profit-taking could emerge. On the downside, 56.85 remains a crucial support - a break below it may trigger renewed selling pressure.

Oil Price investment implications

The current setup suggests heightened downside risk over the medium term for traders and portfolio managers. If volatility spikes, short-term strategies may favour tactical buying near support levels around $61–$62. However, medium-term positioning should reflect the bearish demand outlook and the likelihood of prolonged oversupply.

Energy equities with low-cost production and strong balance sheets - particularly U.S. shale and Middle Eastern producers - could outperform, while high-cost offshore and frontier projects may struggle. Refiners, meanwhile, stand to benefit from strong margins even in a lower-price environment.

The performance figures quoted are not a guarantee of future performance.