Why metals are surging again as Fed uncertainty deepens

%20(1).png)

Metals are surging again because investors are grappling with a Federal Reserve that is signalling caution rather than conviction. November’s US labour data showed unemployment rising to 4.6%, the highest level since 2021, while job creation slowed sharply compared with earlier in the year. Yet inflation remains elevated enough to keep policymakers hesitant. That mix of slowing growth and unresolved price pressures has reignited demand for precious metals as a hedge against policy uncertainty.

Silver’s rally to record highs near $66.50 per ounce and platinum’s sharp breakout above long-term resistance reflect more than speculative enthusiasm. Markets are increasingly pricing US rate cuts in 2026, real yields are drifting lower, and physical supply constraints are tightening. With investors awaiting fresh inflation signals from the Consumer Price Index, metals have once again become a barometer of confidence in the global monetary outlook.

What’s driving the metals rally?

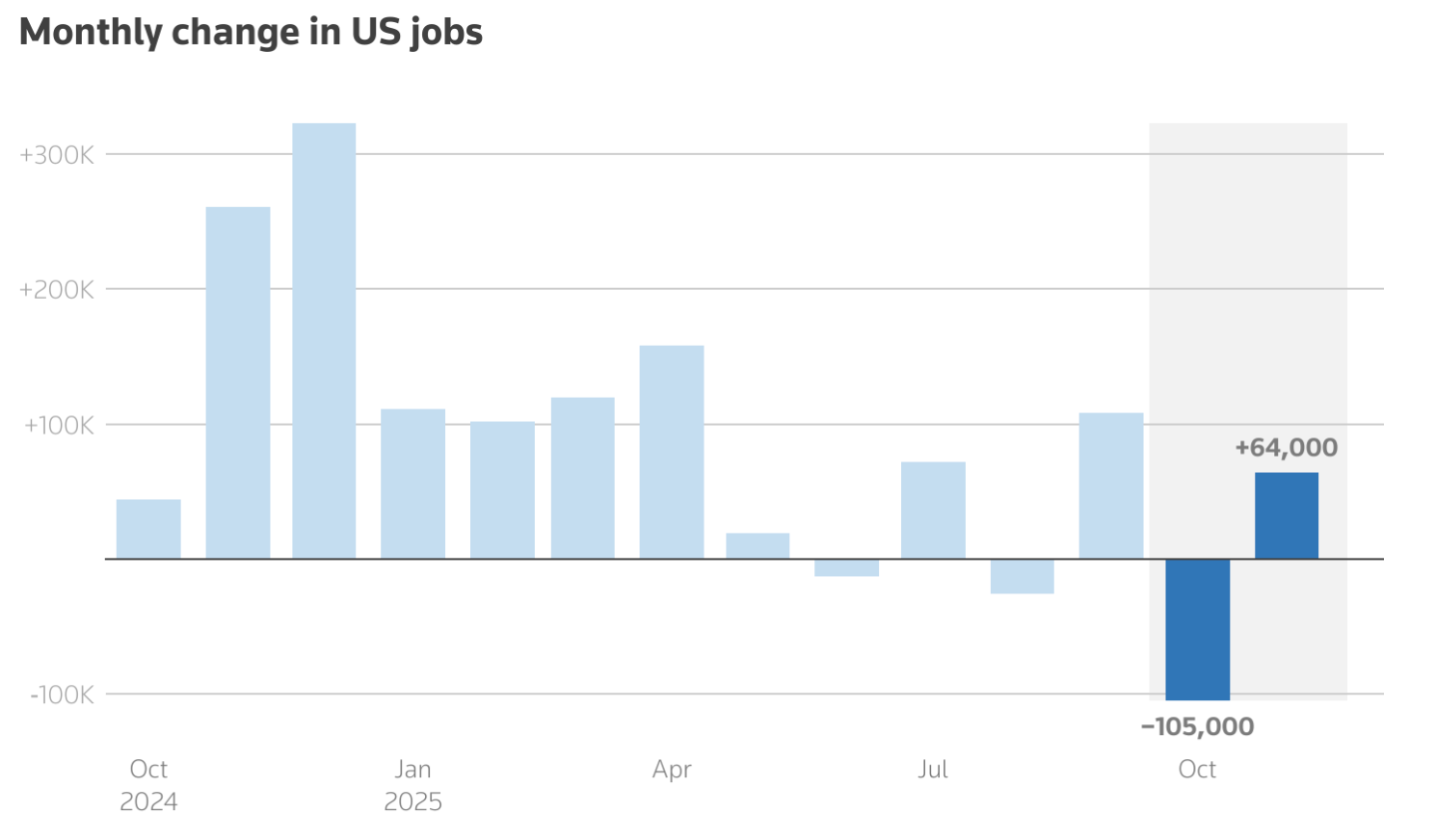

The immediate catalyst behind the renewed surge in metals is uncertainty over the direction and timing of US monetary policy. The latest Non-Farm Payrolls report confirmed that the labour market is cooling, but not collapsing. Payrolls grew by only 64,000 in November, while prior months were revised lower, reinforcing the idea that economic momentum is fading.

