Can Nvidia’s stock keep climbing after its 4 trillion milestone?

.webp)

Note: As of August 2025, we no longer offer the Deriv X platform.

Nvidia has just done the unthinkable - hit a four trillion dollar market valuation. That’s not just impressive; it’s historic. It’s bigger than the entire UK stock market and more valuable than France and Germany’s combined. And yet, with shares hovering around $163, the question on every investor’s mind is simple: Can it go higher?

With AI booming, earnings soaring, and Wall Street buzzing, Nvidia looks unstoppable. But in markets, what goes up doesn’t always keep going. So, is $180 just around the corner?

Nvidia AI chip demand: The case for more upside

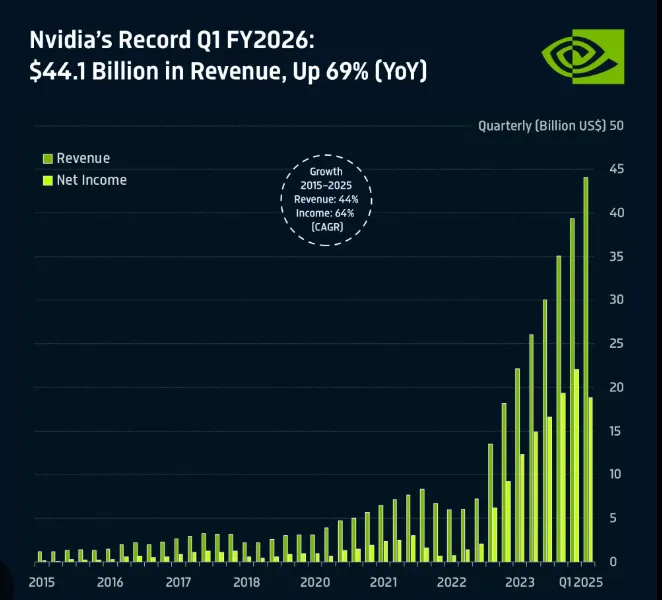

There’s no doubt Nvidia’s rise is rooted in fundamentals. First-quarter revenue surged 69% to $44.1 billion, and analysts are forecasting a blowout 2025: $200 billion in sales, $100 billion-plus in net income, and margins brushing up against 70%.

Not bad for a company that was worth just $144 billion six years ago. The real tailwind? AI. Nvidia’s chips are powering everything from OpenAI’s training clusters to smart factories in China.

Big names like Microsoft and Amazon are throwing money at AI infrastructure, and Nvidia remains the preferred supplier. No surprise, then, that CFRA’s Angelo Zino has a $196 price target, suggesting a market cap of nearly $4.8 trillion could be on the cards.

If Nvidia’s earnings, set for 27 August, meet expectations, some think the stock could easily add $10-$20 in a matter of days. With bullish chatter heating up on X (formerly Twitter) and the stock holding a hefty 7.5% weight in the S&P 500, the FOMO effect could well take hold, pushing the price closer to that $180–$200 zone, according to analysts.

