2024 এর ট্রাইলেমা: মুদ্রাস্ফীতি, স্ট্যাগফ্লেশন বা নরম অবতরণ

ক্রিস্টাল বল ভুলে যান; 2024 সালে সাফল্য আর্থিক নীতিগুলিকে কঠোর করে এবং 2023 সালে ক্ষমতার গতিশীলতার পরিবর্তনের মাধ্যমে তৈরি একটি পরিবর্তিত ল্যান্ডস্কেপ নেভিগেট করার উপর নির্ভর করে৷

যদিও একটি বেস কেস দৃশ্যকল্প ধীরে ধীরে বৃদ্ধির একটি ছবি আঁকে, ঝুঁকি এবং সুযোগের লুকানো স্রোত পৃষ্ঠের ঠিক নীচে ঘূর্ণায়মান। এই 2024 দৃষ্টিভঙ্গি মূল প্রবণতাগুলিকে বিচ্ছিন্ন করে এবং সামনের বছরে সম্ভাব্য সাফল্য আনলক করতে market বিনিয়োগকারীরা নেভিগেট করতে পারে এমন চ্যালেঞ্জগুলি।

মার্কিন যুক্তরাষ্ট্র: নরম অবতরণ, কিন্তু মুদ্রাস্ফীতির দিকে নজর রাখুন

অতিরিক্ত ভোক্তা সঞ্চয় হ্রাস পাচ্ছে এবং উচ্চতর সুদের হার পণ্য, পরিষেবা এবং আবাসনের চাহিদাকে প্রভাবিত করছে। 2024 সালের শুরুতে মার্কিন ত্রৈমাসিক গ্রস ডোমেস্টিক প্রোডাক্ট (GDP) প্রবৃদ্ধির সাময়িক দুর্বলতা প্রত্যাশিত, অর্থনৈতিক বিশ্লেষকদের একটি বিস্তৃত সেট দ্বারা একটি পূর্ণ-বিকশিত মন্দা প্রত্যাশিত নয়৷

ফেডারেল রিজার্ভ 2026 সালের চতুর্থ ত্রৈমাসিকে তার 2% কনজিউমার প্রাইস ইনডেক্স (CPI) লক্ষ্যে পৌঁছানোর আগে 2024 সালে সামগ্রিক মুদ্রাস্ফীতি এবং ধীর অর্থনৈতিক প্রবৃদ্ধি অব্যাহত রাখার পূর্বাভাস দেয়।

ফেডারেল রিজার্ভ একটি সূক্ষ্ম ভারসাম্যমূলক কাজ করে মন্থর প্রবৃদ্ধি এবং ক্রমাগত মুদ্রাস্ফীতি উভয়ই চোখ। হার বৃদ্ধিতে তাদের সাম্প্রতিক বিরতি আস্তিত্বের স্বীকৃতির ইঙ্গিত দেয়, যা মূল ব্যক্তিগত ব্যয় ব্যয় (PCE) রিডিংগুলির সাথে সামঞ্জস্যপূর্ণ হয়ে যায় সম্ভবত অনুমানগুলির নীচে নেমে যায়।

যাইহোক, স্থায়ী মুদ্রাস্ফীতির স্মৃতি তাজা থাকে এবং ব্যতিক্রমী বৃদ্ধি বা সম্ভাব্য তেলের শকের কারণে পুনরায় মূল্য চাপ নিয়ে উদ্বেগ স্থায়ী হয়। জেরোম পাওয়েল নিজেই সতর্ক করেছেন, আরও হার বৃদ্ধি অস্বীকার করা হয়নি। ফেডারেল ওপেন Market কমিটি (FOMC) ডিসেম্বর মিনিট অনুসারে, 2024-এর জন্য তিন চতুর্থাংশ-পয়েন্ট রেট কমানোর টেবিলে রয়েছে, তবে সেগুলি কখন বাস্তবায়িত হবে তা অনিশ্চিত।

জটিলতার সাথে যুক্ত হ'ল ট্রেজারি ফলনের পরিবর্তিত ল্যান্ডস্কেপ। ফেডের ক্রয় ক্ষমতা হ্রাস করা এবং মার্কিন বাজেট ঘাটতির বেলুনিং দীর্ঘমেয়াদী হার বৃদ্ধির জন্য একটি নিখুঁত ঝড় তৈরি করে। ট্রেজারিগুলির জন্য বিদেশী চাহিদা হ্রাস এবং জাপানের ফলন বক্ররেখা নিয়ন্ত্রণের শিথিলতা ঊর্ধ্বমুখী গতিপথকে আরও জ্বালানি দেয়। তবুও, এটা মনে রাখা গুরুত্বপূর্ণ যে এই ফলনগুলি কেবল ঐতিহাসিকভাবে নিম্ন স্তরের এবং একটি দীর্ঘস্থায়ী বিপর্যয় থেকে সংশোধন করেছে। মার্কিন ইক্যুইটি markets বছরের প্রথমার্ধে নেভিগেট করার জন্য প্রস্তুত, অন্তর্নিহিত মৌলিক এবং অর্থনৈতিক ডেটা রিলিজ থেকে নির্দেশিকা অঙ্কন করে, সম্ভাব্য স্থানান্তর বা ভূ-রাজনৈতিক অনিশ্চয়তা পরবর্তীতে লুমছে।

