Il trilemma del 2024: Inflazione, stagflazione o atterraggio morbido

Dimentica le sfere di cristallo; il successo nel 2024 dipende dalla capacità di navigare in un panorama in cambiamento plasmato da politiche monetarie inasprite e dinamiche di potere in evoluzione nel 2023.

Mentre uno scenario di base dipinge un quadro di crescita graduale, correnti nascoste di rischio e opportunità si agitano proprio sotto la superficie. Questa prospettiva per il 2024 analizza le tendenze e le sfide chiave che gli investitori di mercato possono affrontare per sbloccare il potenziale successo nel prossimo anno.

USA: Atterraggio morbido, ma attenzione ai venti favorevoli all'inflazione

I risparmi in eccesso dei consumatori stanno diminuendo e i tassi d'interesse più elevati stanno incidendo sulla domanda di beni, servizi e case. Mentre ci si aspetta un temporaneo indebolimento della crescita trimestrale del Prodotto Interno Lordo (PIL) degli Stati Uniti all'inizio del 2024, non si prevede una recessione totale da un insieme più ampio di analisti economici.

La Federal Reserve prevede una continua moderazione dell'inflazione generale e una crescita economica più lenta nel 2024 prima di raggiungere il suo obiettivo del 2% dell'Indice dei Prezzi al Consumo (CPI) entro il quarto trimestre del 2026.

La Federal Reserve, mentre pratica un delicato equilibrio, osserva sia la crescita rallentata che l'inflazione persistente. La loro recente pausa sugli aumenti dei tassi suggerisce un riconoscimento della lentezza, allineandosi con le letture fondamentali della spesa per consumi personali (PCE) che potrebbero scendere sotto le previsioni.

Tuttavia, i ricordi di un'inflazione transitoria rimangono freschi e le preoccupazioni riguardo la ripresa delle pressioni sui prezzi a causa di una crescita eccezionale o potenziali shock del petrolio persistono. Come avverte lo stesso Jerome Powell, non sono stati esclusi ulteriori aumenti dei tassi. Sono in discussione tre tagli di tasso di un quarto di punto per il 2024, secondo i verbali di dicembre del Federal Open Market Committee (FOMC), ma non è certo quando verranno attuati.

Aggiungendo complessità, è il paesaggio mutevole dei rendimenti dei Treasury. Il potere d'acquisto ridotto della Fed e il crescente deficit di bilancio degli Stati Uniti creano una tempesta perfetta per l'aumento dei tassi a lungo termine. La domanda estera in calo per i Treasury e il rilascio del Giappone dal controllo della curva dei rendimenti alimentano ulteriormente la traiettoria in rialzo. Tuttavia, è fondamentale ricordare che questi rendimenti si stanno semplicemente correggendo da livelli storicamente bassi e da una prolungata inversione. I mercati azionari statunitensi sono pronti a navigare la prima metà dell'anno, traendo indicazioni dai fondamenti sottostanti e dalle pubblicazioni di dati economici, con potenziali cambiamenti o incertezze geopolitiche che si profilano dopo.