Nvidia earnings forecast

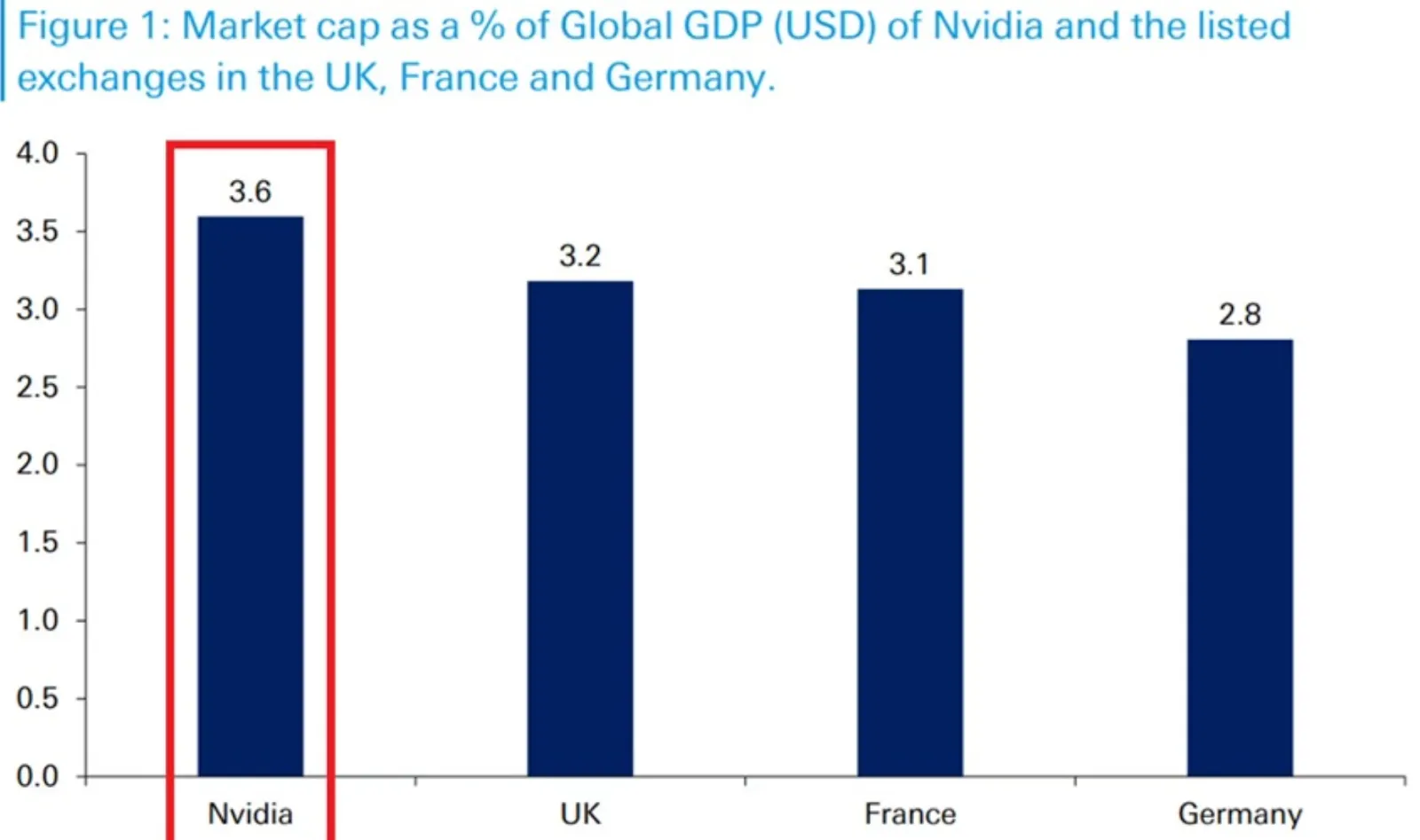

To grasp just how far Nvidia has come, it’s worth revisiting the dot-com days. At its peak in 2000, Cisco’s valuation reached $550 billion, equivalent to 1.6% of global GDP. Nvidia now commands 3.6%. That’s not a typo.

And yet, comparing market cap to GDP has its critics. GDP is an annual flow of goods and services, and market cap is a snapshot of future expectations. As some analysts on X rightly note, it’s not quite apples to apples.

Still, others point to Nvidia’s projected net income of $153 billion in three years, nearly matching the entire FTSE 100. Now that’s a comparison worth chewing on.

What could go wrong?

Of course, no stock climbs forever. Nvidia’s forward price-to-earnings ratio may be sitting at a “reasonable” 33 (below its 5-year average of 41), but it’s still pricing in a whole lot of perfection. Any wobble, whether in earnings, AI spending, or global chip demand, could knock the wind out of its sails, according to analysts.

There’s also the thorny issue of geopolitics. Nvidia relies heavily on Taiwan for chip production, and escalating US-China tensions pose real risks. Add in the possibility of fresh export controls or tariffs, and supply disruptions could become more than just a headline risk.

Then there’s the trading dynamic. With only a 0.02% dividend yield and plenty of leveraged exposure in the market, any spike in interest rates or bout of margin selling could cause a sharp pullback. Let’s not forget: Nvidia lost nearly $600 billion in value earlier this year after DeepSeek’s surprise AI model announcement spooked the market.

Nvidia price Short-term outlook: $150 or $185 next?

According to analysts, in the next month or two, Nvidia’s price could swing between $150 and $185. A strong August earnings report could see it take out recent highs and test $180, while a miss - or a geopolitical curveball - could knock it back below $150.

Looking further out, the path diverges. If AI adoption continues to explode and Nvidia stays ahead of rivals like AMD, we could be talking $200–$250 by year-end. But if macro conditions tighten or competitors gain ground, a retrace to $125–$140 isn’t out of the question.

Nvidia’s $4 trillion milestone isn’t just about valuation - it’s a statement. A signal that the market believes AI isn’t hype, but a full-blown economic revolution. Still, even revolutions face resistance.

According to experts, whether Nvidia breaks through to $180 and beyond will depend on earnings, sentiment, and a healthy dose of geopolitical luck. For now, the stock may be flying high, but it’s not immune to gravity.

At the time of writing, we are seeing a slight pullback from record highs, indicating that sellers are offering some pushback which could lead to a significant drawdown. However, the volume bars paint a picture of near-even buy and sell pressure - hinting at potential consolidation. The $167.74 price is a potential resistance level if prices tick upwards. Conversely, should we see a crash, prices could find support floors at the $162.61, $141.85 and $116.26 support levels.

Disclaimer:

The performance figures quoted are not a guarantee of future performance.