চীন: দীর্ঘমেয়াদী লক্ষ্য পূরণ করছে

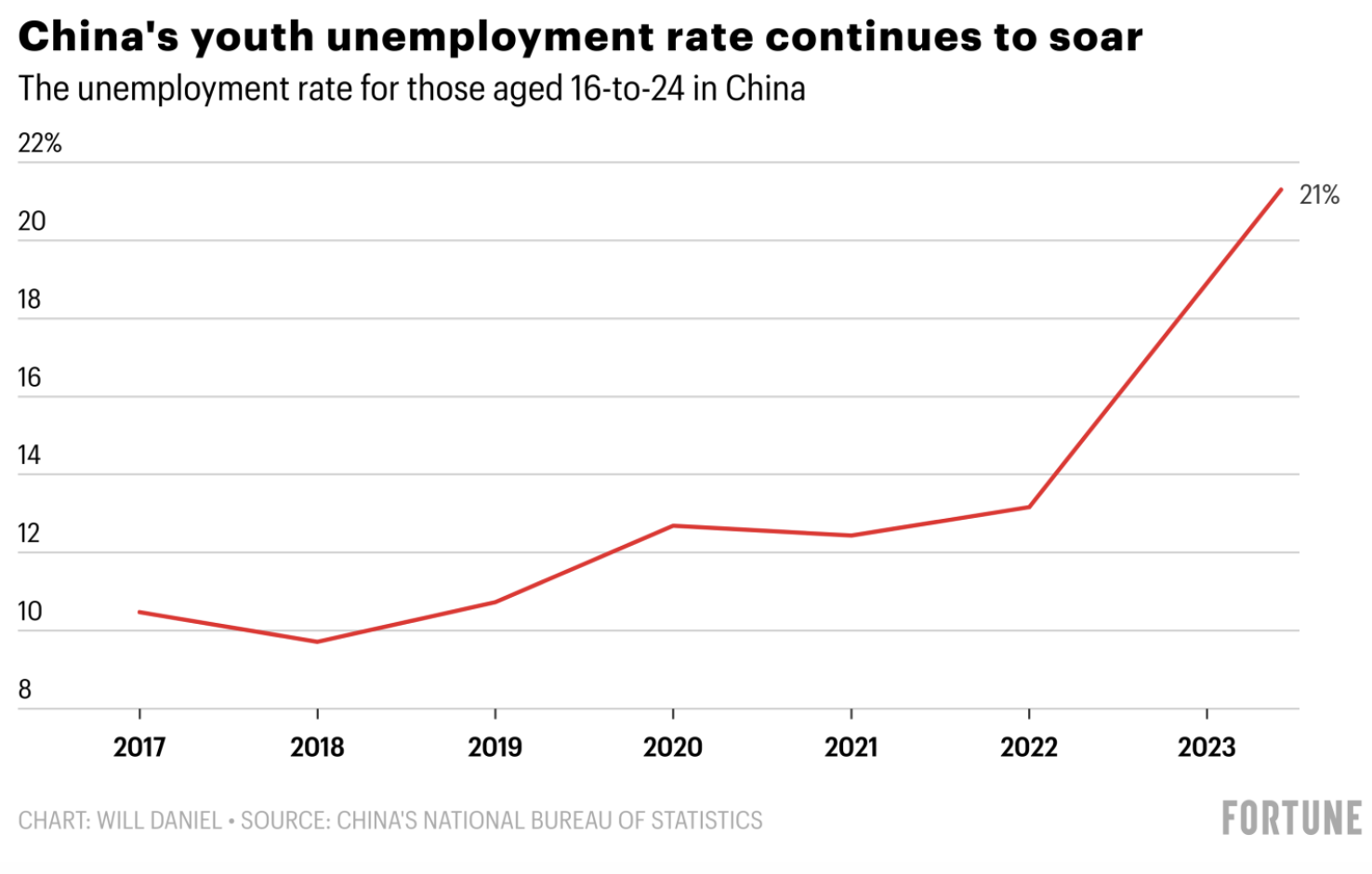

2024-এর পোস্ট-মহামারী চীনের জন্য প্রাথমিক আশাবাদ ছড়িয়ে পড়ে কারণ বর্ধিত আবাসন মন্দা, ক্রমবর্ধমান যুব বেকারত্ব এবং নিয়ন্ত্রক অনিশ্চয়তা market এর উপর ব্রেক ফেলেছে। নির্মাণ এবং রিয়েল এস্টেট দীর্ঘকাল ধরে অর্থনীতির ইঞ্জিনকে জ্বালানি দিয়ে, সম্পত্তি সংকট গভীরভাবে ছড়িয়ে পড়ে, উল্লেখযোগ্য ইক্যুইটি বিক্রির সূত্রপাত করে।