At the same time, inflation has not slowed quickly enough to give the Fed room for decisive easing. That ambiguity has left markets in limbo. Fed Governor Christopher Waller recently stated that US borrowing costs could eventually be up to one percentage point lower if the labour market softens, prompting traders to price in two rate cuts in 2026. Lower expected rates tend to weaken real yields, which directly improves the relative appeal of non-yielding assets such as gold and silver.

Supply dynamics are amplifying the move. Silver is heading into its fifth consecutive annual market deficit, driven by robust industrial demand from solar panels, electric vehicles, and data centres. Inventories are already tight, meaning that even modest shifts in investment flows can have a significant impact on prices.

Why it matters

The rally in metals matters because it reflects a deeper re-pricing of risk across financial markets, according to analysts. Investors are no longer positioning themselves purely for growth or recession, but rather for a prolonged period of economic uncertainty where inflation, interest rates, and growth fail to move in tandem. In that environment, metals regain their traditional role as stores of value rather than being used as tactical trades.

Platinum’s resurgence is particularly revealing. Often overshadowed by gold and silver, platinum is now benefiting from structural supply shortages. The World Platinum Investment Council expects a deficit of several hundred thousand ounces in 2025, marking the third consecutive year of undersupply.

As one market analyst observed, “low elasticity in recycling, limited reinvestment at the mine level, and persistent production constraints are making future supply risks harder to ignore.” This suggests the current move resembles a re-rating rather than a short-lived spike.

Impact on markets and investors

For investors, the metals rally is reshaping portfolio dynamics. Gold continues to anchor defensive allocations, supported by central bank buying and geopolitical uncertainty. Silver, however, has taken on a more complex role. Its price now reflects both safe-haven demand and expectations that industrial consumption will remain resilient even if global growth slows.

Platinum’s advance adds another layer to the story. South Africa, which accounts for between 70% and 80% of global platinum production, has faced repeated mining disruptions that have constrained output. At the same time, exports to China have been strong, and the launch of platinum futures on the Guangzhou Futures Exchange has increased confidence in long-term demand from Asia.

There are also signs of stress in physical markets. Financial institutions have reportedly been moving metal inventories to the United States to hedge against tariff risks, while the London market is showing signs of tightening. These shifts underscore the growing influence of geopolitical fragmentation and supply-chain security on commodity pricing.

Expert outlook

Looking beyond the near-term data cycle, Deriv expert Vince Stanzione argues that the broader bull case for precious metals remains firmly intact as we head into 2026.

After what he describes as a “blockbuster” 2025 - with gold rising roughly 60% to around $4,200 per ounce and silver gaining close to 80% on strong industrial demand - momentum has carried into the new year. In his view, the rally is unlikely to repeat those extremes, but still has room to run.

Stanzione forecasts further double-digit gains, projecting gold to rise 20-25% and silver 25-30% in 2026, comfortably outperforming equities, where expected returns for the S&P 500 sit closer to 3-5% as valuations stretch. He cautions that sharp pullbacks are likely along the way, but stresses that the dominant trend remains upward as investors continue to seek protection from policy uncertainty and currency debasement.

The structural case rests heavily on central bank behaviour. According to Stanzione, official institutions added more than 1,000 tonnes of gold to reserves in 2025, led by the People’s Bank of China and the Reserve Bank of India, with a further 800-900 tonnes potentially coming in 2026 as diversification away from the US dollar accelerates. China alone has experienced a steady thirteen-month buying streak since late 2022, followed by a brief pause in May 2024.

Silver’s outlook is reinforced by its dual role as a monetary hedge and industrial input, with demand from solar panels and electric vehicles expected to outpace mined supply, further tightening inventories.

Stanzione also highlights gold miners as a leveraged way to express the metals theme. Despite a strong 2025, valuations remain compressed. Newmont Corporation, the world’s largest gold producer, trades on a forward price-to-earnings ratio well below the broader market, supported by low production costs and strong free cash flow.

Historically, he notes, a 10% move in gold prices has translated into roughly 25-30% earnings growth for miners, although risks such as a stronger US dollar or weaker Chinese demand could temper gains.

Monthly price chart of Newmont Corporation (NEM) from 1997 to November 2025

On platinum and palladium, Stanzione remains constructive but selective. Both metals experienced solid gains in 2025 and benefited from industrial demand, particularly in catalytic converters, yet remain well below their previous peaks. While smaller and more volatile than gold and silver, they remain worth monitoring as potential catch-up trades if supply constraints persist. To read more on how to trade commodities, read this free ebook exclusively published by Deriv.

Key takeaway

Metals are surging again because markets are adjusting to a world where monetary policy clarity is absent and economic risks are uneven. Silver’s record highs and platinum’s rapid catch-up point to tightening supply and renewed defensive positioning. With inflation data and Fed signals still pulling markets in different directions, metals remain a critical hedge and indicator. The next CPI release may shape short-term price action, but the broader trend appears increasingly durable.

Silver technical insights

Silver remains firmly in an uptrend, with price holding near the upper Bollinger Band, signalling strong bullish momentum. However, the RSI has pushed well into overbought territory, increasing the risk of short-term consolidation or profit-taking.

On the downside, $50.00 is the first key support, followed by $46.93, where a break could trigger sell-side liquidations and a deeper corrective move. As long as silver holds above $50, the broader bullish structure remains intact, though upside gains may slow without a pullback.

The performance figures quoted are not a guarantee of future performance.