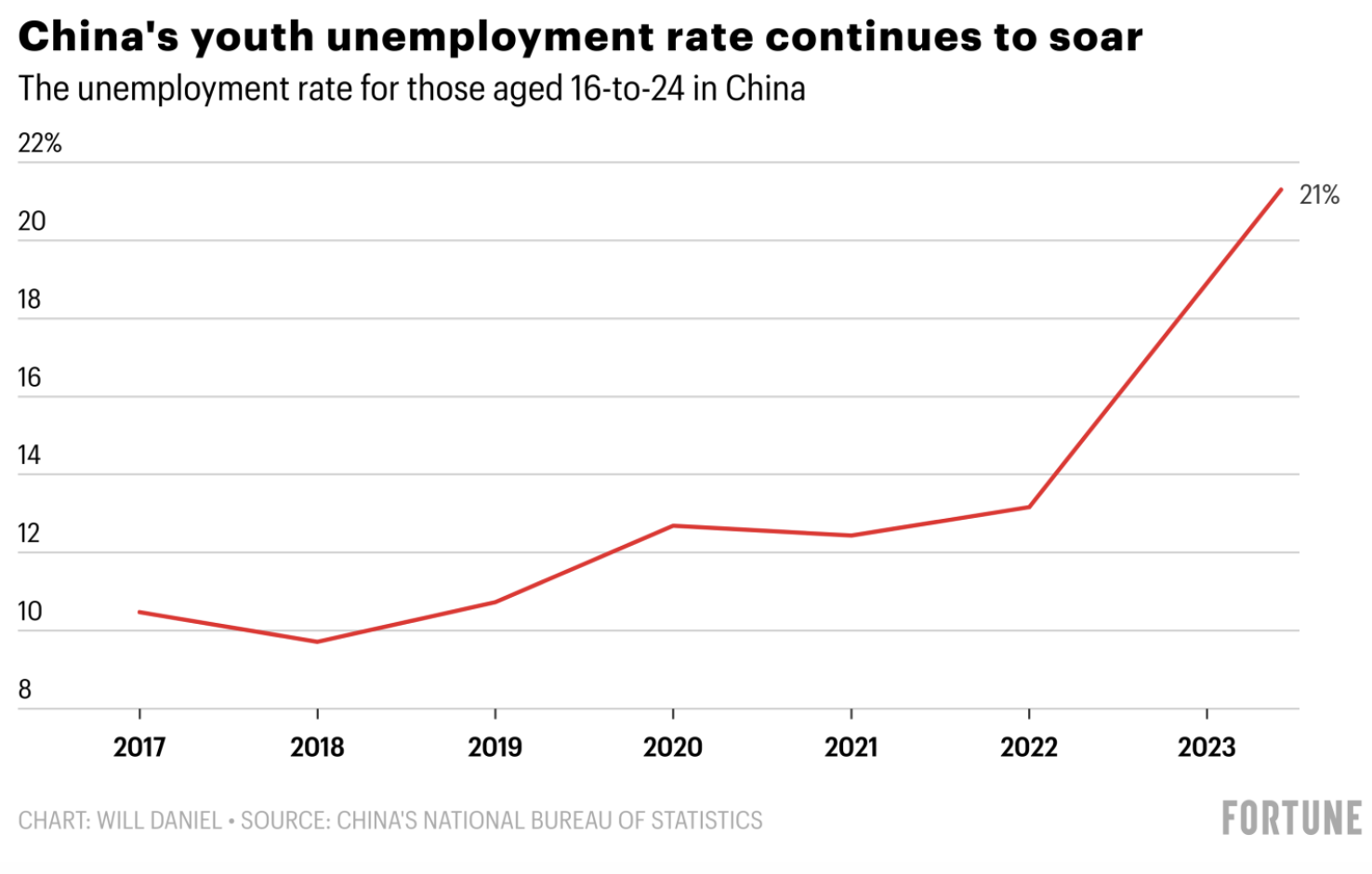

Cina: il calo della crescita incontra obiettivi a lungo termine

L'ottimismo iniziale del 2024 per una Cina post-pandemia è svanito quando un prolungato calo del mercato immobiliare, l'aumento della disoccupazione giovanile e le incertezze normative hanno bloccato il mercato. Con la costruzione e il settore immobiliare che a lungo hanno alimentato il motore dell'economia, la crisi immobiliare ha ripercussioni profonde, innescando significative vendite di azioni.

Un barlume di speranza brilla da una potenziale ripresa dello yuan nel 2024, la prima in tre anni. Un restringimento del divario dei tassi d'interesse potrebbe fermare l'uscita di capitali, come previsto da un'indagine di Bloomberg. Tuttavia, i tagli ai tassi limitati e una salvezza poco chiara per il settore immobiliare gettano ombre sul rimbalzo. Gli investitori esteri rimangono in attesa, aspettando un'azione decisiva da parte del governo prima di immergersi nuovamente. Nonostante le sfide, i leader cinesi esprimono una fiducia incrollabile nella loro visione a lungo termine per la trasformazione economica della nazione. Le riforme strutturali mirano alla prosperità condivisa e alla crescita sostenibile, esemplificate dall'impegno della Cina a raggiungere il picco delle emissioni di carbonio nel 2030 e a ottenere la neutralità carbonica entro il 2060.

Il Giappone per porre fine finalmente ai tassi d'interesse

Lo yen affronta una pressione rinnovata a seguito di un significativo terremoto di Capodanno in Giappone, complicando gli sforzi della Banca del Giappone per eliminare i tassi d'interesse negativi questo mese. Sebbene non sia probabile che ci siano cambiamenti a gennaio, la maggior parte delle persone si aspetta che i tassi d'interesse negativi finiscano ad aprile o più tardi nel 2024. Questo suggerisce che potrebbero esserci maggiori volatilità nel valore dello yen giapponese.

Eurozona, Regno Unito: Combattere le pressioni inflazionistiche

Si prevede che Regno Unito ed Europa sperimenteranno una lieve recessione e una crescita minima nel 2024, caratterizzate da una crescita più lenta e un'inflazione ostinata.