2024 সালে একটি সম্ভাব্য ইউয়ান সমাবেশ থেকে আশার ঝলক দেখা যায়, যা তিন বছরের মধ্যে প্রথম। ব্লুমবার্গের সমীক্ষায় অনুমান করা হয়েছে, সুদের হারের একটি ব্যবধান সংকুচিত করা মূলধনের প্রবাহকে বাঁচাতে পারে। যাইহোক, সীমিত হার হ্রাস এবং সম্পত্তি খাতের জন্য একটি অস্পষ্ট বেলআউট পুনরাবৃত্তির উপর ছায়া ফেলে। বিদেশী বিনিয়োগকারীরা ফিরে যাওয়ার আগে সরকারের সিদ্ধান্তমূলক পদক্ষেপের অপেক্ষায় রয়েছেন। চ্যালেঞ্জ সত্ত্বেও, চীনা নেতারা জাতির অর্থনৈতিক রূপান্তরের জন্য তাদের দীর্ঘমেয়াদী দৃষ্টিভঙ্গিতে অটুট আস্থা প্রকাশ করেছেন। কাঠামোগত সংস্কারগুলি সাধারণ সমৃদ্ধি এবং টেকসই বৃদ্ধিকে লক্ষ্য করে, 2030 সালে সর্বোচ্চ কার্বন নির্গমন এবং 2060 সালের মধ্যে কার্বন নিরপেক্ষতা অর্জনে চীনের প্রতিশ্রুতি দ্বারা উদাহরণ।

অবশেষে সুদের হার বন্ধ করবে জাপান

জাপানে একটি উল্লেখযোগ্য নববর্ষ দিবসের ভূমিকম্পের পর ইয়েন নতুন চাপের সম্মুখীন হয়েছে, যা এই মাসে ঋণাত্মক সুদের হার দূর করার জন্য ব্যাংক অফ জাপানের প্রচেষ্টাকে জটিল করে তুলছে। যদিও জানুয়ারিতে পরিবর্তন হওয়ার সম্ভাবনা নেই, বেশিরভাগ লোক আশা করেন নেতিবাচক সুদের হার এপ্রিল মাসে বা পরে 2024 সালে শেষ হবে। এটি পরামর্শ দেয় যে জাপানি ইয়েনের মূল্যে অস্থিরতা বৃদ্ধি পেতে পারে।

