Why Gold is surging again: Can the rally last?

%20(1).png)

Gold is surging again; market data suggests investors are repositioning for a world defined by rising geopolitical risk and shifting monetary policy expectations. Spot prices have climbed back to record highs, surpassing $4,460 per ounce, and lifting year-to-date gains to around 70%, as markets respond to US actions against Venezuelan oil shipments and renewed uncertainty across global energy trade routes.

At the same time, analysts report that the outlook for US interest rates has turned decisively more supportive. With real yields falling to their lowest levels since mid-2022 and futures markets pricing in multiple Federal Reserve rate cuts next year, the opportunity cost of holding non-yielding assets has dropped sharply. The question now is whether these forces are powerful enough to sustain the rally or whether gold is nearing a turning point.

What’s driving gold?

The immediate catalyst behind gold’s latest surge is a rise in geopolitical tension centred on Venezuela. The US Coast Guard recently seized a sanctioned supertanker carrying Venezuelan oil and attempted to intercept two additional vessels, one of which was reportedly bound for China. These actions have raised concerns about broader energy-market disruptions, even as Venezuela’s reduced output limits direct supply risks.

Market sensitivity to geopolitical shocks remains high, particularly when they involve strategic commodities and major trading partners. President Donald Trump’s declaration of a naval “blockade” targeting sanctioned tankers has reinforced uncertainty rather than delivered clarity. History shows that gold responds less to the scale of economic damage and more to the unpredictability such confrontations introduce into global markets.

Monetary conditions have added a second, equally important layer of support. US real interest rates - a key driver of gold demand - have slipped to levels last seen more than three years ago.

According to futures pricing, traders continue to expect at least two Federal Reserve rate cuts in 2026, following signs of labour-market cooling and easing inflation pressures. As yields fall, gold’s relative appeal increases, particularly for institutional investors seeking stability and diversification.

Why it matters

Gold’s rally matters because it reflects a broader reassessment of risk rather than a short-lived flight to safety. The metal has not only recovered from its late-October pullback but has reasserted itself as one of the strongest-performing assets of the year. UBS strategists note that bullion is now consolidating gains at record levels after a sharp advance, reinforcing its status as a core defensive holding.

This performance signals what many analysts interpret as deeper concerns about financial resilience. Persistent geopolitical flashpoints, uncertainty surrounding US monetary leadership, and growing skepticism towards long-term debt sustainability have prompted investors to shift towards assets perceived as politically neutral. Gold’s liquidity, global acceptance, and history as a store of value place it in a unique position when confidence in fiat systems begins to fray.

Impact on markets and investors

Institutional and central bank demand is reshaping the structure of the gold market. UBS estimates that central banks will purchase between 900 and 950 metric tonnes of gold this year, close to record levels. This steady accumulation has reduced downside volatility and helped establish a new price floor well above $4,300 per ounce.

Currency dynamics have further reinforced the trend. The US dollar has slipped towards one-week lows against major peers, making dollar-priced bullion more affordable for overseas buyers. For investors outside the US, gold has served as both a hedge against currency weakness and protection against rising geopolitical uncertainty.

Silver’s parallel surge adds another dimension. Prices have climbed close to $70 per ounce after gaining roughly 140% this year, far outpacing gold. When both metals rally together, it often points to broad-based risk aversion combined with speculative participation, rather than a narrow defensive trade.

Expert outlook

Looking ahead, analysts broadly expect gold to consolidate rather than reverse sharply. UBS argues that prices are digesting gains after an aggressive move higher, supported by falling real yields and sustained institutional demand. The bank also highlights that gold has benefited from the US real interest rate dropping to its lowest level since mid-2022, reducing the opportunity cost of holding bullion.

There are, however, risks to monitor. Any sudden de-escalation in geopolitical tensions or a resurgence in real yields could prompt short-term corrections. Even so, portfolio managers increasingly view pullbacks as opportunities rather than warning signs. With some forecasts pointing towards $5,000 per ounce in 2026, gold’s role as both a hedge and a strategic asset appears firmly re-established.

Key takeaway

Gold’s renewed surge appears to be driven by a rare convergence of geopolitical risk, falling real yields, and persistent institutional demand. Analysts suggest that the rally reflects strategic repositioning rather than fear-based buying. With central banks still accumulating and rate cuts firmly on the horizon, gold’s role in portfolios is evolving. Investors will be watching inflation data, Federal Reserve signals, and geopolitical developments for the next decisive catalyst.