L'inflazione è stata più persistente in queste regioni a causa della loro maggiore dipendenza dalle importazioni di materie prime ed energia. I prezzi dell'energia e delle materie prime si prevede rimarranno superiori ai livelli pre-crisi, influenzati da incertezze geopolitiche e dagli attesi tagli ai tassi statunitensi. Di conseguenza, i tassi d'interesse chiave nell'UE e nel Regno Unito sono previsti rimanere più elevati per più tempo per controllare l'inflazione.

I tassi d'interesse più elevati tendono ad avere effetti visibili sul debito pubblico, portando a un aumento continuo del debito nazionale. Con un debito sostanziale dalla pandemia e dal conflitto in Ucraina, la capacità dei governi UE e UK di stabilizzare le loro economie sta diminuendo. Le opzioni limitate per stimoli fiscali aggiuntivi determinano uno scenario di stagflazione, a differenza degli Stati Uniti, dove la crescita rimane resiliente e l'inflazione è sotto controllo.

Mercati emergenti: in piedi da soli

Con il raffreddamento dei tassi d'interesse negli Stati Uniti e il dollaro che allenta la sua presa, JP Morgan prevede una rinascita nei mercati emergenti nella seconda metà del 2024. Questo slancio è alimentato da un cambiamento globale nelle catene di approvvigionamento, sfuggendo al lungo dominio della Cina.

I beneficiari di questo riallineamento includono regioni come l'America Latina, l'Europa, il Medio Oriente e l'Africa (EMEA), l'Associazione delle Nazioni del Sud-est asiatico (ASEAN) e l'India. Questi nuovi arrivati offrono un potente cocktail di lavoro economico, robusta manifattura e un tesoro di materie prime essenziali. Con uno scenario di manifattura fiorente, una vasta forza lavoro e risorse naturali come energia, rame e litio (il cuore dei veicoli elettrici (EV) e delle rinnovabili), l'America Latina si distingue come un contendore di primo piano.

L'aumento degli investimenti diretti esteri (FDI) dipinge un quadro vivace per l'ASEAN, con il Vietnam che guida la carica. Le grandi aziende che cercano diversificazione stanno aprendo attività, con la straordinaria crescita del Vietnam che diventa un caso di studio. Nel settore tecnologico, la Malesia emerge come campione della confezione e test avanzati dei semiconduttori, mentre Singapore regna suprema come hub di fabbricazione di wafer. La ricchezza di nichel dell'Indonesia e l'affermato sistema di approvvigionamento auto della Thailandia li rendono giocatori vitali nel gioco dei veicoli elettrici.

I recenti successi elettorali di Narendra Modi hanno rafforzato la già impressionante crescita dell'India, alimentata dai cambiamenti della fornitura globale e dai costi competitivi del lavoro. Questo si traduce in massimi storici per le azioni indiane nel 2024, con il Sensex e il Nifty che raggiungono vertiginose nuove vette.

Anche se l'incertezza potrebbe persistere, il potenziale per una robusta ripresa nei mercati emergenti durante la seconda metà del 2024 appare allettante. Con tassi più bassi, un dollaro più debole e catene di approvvigionamento che cambiano, queste stelle nascenti sono pronte a prendersi la scena e ridefinire il panorama economico globale.

Intelligenza artificiale: riflettori sui semiconduttori

Il recente progresso nell'IA è un cambiamento di gioco per la globalizzazione. Si distingue come un punto saliente per il 2024 con profonde implicazioni per il trading e gli investimenti.

L'IA generativa è un tipo di algoritmo IA che crea contenuti basati su dati esistenti. Alimenta l'innovazione in vari settori oltre alla tecnologia, dal trasporto e alla sanità all'istruzione e al commercio. Tra i beneficiari notabili ci sono aziende di giochi, produttori di veicoli elettrici, attori dell'e-commerce e fornitori di cloud.

Gli analisti prevedono un outlook positivo per il settore dei semiconduttori nel 2024. Si prevede che l'industria sosterrà il suo recupero dalla recessione del 2022 e mostrerà crescita in tutti i segmenti. I progressi nell'IA dipendono fortemente dai chip semiconduttori di alto livello per l'elaborazione e l'analisi dei dati. Le tensioni commerciali in corso tra Stati Uniti e Cina nel settore dei semiconduttori hanno creato uno squilibrio tra domanda e offerta. Questo ha portato a un aumento dei prezzi e dei margini per i semiconduttori, influenzando le valutazioni delle aziende del settore.