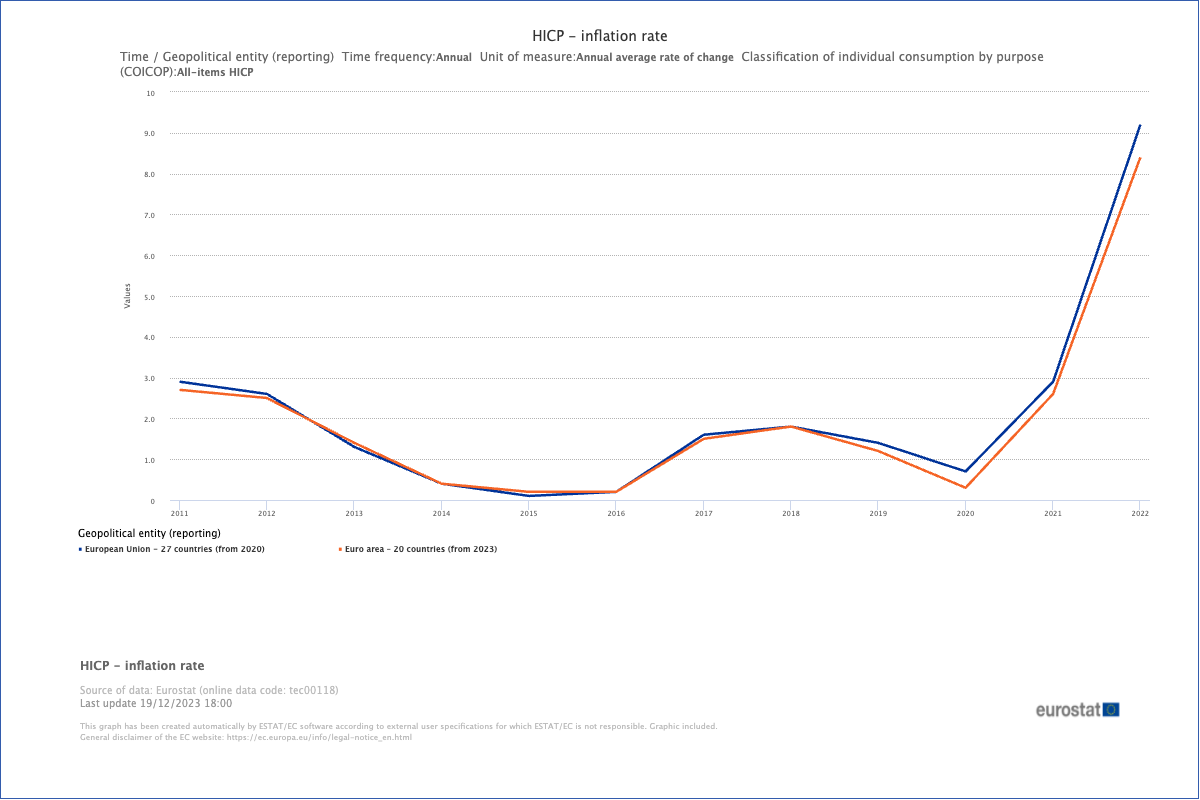

ইউরোজোন, UK: মুদ্রাস্ফীতির চাপের সাথে লড়াই

যুক্তরাজ্য এবং ইউরোপ 2024 সালে হালকা মন্দা এবং ন্যূনতম বৃদ্ধির অভিজ্ঞতা অর্জন করবে বলে আশা করা হচ্ছে, যা ধীর বৃদ্ধি এবং কঠিন মুদ্রা

পণ্য এবং শক্তি আমদানির উপর তাদের ভারী নির্ভরতার কারণে এই অঞ্চলগুলিতে মুদ্রাস্ফীতি আরও অবিচ্ছিন্ন হয়েছে। ভূ-রাজনৈতিক অনিশ্চয়তা এবং প্রত্যাশিত মার্কিন হার হ্রাস দ্বারা প্রভাবিত হয়ে শক্তি এবং পণ্যের মূুল্য প্রাক-সংকটের স্তরের উপরে থাকবে বলে আশা করা হচ্ছে। ফলস্বরূপ, মূল্যস্ফীতি নিয়ন্ত্রণ করতে ইইউ এবং যুক্তরাজ্যের মূল সুদের হার দীর্ঘ সময়ের জন্য higher থাকবে বলে অনুমান করা হচ্ছে।

higher সুদের হার সরকারি ঋণের উপর দৃশ্যমান প্রভাব ফেলে, যা জাতীয় ঋণের ক্রমাগত rise এর দিকে পরিচালিত করে। মহামারী এবং ইউক্রেনের দ্বন্দ্ব থেকে যথেষ্ট ঋণের কারণে, ইইউ এবং যুক্তরাজ্য সরকারগুলির তাদের অর্থনীতিকে স্থিতিশীল করার ক্ষমতা হ্রাস পাচ্ছে। অতিরিক্ত আর্থিক উদ্দীপনার জন্য সীমিত বিকল্পগুলির ফলে মার্কিন যুক্তরাষ্ট্রের বিপরীতে একটি স্থবিরতা পরিস্থিতি তৈরি হয়, যেখানে বৃদ্ধি স্থিতিস্থাপক থাকে এবং মুদ্রাস্ফীতি under নিয়ন্ত্রণে থাকে।

উদীয়মান বাজার: তাদের নিজের উপর দাঁড়িয়ে

মার্কিন যুক্তরাষ্ট্রে সুদের হার শীতল হওয়ার সাথে সাথে ডলার তার গ্রিপ কমেছে, জেপি মরগান 2024 সালের শেষার্ধে উদীয়মান markets পুনরুজ্জীবিত হওয়ার পূর্বাভাস দিয়েছে। চীনের আধিপত্যের দীর্ঘ ছায়া থেকে বাঁচতে এই গতি সরবরাহ শৃঙ্খলে বৈশ্বিক পরিবর্তনের দ্বারা উত্সাহিত হয়।