Gold technical insights

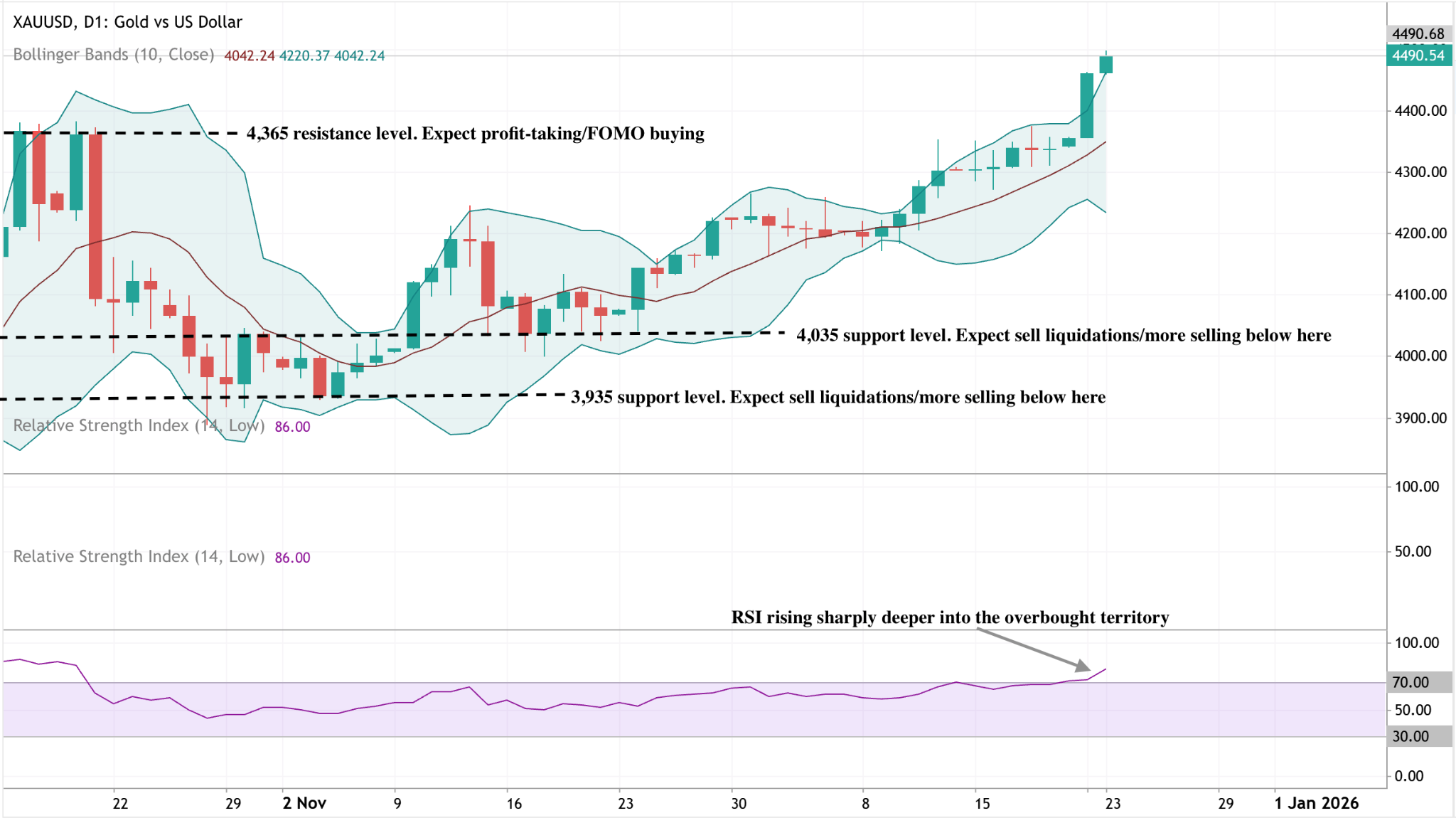

Gold remains firmly bullish, with price breaking higher and pushing along the upper Bollinger Band, signalling strong upside momentum and increasingly FOMO-driven buying. The sharp expansion of the bands highlights rising volatility in favour of the bulls.

On the downside, $4,365 now serves as near-term resistance and a reaction zone, while $4,035 and $3,935 remain the key supports. A break below these levels would likely trigger sell-side liquidations, but for now, dips continue to attract buyers. Momentum is stretched, with the RSI rising sharply deeper into overbought territory, increasing the risk of a pause or shallow pullback.

The performance figures quoted are not a guarantee of future performance.