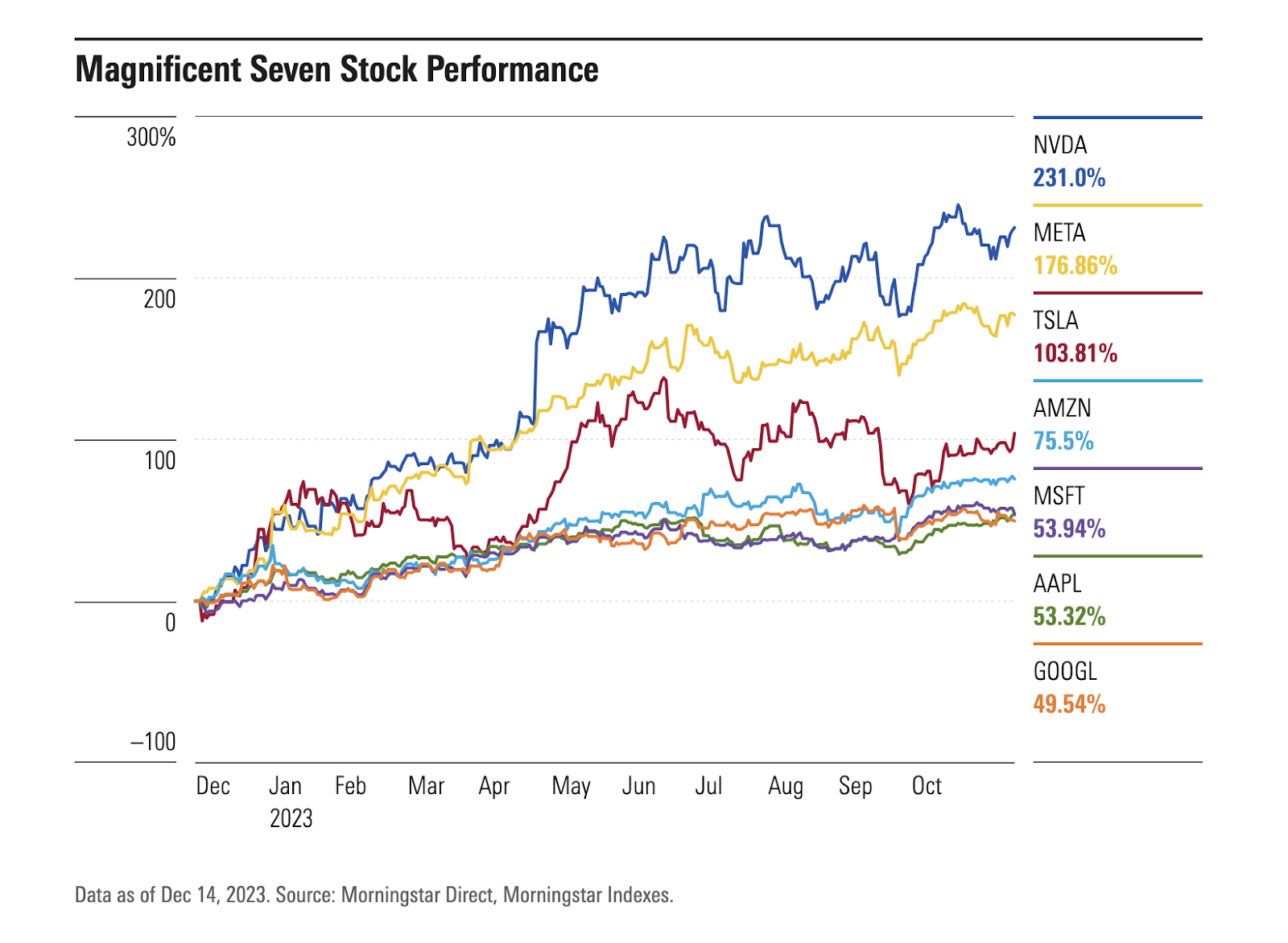

A partire dal 2023, l'industria dei semiconduttori è rimbalzata, e un fattore significativo dietro questa rinascita è NVIDIA Corp. (NVDA), un protagonista nel mercato in espansione delle unità di elaborazione grafica (GPU) per applicazioni IA. Le azioni di Nvidia sono aumentate di oltre tre volte, rendendola il primo produttore di chip a raggiungere una capitalizzazione di mercato superiore a 1 trilione di USD. Un altro attore notevole nel settore IA, Advanced Micro Devices Inc. (AMD), ha conquistato il secondo posto tra i componenti dell'indice, registrando un notevole aumento delle azioni di quasi il 130% quest'anno.