এই পুনর্বিন্যাসের সুবিধাভোগীদের মধ্যে রয়েছে ল্যাটিন আমেরিকা, ইউরোপ, মধ্যপ্রাচ্য ও আফ্রিকা (EMEA), দক্ষিণ-পূর্ব এশিয়ান নেশনস (ASEAN) এবং ভারতের মতো অঞ্চল। এই উদীয়মান তারাগুলি সাশ্রয়ী শ্রমের একটি শক্তিশালী ককটেল, শক্তিশালী উত্পাদন এবং প্রয়োজনীয় পণ্যের ভান্ডার সরবরাহ করে। একটি আলোড়ন সৃষ্টিকারী দৃশ্য, বিশাল জনবল এবং শক্তি, তামা এবং লিথিয়ামের মতো প্রাকৃতিক সম্পদ (ইলেকট্রিক যান (EVs) এবং পুনর্নবীকরণযোগ্য পদার্থের প্রাণবন্ত) নিয়ে গর্ব করা, ল্যাটিন আমেরিকা একটি প্রধান প্রতিযোগী হিসাবে উজ্জ্বল।

বিদেশী সরাসরি ক্রমবর্ধমান বিনিয়োগ (FDI) আসিয়ানের জন্য একটি প্রাণবন্ত চিত্র এঁকেছে, যেখানে ভিয়েতনাম নেতৃত্ব দিচ্ছে। বৈচিত্র্যের সন্ধানকারী প্রধান সংস্থাগুলি দোকান স্থাপন করছে, ভিয়েতনামের দুর্দান্ত বৃদ্ধি পাঠ্যপুস্তকের ক্ষেত্রে পরিণত হয়েছে৷ প্রযুক্তির ক্ষেত্রে, মালয়েশিয়া উন্নত সেমিকন্ডাক্টর প্যাকেজিং এবং পরীক্ষার একটি চ্যাম্পিয়ন হিসাবে আবির্ভূত হয়েছে, যখন সিঙ্গাপুর একটি ওয়েফার ফ্যাব্রিকেশন হাব হিসাবে সর্বোচ্চ রাজত্ব করছে। ইন্দোনেশিয়ার নিকেল সম্পদ এবং থাইল্যান্ডের প্রতিষ্ঠিত অটো সাপ্লাই চেইন তাদের বৈদ্যুতিক গাড়ির খেলায় গুরুত্বপূর্ণ খেলোয়াড় করে তোলে।

নরেন্দ্র মোদির সাম্প্রতিক নির্বাচনী জয় ইতিমধ্যেই ভারতের চিত্তাকর্ষক প্রবৃদ্ধিকে জোরদার করেছে, যা বৈশ্বিক সরবরাহের পরিবর্তন এবং প্রতিযোগিতামূলক শ্রম ব্যয়ের দ্বারা ইন্ধন দেওয়া হয়েছে। এটি 2024 সালে ভারতীয় স্টকগুলির জন্য রেকর্ড highs অনুবাদ করে, সেনসেক্স এবং নিফটি চকচকে নতুন শিখরে পৌঁছেছে৷

যদিও অনিশ্চয়তা দীর্ঘস্থায়ী হতে পারে, 2024 সালের দ্বিতীয়ার্ধে উদীয়মান markets একটি শক্তিশালী পুনরুজ্জীবনের সম্ভাবনা উদ্বেগজনক বলে মনে হচ্ছে৷ lower হার, দুর্বল ডলার এবং পরিবর্তন সাপ্লাই চেইনের সাথে এই উদীয়মান তারকাগুলি স্পটলাইট ধরে নেওয়ার এবং বিশ্বব্যাপী অর্থনৈতিক দৃশ্যের পুনর্নির্ধারণ করার জন্য প্রস্তুত।

