US indices outlook brightens as Greenland tensions ease

US stock indices showed signs of stabilisation this week as Wall Street bounced from a recent sell-off, driven largely by a sudden de-escalation in geopolitical risk tied to tensions over Greenland.

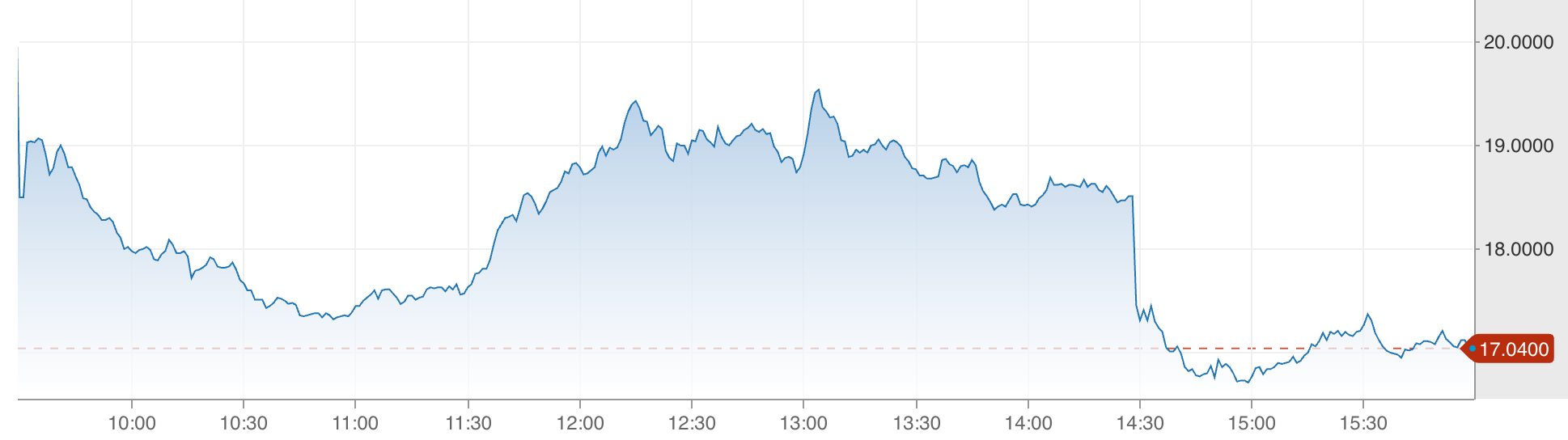

The S&P 500 climbed about 1.2% to roughly 6,875, while the Dow Jones Industrial Average and Nasdaq Composite each rose by similar margins during Wednesday’s session as traders digested President Trump’s rollback of tariff threats.

The relief rally lifted futures late into the evening, signalling that markets may be positioned for a more constructive phase as the calendar turns toward key inflation data and a packed earnings schedule. With broader macro risks still in play, investors are now looking beyond yesterday’s headlines to the indicators that will shape the next leg of the market’s trajectory.

What’s driving the market outlook?

What began as a sharp risk-off move earlier in the week reversed quickly after President Trump clarified that he would not impose the planned tariffs on European trading partners tied to his controversial push for Greenland.

Trump’s comments at the World Economic Forum in Davos, where he outlined a so-called “framework” for a future understanding with NATO, reassured market participants that a broader trade conflict might be avoided.

Investors had grown anxious after Trump’s earlier threats to escalate tariffs on multiple European nations, which sent index futures sliding and gold prices higher as traders sought safe havens. The pivot toward diplomacy, even if still lacking detail, lessened immediate tail risks and invited dip-buying, which helped the S&P 500 and Nasdaq recover substantial ground.

But the backdrop remains complex. Markets are simultaneously bracing for a key personal consumption expenditures (PCE) inflation reading - the Federal Reserve’s preferred gauge - and a slate of heavyweight earnings reports. Traders are acutely aware that macro signals and corporate performance will determine whether current gains stick or simply mark a short-lived relief bounce.

Why this matters to investors

The turnaround in sentiment speaks to how sensitive equities have become to policy swings and risk perceptions. When tariff threats loomed, risk assets weakened sharply, with the Dow Jones Industrial Average posting notable point losses and the CBOE Volatility Index spiking as fear gripped markets. The subsequent pullback underscores how quickly positioning can unwind when geopolitical uncertainty evaporates.

Relief rallies like this one often reveal deeper undercurrents about investor psychology, according to analysts. Broad participation across major indices - from the Russell 2000 small-cap gauge to large-cap tech stocks - suggests that traders are willing to re-engage with risk, but only in the context of clearer macro direction and reduced headline shock. Analysts pointed out that what matters now is not just the absence of conflict, but the active presence of data that supports sustained economic growth.

Sentiment is also being shaped by the broader macro calendar. With inflation metrics and earnings from bellwether companies approaching, the narrative has shifted from pure geopolitical risk to whether the real economy aligns with lofty market valuations. In this environment, soft inflation data or stronger-than-expected earnings could further buoy indices, while the opposite could quickly tighten financial conditions.

Impact on markets and strategic positioning

The easing of tensions over Greenland has important implications for sector rotation and investor strategy. Financials and energy stocks, which bore the brunt of earlier risk-off positioning, recovered as bonds stabilised and yields retreated modestly. Meanwhile, technology stocks, although rallying, showed a more measured advance - suggesting that traders are not simply chasing growth irrespective of fundamentals.

Sector dynamics offer clues about market confidence. Value-oriented areas responding well to reduced geopolitical risk indicate that expectations of an economic soft landing remain alive, even amid inflation concerns and central bank vigilance. If macro data continues to support resilient spending and earnings, this could validate the current rebound and encourage more durable flows into cyclical exposures.

However, the relief rally does not erase fragility. Indices remain mixed on a weekly basis with the S&P 500, Dow, and Nasdaq still lower over recent sessions despite Wednesday’s bounce. This dichotomy shows that while headline risks can abate quickly, structural concerns like inflation, rate expectations, and profit margins still warrant close scrutiny.

Expert outlook

Looking ahead, the market narrative is set to pivot toward several critical gauges. The forthcoming PCE inflation print will be one of the most consequential data points for the Federal Reserve’s rate outlook. A cooler-than-expected reading could embolden risk appetite; a hotter print might strengthen hawkish sentiment and curb equity gains.

Earnings seasons provide another pivotal catalyst. With results due from household names across tech, consumer staples and industrials, investors will be assessing not just top-line performance but guidance. In an environment where “beat and raise” results have had muted impact on stock prices, future earnings surprises must translate into credible forward narratives to sustain upside.

Strategists caution that volatility remains an active risk. Geopolitical headlines can flip sentiment swiftly, and macro releases will have outsized influence as volatility continues to ebb and flow around news events. For traders and long-term investors alike, adaptability and attention to incoming data will be key in navigating the evolving outlook.

Key takeaway

Sentiment on Wall Street improved sharply as geopolitical tensions tied to Greenland eased, supporting a broad-based rebound in major US indices. Yet, the market’s forward trajectory hinges on macroeconomic data and corporate performance, not just headline risk reductions. Traders should watch inflation indicators and earnings reports closely as they will shape market leadership and volatility in the weeks ahead.

The information contained on the Deriv Blog is for educational purposes only and is not intended as financial or investment advice. The information may become outdated, and some products or platforms mentioned may no longer be offered. We recommend you do your own research before making any trading decisions." is present