Oltre ai produttori di chip negli Stati Uniti, a Singapore e in Malesia, come menzionato in precedenza, altri chiari beneficiari includono Corea e Taiwan. Le fabbriche coreane stanno sviluppando i chip di memoria ad alta larghezza di banda di prossima generazione che beneficeranno dall'adozione diffusa dell'IA. Taiwan vanta una catena di approvvigionamento industriale completa che supporta le attuali e future tendenze dell'industria IA.

Rischi da monitorare: geopolitici, instabilità finanziaria

Nel 2024, in un anno elettorale cruciale, le tensioni e i rischi geopolitici globali sono in aumento. Due conflitti maggiori e elezioni in 40 paesi, compresi quelli principali come Stati Uniti, Regno Unito e UE, contribuiscono all'incertezza. Morgan Stanley prevede una maggiore volatilità negli attivi ad alto rischio rispetto all'anno precedente.

I canali di investimento e le catene di approvvigionamento sono intrinsecamente legati alla leadership di ciascun paese. Le continue tensioni USA-Cina, il conflitto Russia-Ucraina e il conflitto Israele/Hamas rappresentano fattori di rischio sostanziali.

Inoltre, le preoccupazioni riguardanti il rallentamento della crescita economica sollevano interrogativi sulla sostenibilità fiscale dei governi e sul debito aziendale. Eastspring Investments, con sede a Singapore, adotta una posizione difensiva nello spazio creditizio statunitense, preferendo il grado di investimento statunitense rispetto ai bond corporate ad alto rendimento. Le loro ricerche indicano una potenziale sottovalutazione dei rischi di rifinanziamento aziendale man mano che si espande il muro di scadenza nei prossimi anni.

Sia l'UE che gli USA stanno affrontando una crescente minaccia di default sui prestiti immobiliari commerciali, ponendo rischi per le istituzioni finanziarie. Costi di finanziamento più elevati, potenziali debolezze di capitale normativo e rischi crescenti associati ai prestiti immobiliari commerciali, unitamente a una domanda debole per spazi ufficio, spingono per una revisione delle banche. Moody's Investors Service ha abbassato il rating creditizio di 10 banche statunitensi più piccole e potrebbe estendere questa azione a grandi prestatori come US Bancorp, Bank of New York Mellon, State Street e Truist Financial, evidenziando le crescenti pressioni sull'industria.

Nonostante un aumento dei rendimenti obbligazionari, gli spread creditizi non si sono ampliati in modo significativo. Questo fenomeno ha giocato un ruolo nel minimizzare le bancarotte e le perdite di posti di lavoro. Analisti di varie importanti banche di Wall Street prevedono un lieve deterioramento delle condizioni creditizie nel 2024, fornendo un cuscinetto per le aziende, i posti di lavoro e la crescita economica complessiva contro un possibile declino più grave.

Conclusione

Navigare nel paesaggio di investimento in cambiamento nel 2024 richiede una chiara comprensione dei fattori macroeconomici, delle strategie di allocazione degli attivi e del ruolo dell'intelligenza artificiale all'interno delle aziende e dei beni privati.

Nella prima metà del 2024, la traiettoria dei mercati è destinata a essere fortemente influenzata dai fondamenti economici in corso, poiché le conseguenze delle elezioni e i potenziali rischi di credito devono ancora essere completamente valutati.

Sebbene gli investitori possano normalmente anticipare e prepararsi a vari rischi, la minaccia più significativa deriva spesso da un imprevisto "colpo di scena" — un evento che sorprende tutti. Dal momento che questi eventi non sono considerati nei prezzi di mercato, possono provocare importanti interruzioni quando si verificano. Esempi recenti includono l'imprevista pandemia di COVID-19 e la guerra in Ucraina, entrambe gli eventi che pochi investitori si aspettavano. Riconoscendo la natura imprevedibile del panorama finanziario, è sensato considerare potenziali sfide impreviste anche nel 2024.

Dichiarazione di non responsabilità:

Le informazioni contenute in questo articolo del blog sono solo a scopo educativo e non sono intese come consigli finanziari o di investimento. Si considera accurato alla data di pubblicazione dalle fonti. Cambiamenti delle circostanze dopo il momento della pubblicazione possono influire sull'accuratezza delle informazioni.

Il trading è rischioso. Le performance passate non sono indicative dei risultati futuri. Si consiglia di fare ricerche autonome prima di prendere qualsiasi decisione di trading.