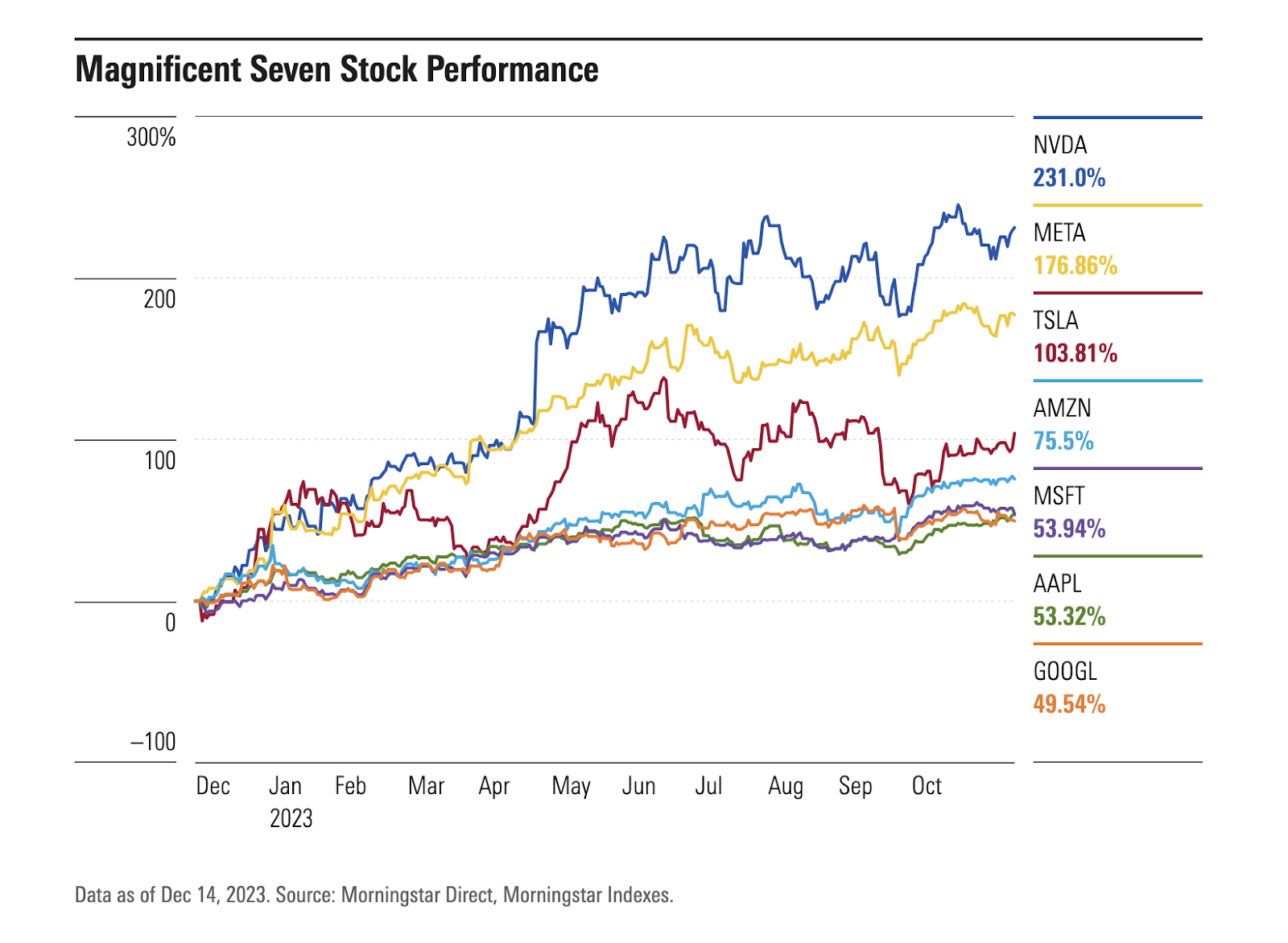

কৃত্রিম বুদ্ধিমত্তা: সেমিকন্ডাক্টরগুলিতে স্পটলাইট

এআইতে সাম্প্রতিক অগ্রগতি বিশ্বায়নের জন্য একটি গেম-চেঞ্জার। এটি ট্রেডিং এবং বিনিয়োগের জন্য গভীর প্রভাব সহ 2024 এর জন্য একটি মূল হাইলাইট হিসাবে দাঁড়িয়েছে।

জেনারেটিভ এআই এক ধরণের এআই অ্যালগরিদম যা বিদ্যমান ডেটার উপর ভিত্তি করে সামগ্রী তৈরি করে। এটি প্রযুক্তির বাইরে বিভিন্ন শিল্পে উদ্ভাবনকে জ্বালানি দেয়—পরিবহন এবং স্বাস্থ্যসেবা থেকে শিক্ষা এবং খুচরা পর্যন্ত। উল্লেখযোগ্য সুবিধাভোগীদের মধ্যে রয়েছে গেমিং ফার্ম, বৈদ্যুতিক যানবাহন নির্মাতা, ই-কমার্স প্লেয়ার এবং ক্লাউড প্রদানকারী।

বিশ্লেষকরা 2024 সালে সেমিকন্ডাক্টর সেক্টরের জন্য একটি ইতিবাচক দৃষ্টিভঙ্গির পূর্বাভাস দিয়েছেন। শিল্পটি 2022 এর মন্দ থেকে তার পুনরুদ্ধার বজায় রাখবে এবং সমস্ত বিভাগে বৃদ্ধি প্রদর্শন করবে বলে আশা করা হচ্ছে। এআই-এর অগ্রগতিগুলি ডেটা প্রক্রিয়াকরণ এবং বিশ্লেষণের জন্য উচ্চ-সম্পদ সেমিকন্ডাক্টর চিপগুলির উপর নির্ভর করে। সেমিকন্ডাক্টর সেক্টরে মার্কিন যুক্তরাষ্ট্র এবং চীনের মধ্যে চলমান ট্রেড উত্তেজনা চাহিদা-সরবরাহের ভারসাম্যহীনতা তৈরি করেছে। এর ফলে অর্ধপরিবাহী সংস্থাগুলির মূল্যায়নকে প্রভাবিত করে সেমিকন্ডাক্টরগুলির মূুল্য এবং মার্জিন বৃদ্ধি পেয়েছে।

2023 সাল পর্যন্ত, অর্ধপরিবাহী শিল্প পুনরুজ্জীবিত হয়েছে এবং এই পুনরুজ্জীবনের পিছনে একটি উল্লেখযোগ্য কারণ NVIDIA Corp. (NVDA), এআই অ্যাপ্লিকেশনগুলির জন্য প্রসারিত গ্রাফিক্স প্রসেসিং ইউনিট (GPU) market এ শীর্ষস্থানীয়। Nvidia এর স্টক তিনগুণেরও বেশি বেড়েছে, এটি প্রথম চিপমেকার হিসেবে market মূলধন USD 1 ট্রিলিয়ন ছাড়িয়েছে। এআই সেক্টরের আরেকটি উল্লেখযোগ্য খেলোয়াড়, Advanced Micro Devices Inc. (AMD), সূচকের উপাদানগুলির মধ্যে দ্বিতীয় স্থান দাবি করেছে, এই বছর প্রায় 130% এর উল্লেখযোগ্য স্টক বৃদ্ধির সম্মুখীন হয়েছে।

মার্কিন যুক্তরাষ্ট্র, সিঙ্গাপুর এবং মালয়েশিয়ার চিপ নির্মাতাদের বাইরে, যেমনটি আগে উল্লেখ করা হয়েছে, অন্যান্য স্পষ্ট সুবিধাভোগীদের মধ্যে রয়েছে কোরিয়া এবং তাইওয়ান। কোরিয়ান ফ্যাবগুলি পরবর্তী প্রজন্মের হাই ব্যান্ডউইথ মেমরি চিপগুলি বিকাশ করছে যা এআইয়ের ব্যাপক গ্রহণ থেকে উপকৃত হবে। তাইওয়ান একটি সম্পূর্ণ শিল্প সরবরাহ চেইন নিয়ে গর্ব করে যা বর্তমান এবং ভবিষ্যতের AI শিল্পের প্রবণতাকে সমর্থন করে।

নিরীক্ষণের ঝুঁকি: ভূ-রাজনৈতিক, আর্থিক অস্থিতিশীলতা

2024 সালে, একটি গুরুত্বপূর্ণ নির্বাচনী বছরের মধ্যে, বিশ্বব্যাপী ভূ-রাজনৈতিক উত্তেজনা এবং ঝুঁকি rise করছে। মার্কিন যুক্তরাষ্ট্র, যুক্তরাজ্য এবং ইইউ-এর মতো বড় দেশসহ ৪০টি দেশে দুটি বড় দ্বন্দ্ব এবং নির্বাচন এই অনিশ্চয়তায় অবদান রাখে। মরগান স্ট্যানলি পূর্ববর্তী বছরের তুলনায় উচ্চ-ঝুঁকির সম্পদে বর্ধিত অস্থিরতা প্রত্যাশা করে।

বিনিয়োগ চ্যানেল এবং সরবরাহ চেইন প্রতিটি দেশের নেতৃত্বের সাথে জটিলভাবে যুক্ত। চলমান মার্কিন-চীন উত্তেজনা, রাশিয়া-ইউক্রেন দ্বন্দ্ব, এবং ক্রমাগত ইসরাইল/হামাস বিরোধ যথেষ্ট ঝুঁকিপূর্ণ কারণ।

উপরন্তু, মন্থর অর্থনৈতিক প্রবৃদ্ধির উদ্বেগ সরকার এবং কর্পোরেট ঋণের আর্থিক স্থায়িত্ব সম্পর্কে প্রশ্ন উত্থাপন করে। ইস্টস্প্রিং ইনভেস্টমেন্টস, সিঙ্গাপুরে অবস্থিত, মার্কিন ক্রেডিট স্পেসে একটি প্রতিরক্ষামূলক অবস্থান নেয়, উচ্চ ফলন কর্পোরেট বন্ডের চেয়ে ইউএস ইনভেস্টমেন্ট গ্রেড over পছন্দ করে। তাদের গবেষণা আগামী বছরগুলিতে পরিপক্কতার প্রাচীর প্রসারিত হওয়ার সাথে সাথে কর্পোরেট পুনঃঅর্থায়ন ঝুঁকির সম্ভাব্য নিম্নমূল্য নির্দেশ করে।

ইইউ এবং মার্কিন উভয়ই ট্রেডিক রিয়েল এস্টেট ঋণের ডিফল্টের ক্রমবর্ধমান হুমকির সাথে লড়াই করছে, যা আর্থিক প্রতিষ্ঠানগুলির জন্য ঝুঁকি তৈরি করে। Higher তহবিল খরচ, সম্ভাব্য নিয়ন্ত্রক মূলধন দুর্বলতা, এবং বাণিজ্যিক রিয়েল এস্টেট ঋণের সাথে যুক্ত ক্রমবর্ধমান ঝুঁকি, এবং অফিসের জায়গার জন্য দুর্বল চাহিদা, ব্যাঙ্কগুলির একটি পর্যালোচনাকে ত্বরান্বিত করে৷ মুডি’স ইনভেস্টর সার্ভিস 10টি ছোট ইউএস ব্যাঙ্কের ক্রেডিট রেটিং কমিয়েছে এবং এটি ইউএস ব্যানকর্প, ব্যাঙ্ক অফ নিউ ইয়র্ক মেলন, স্টেট স্ট্রিট এবং ট্রুইস্ট ফাইন্যান্সিয়ালের মতো বড় ঋণদাতাদের কাছে প্রসারিত করতে পারে, যা শিল্পের উপর বাড়ন্ত চাপকে তুলে ধরে।

বন্ডের ফলন বৃদ্ধি সত্ত্বেও, ক্রেডিট স্প্রেড আশ্চর্যজনকভাবে উল্লেখযোগ্যভাবে প্রসারিত হয়নি। এই ঘটনাটি দেউলিয়া হওয়া এবং চাকরি হারানোর ক্ষেত্রে ভূমিকা পালন করেছে। বিভিন্ন শীর্ষস্থানীয় ওয়াল স্ট্রিট ব্যাঙ্ক জুড়ে বিশ্লেষকরা 2024 সালে ক্রেডিট অবস্থার সামান্য অবনতির পূর্বাভাস দিয়েছেন, যা কোম্পানি, চাকরি এবং আরও গুরুতর পতনের বিরুদ্ধে সামগ্রিক অর্থনৈতিক বৃদ্ধির জন্য একটি বাফার প্রদান করবে।

উপসংহার

2024 সালে পরিবর্তিত বিনিয়োগের ল্যান্ডস্কেপ নেভিগেট করার জন্য সামষ্টিক অর্থনৈতিক কারণ, সম্পদ বরাদ্দ কৌশল এবং ট্রেড এবং ব্যক্তিগত সম্পদের মধ্যে কৃত্রিম বুদ্ধিমত্তার ভূমিকা সম্পর্কে

2024 সালের প্রাথমিক অর্ধে, বাজারগুলির গতিপথ চলমান অর্থনৈতিক মৌলিক বিষয়গুলি দ্বারা প্রচুর প্রভাবিত হওয়ার জন্য প্রস্তুত, কারণ নির্বাচনের প্রভাব এবং সম্ভাব্য ক্রেডিট ঝুঁকিগুলি এখনও পুরোপুরি মূল্যায়ন করা হয়নি।

যদিও বিনিয়োগকারীরা সাধারণত বিভিন্ন ঝুঁকির জন্য প্রত্যাশা করতে এবং প্রস্তুতি নিতে পারেন, তবে সবচেয়ে উল্লেখযোগ্য হুমকি প্রায়শই একটি অপ্রত্যাশিত “কার্ভবল” থেকে উদ্ভূত হয় - এমন একটি যেহেতু এই ইভেন্টগুলি বাজারের মূুল্যে বিবেচনা করা হয় না, তখন তারা ঘটে তখন বড় বাধা সৃষ্টি করতে পারে। সাম্প্রতিক উদাহরণগুলির মধ্যে রয়েছে অপ্রত্যাশিত COVID-19 মহামারী এবং ইউক্রেনের যুদ্ধ, উভয়ই কিছু বিনিয়োগকারী আশা করেছিল। আর্থিক ল্যান্ডস্কেপের অপ্রত্যাশিত প্রকৃতি স্বীকৃতি স্বীকার করে, 2024 সালেও সম্ভাব্য অপ্রত্যাশিত চ্যালেঞ্জগুলির জন্য বিবেচনা করা

অস্বীকৃতি:

এই ব্লগে থাকা তথ্য শুধুমাত্র শিক্ষামূলক উদ্দেশ্যে এবং আর্থিক বা বিনিয়োগের পরামর্শের উদ্দেশ্যে নয়। সূত্র দ্বারা প্রকাশের তারিখে এটি সঠিক বলে মনে করা হয়। প্রকাশ কালের পরে পরিস্থিতির পরিবর্তন তথ্যের নির্ভুলতাকে প্রভাবিত করতে পারে৷

ট্রেডিং ঝুঁকিপূর্ণ। অতীতের কর্মক্ষমতা ভবিষ্যতের ফলাফলের নির্দেশক নয়। কোনো ট্রেডিং সিদ্ধান্ত নেওয়ার আগে আপনার নিজের গবেষণা করার পরামর্শ দেওয়া হয়।